This blog was co-authored by Srichandra Masabathula and Nicholas Godec

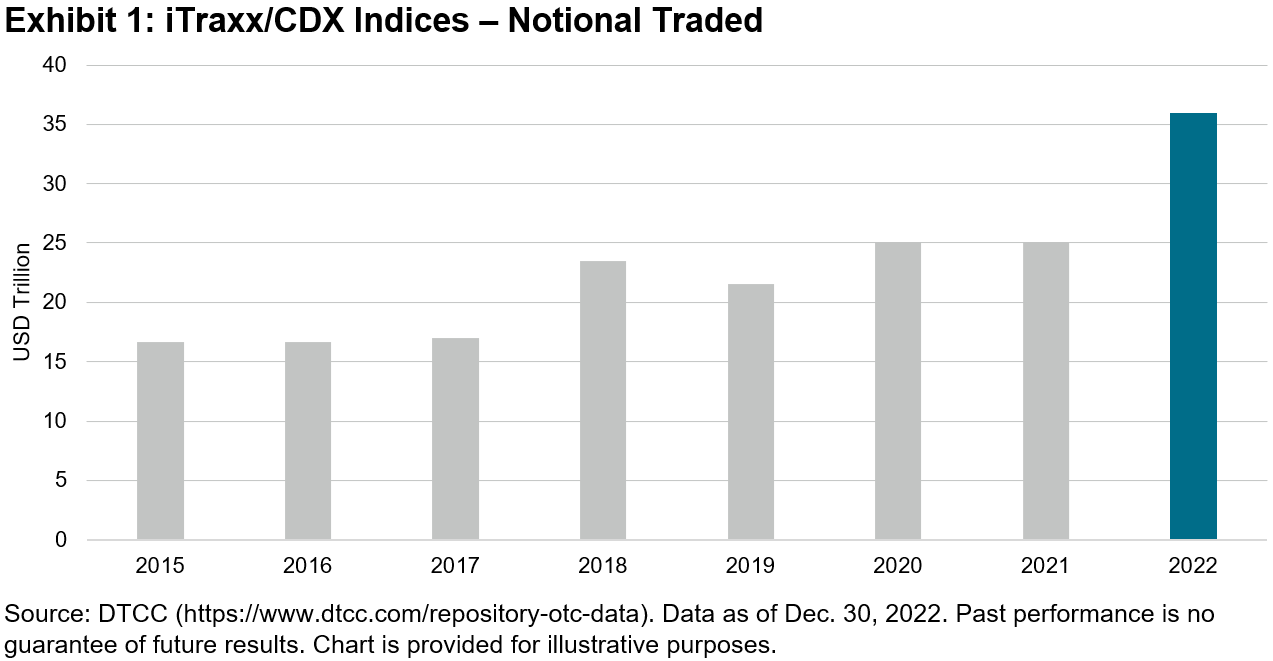

In 2022, volumes in CDX and iTraxx reached an all-time high of nearly USD 36 trillion—a 43% year-over-year increase. Such record-breaking volumes occurred as we fast approach the 20-year anniversary of the indices—CDX and iTraxx will roll into Series 40 in March and September 2023, respectively. Two decades later, the CDS indices continue to evolve with changing markets and provide the most liquid means for institutional investors to gain or hedge credit exposure. The last three years have been some of the most volatile in recent history—they have also successively set record volumes for CDS indices. When markets were volatile and fixed income liquidity became sparse, the liquidity of the CDS indices remained.

