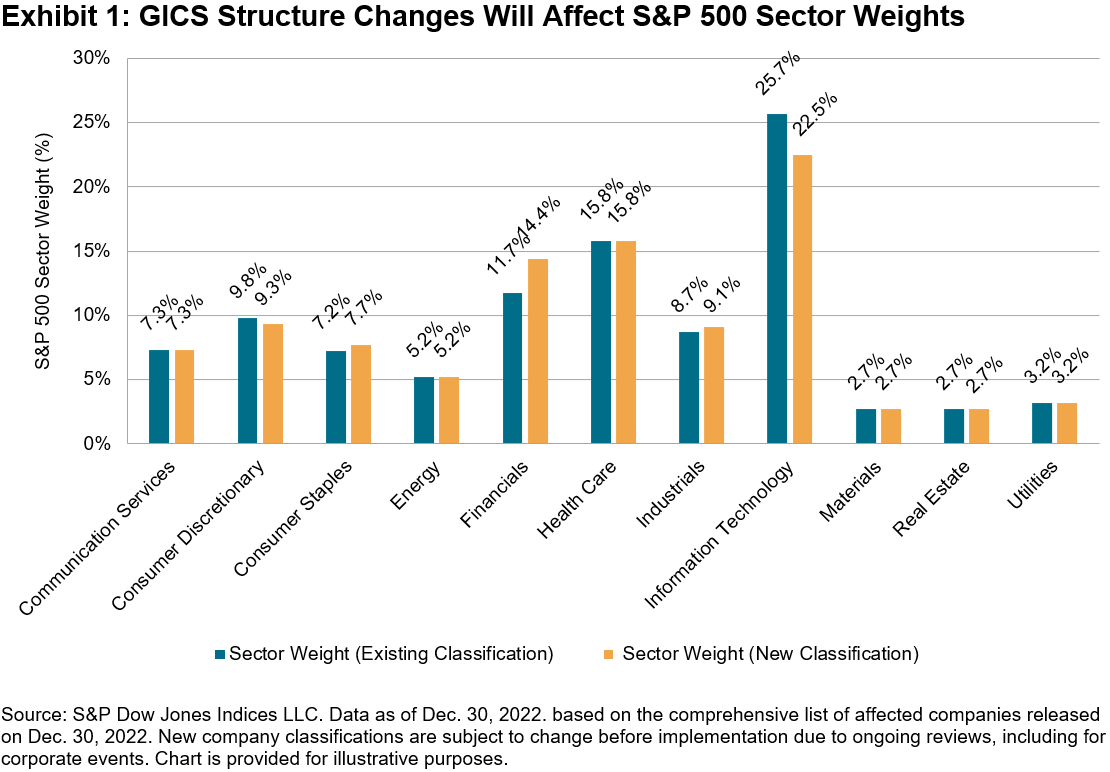

After the close on March 17, 2023, changes to the Global Industry Classification Standard (GICS®) structure will go into effect in GICS Direct and in S&P DJI’s indices. These changes will affect most sectors and will change what it means to be sector neutral. For example, Exhibit 1 compares the S&P 500 sector weights at the end of 2022 under the existing GICS structure compared to the new structure, assuming it had already gone into effect. Information Technology and Consumer Discretionary’ s weights are set to fall, while Financials and Industrials’ weights are set to increase. Here is an overview of some of the biggest upcoming changes.

GICS Is Reviewed Annually to Ensure It Continues to Reflect Global Equity Markets

Launched in 1999, GICS provides a single, consistent framework to classify companies, allowing for global sector and industry comparisons. Companies are assigned to a sub-industry according to their principal business activities, based on revenues (mainly) as well as earnings and market perception. Allocation to a sub-industry then determines—in decreasing order of granularity—membership to an industry, an industry group and a headline sector. The GICS framework is reviewed annually to ensure that the structure continues to reflect global equity markets.

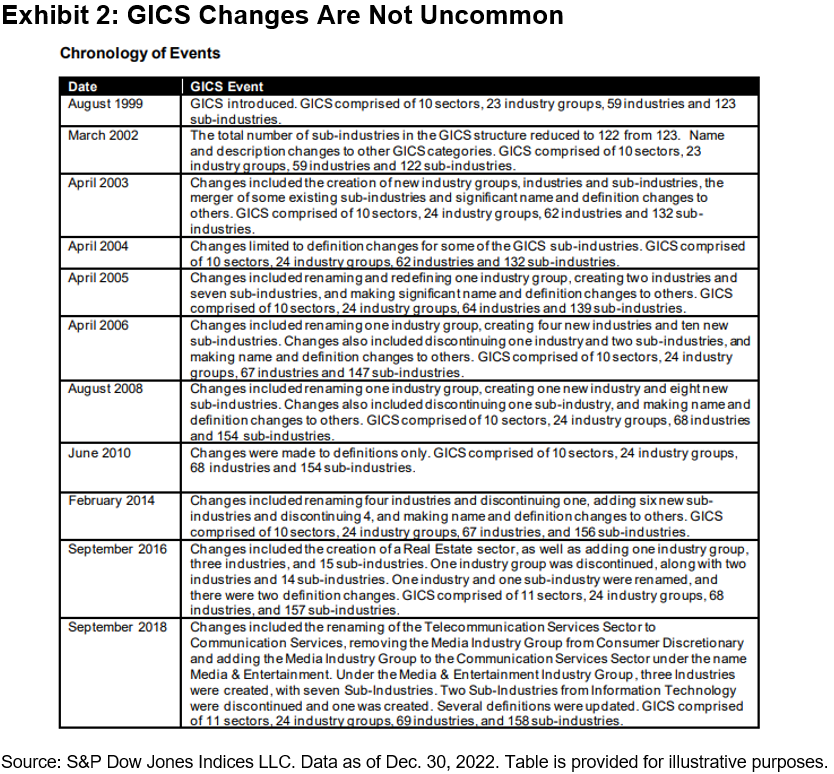

Exhibit 2 shows that there have been several updates over the years, including the creation of Real Estate as standalone sector (2016) and the renaming of Telecommunication Services to Communication Services (2018). The upcoming GICS changes will affect most GICS sectors and will leave us with 11 sectors, 25 industry groups, 74 industries and 163 sub-industries.

Updates to Consumer Discretionary and Consumer Staples Reflect the Evolution of the Retail Landscape

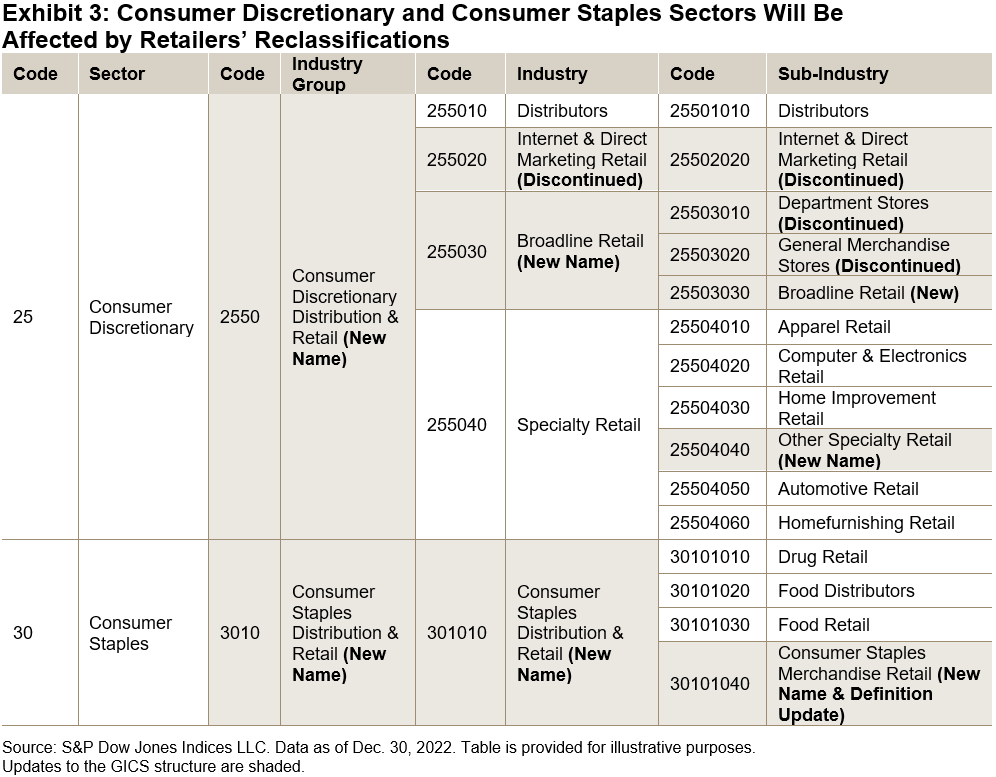

A key update in March 2023 is that retailers will be classified based on the nature of goods sold rather than according to the underlying technology used to deliver the product or service. This update reflects the fact that retailers have increasingly taken an omni-channel approach to sell their products, reducing the demarcation between existing segments.