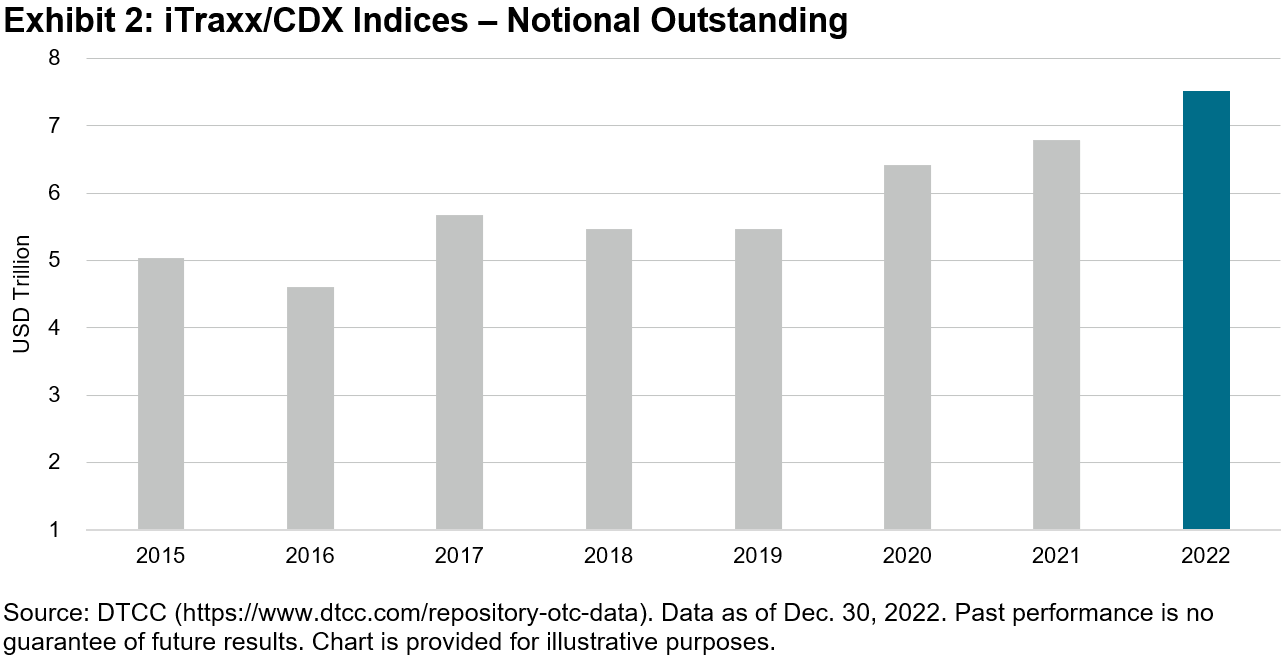

From a notional outstanding perspective, CDS exposure from the iTraxx and CDX indices has continued to climb (see Exhibit 2). Currently, there is over USD 7.5 trillion of notional outstanding in iTraxx and CDX, up from about USD 6.8 trillion at the end of 2021. The magnitude of outstanding notional points to the structural importance of the CDS indices to the global credit markets.

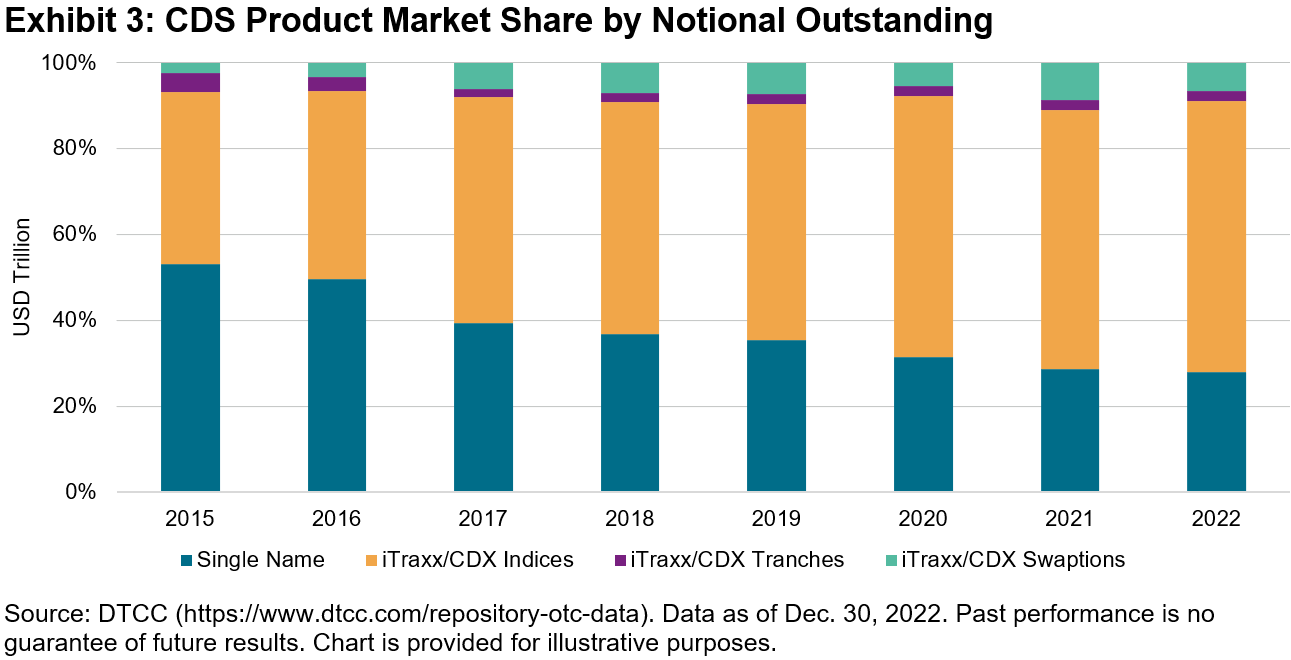

There’s also been a consistent increase in the share of overall CDS exposure that is linked to iTraxx and CDX products. As of year-end 2022, over 70% of all CDS gross notional oustanding was linked to iTraxx and CDX indices, including tranches and swaptions (see Exhibit 3).

At nearly 20 years old, with varied market participants and trillions in volumes and outstanding exposure, one might deem CDX and iTraxx to be mature. However, maturity often connotes the end of growth, which would be incorrect. Rather, the CDS indices are coming of age and continue to grow and change to reflect the needs of the market participants they serve. The indices may be getting older—but they’ve no signs of slowing down.

The posts on this blog are opinions, not advice. Please read our Disclaimers.