Exhibit 3 summarizes the impact across the Consumer Discretionary and Consumer Staples sectors. For example, the General Merchandise Stores and Department Stores sub-industries will be merged into a new sub-industry called Broadline Retail, which will also capture some of the companies (e.g., Amazon and eBay) in the soon-to-be discontinued Internet & Direct Marketing Retail sub-industry. Retailers that generate a majority of revenue or earnings from staples such as food, household and personal care products will be migrated to Consumer Staples.

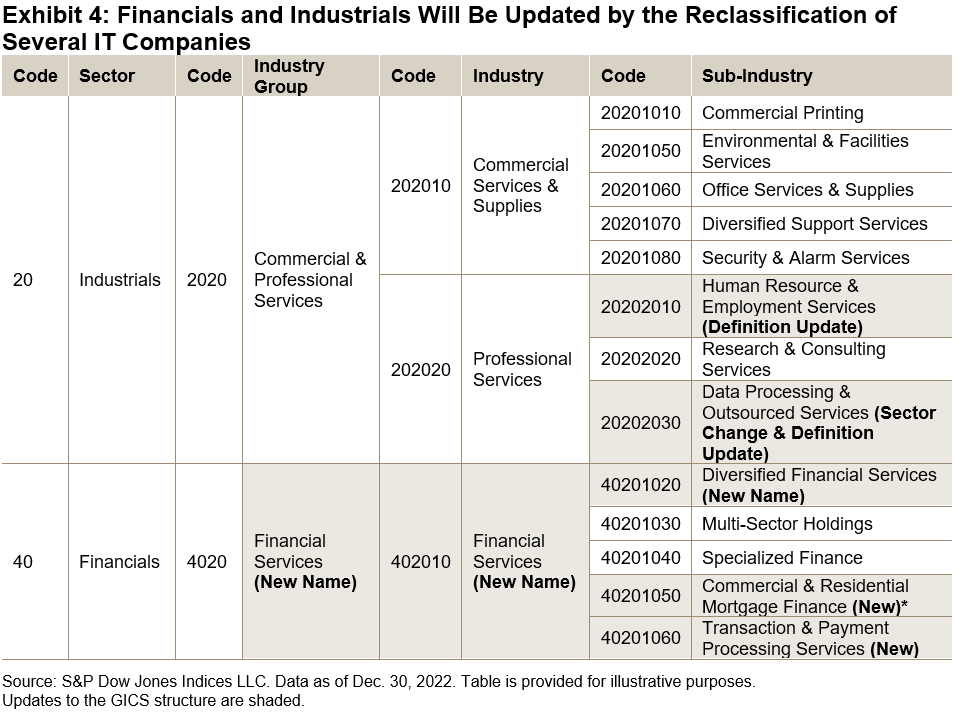

Several Information Technology Companies Will Move to Other Sectors

Information Technology will also be affected by the upcoming changes: the Data Processing & Outsourced Services sub-industry is being discontinued to reflect the close alignment with business support activities in other sectors. Companies in the sub-industry will migrate to: Industrials under a definition update or under Human Resources & Employment Services; to Financials under Transaction and Payment Processing; or to Consumer Discretionary under Hotels, Resorts & Cruise Lines.

These changes will affect indices’ sector weights. For example, the Data Processing & Outsourced Services sub-industry accounts for around 3% of the S&P 500’s weight as of January 2023, and 2 of the largest 10 S&P 500 IT companies (Visa and Mastercard) will migrate to Financials.

Elsewhere, the upcoming GICS changes update the classification of Transportation, Banks and Thrifts & Mortgage Finance, as well as providing greater granularity in the classification of Real Estate Investment Trusts (REITs).

A full overview of the latest revisions to GICS can be found here, and the current and historical GICS classifications—including definitions—can be downloaded here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

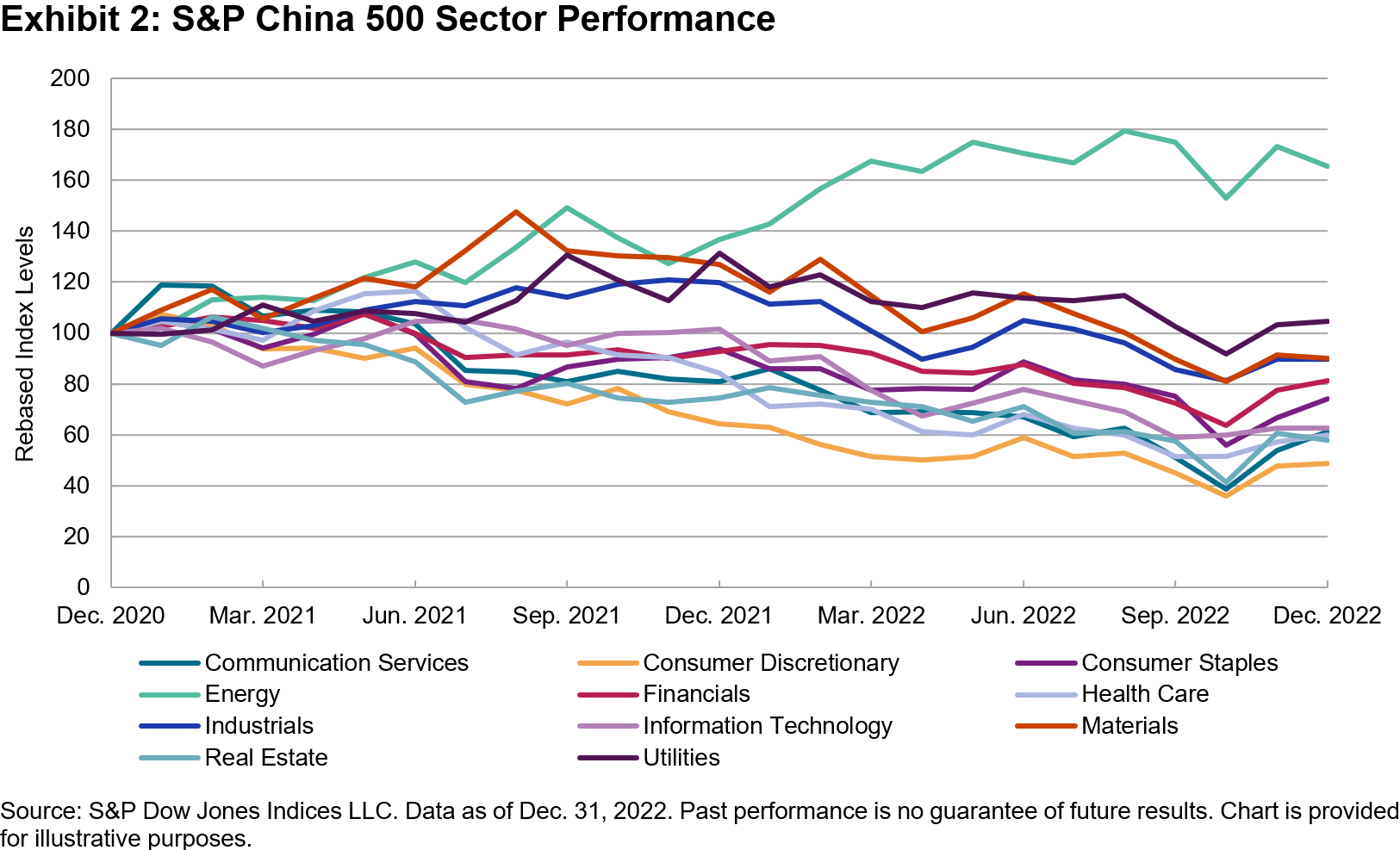

Communication Services and Health Care Led the Gains

Communication Services and Health Care Led the Gains  Valuation Metrics Remain Attractive

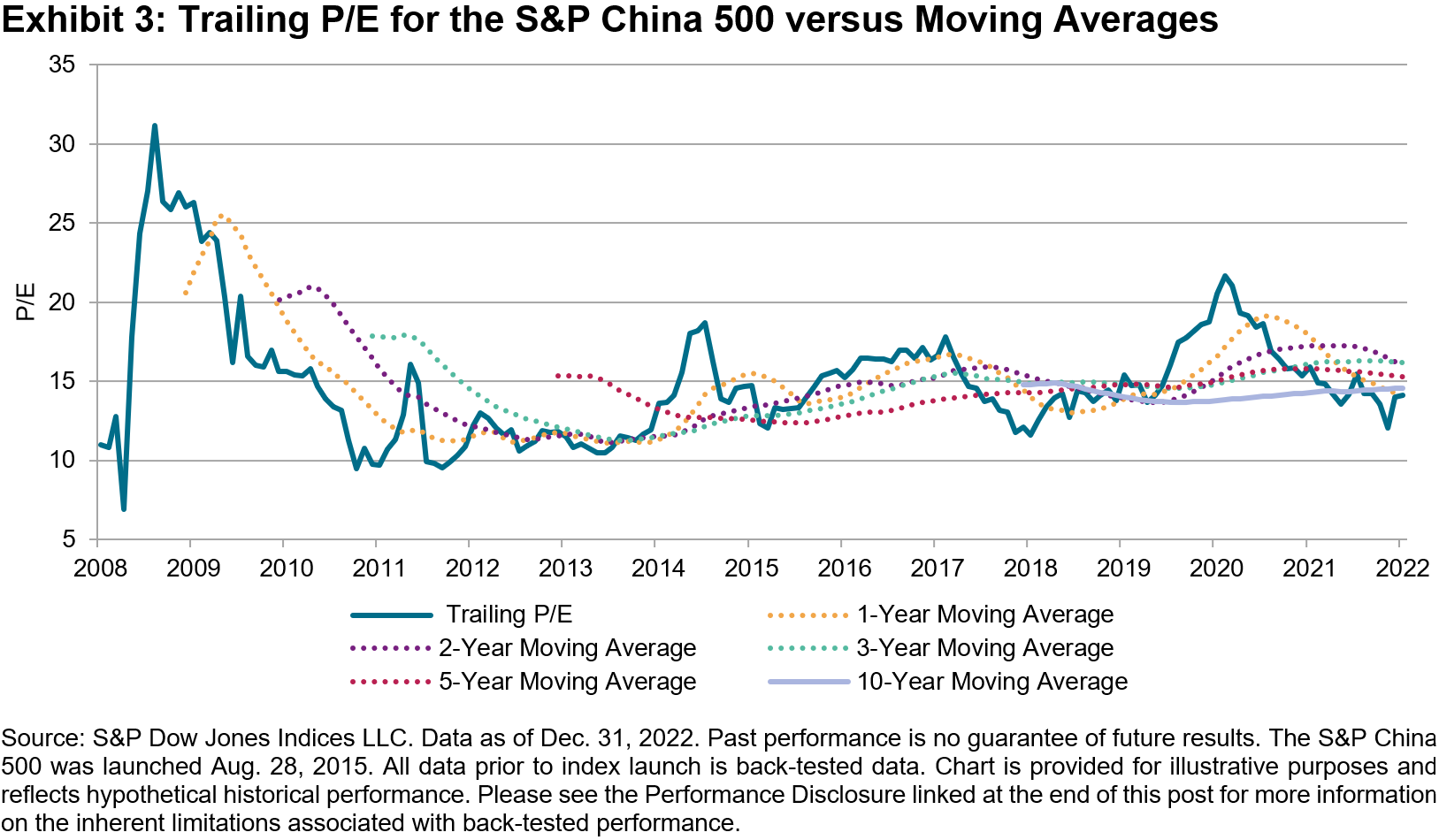

Valuation Metrics Remain Attractive The trailing P/E for the S&P Emerging BMI also increased to 13.2x, as security price gains were broad across ex-China emerging regions. The S&P China 500 index dividend yield, meanwhile, decreased from 2.58% to 2.44% on a quarterly basis.

The trailing P/E for the S&P Emerging BMI also increased to 13.2x, as security price gains were broad across ex-China emerging regions. The S&P China 500 index dividend yield, meanwhile, decreased from 2.58% to 2.44% on a quarterly basis.