Why does sector dispersion matter and how can it inform tactical approaches to sectors? S&P DJI’s Elizabeth Bebb and Invesco’s András Vig explore how sector dispersion can impact long-term asset allocations.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Examining Tactical Approaches to Sectors

The Key to the S&P 500 ESG Index’s Outperformance: Avoiding the “Worst”

Global Islamic Indices Declined Over 20% YTD, Underperforming Conventional Benchmarks in 2022

Style, Size, and Skewness

Understanding an Icon: 30 Years of Indexing the S&P 500

Examining Tactical Approaches to Sectors

The Key to the S&P 500 ESG Index’s Outperformance: Avoiding the “Worst”

Now approaching its fourth anniversary since launch, the S&P 500® ESG Index seeks to reflect many of the attributes of the S&P 500 itself, while providing an improved sustainability profile as a result of an updated ESG score.1 With live performance data covering an extraordinary period—including two bear markets on either side of a growth boom—we are presented with a real-world performance test for the index’s improved sustainability profile.

From its launch date until the end of 2022, the ESG index outperformed its benchmark, the S&P 500, by a cumulative 9.16% (impressive in the context of a benchmark that is notoriously hard to beat). But how important were higher or lower ESG-scoring constituents in generating this excess return?

To measure this, we created hypothetical ESG “quintile portfolios,” reconstituted annually by ranking the S&P 500’s constituents by their ESG score and assigning each to one of five portfolios, from highest to lowest ESG-scoring. The hypothetical cap-weighted performance of these portfolios was then calculated and used to create a Brinson-like2 “ESG attribution,” teasing out the importance of ESG exposures in the returns in the S&P 500 ESG Index.

Exhibit 1 summarizes the results of this analysis, including the average weights of the S&P 500 ESG Index and the S&P 500 in each ESG quintile (from high to low scoring), the corresponding portfolio and index returns, as well as a summary of the corresponding allocation and selection effects over the full period.3

Although an overweight in the High ESG Quintile 1 detracted from returns, the total effect from over- and underweighting across and within the ESG quintiles was positive in every other quintile. Most strikingly, underweighting the lowest ESG-scoring constituents contributed the most to the S&P 500 ESG Index’s outperformance. Specifically, the Low ESG Quintile 5 underperformed S&P 500 by -16.9%, the S&P 500 ESG Index underweighted this quintile by an average of 10.2%, and the combined effect was to generate 4.18% in excess return for the S&P 500 ESG Index.

Drilling down, Exhibit 2 compares the performance of the Lowest ESG Quintile to the S&P 500 in each calendar year included in the sample: it underperformed in three of the four calendar years represented. Exhibits 1 and 2 together show that, in short: the S&P 500 ESG Index consistently benefited from avoiding the worst-scoring constituents.

Of course, performance drivers can (and do) change over time. ESG-based attribution analysis such as these can offer insight and perspective as markets and conditions evolve. Investors seeking similar attributions for a range of our flagship indices are now able to find them—updated as of the most recent quarter-end—in S&P DJI’s recently launched Climate & ESG Index Dashboard.

Register here to receive quarterly insights and performance attributions for our range of flagship ESG and climate indices.

1 The index methodology is available at: www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-esg-index-series.pdf.

2 Similar to our previous analysis with Carbon Quintiles, the quintile portfolios are each assigned an equal number of benchmark constituents, and the impact of weighting to stocks with higher- or lower ESG scores is measured analogously to the way sector or country effects are measured by a traditional Brinson attribution.

3 Analysis carried out using S&P Capital IQ Pro.

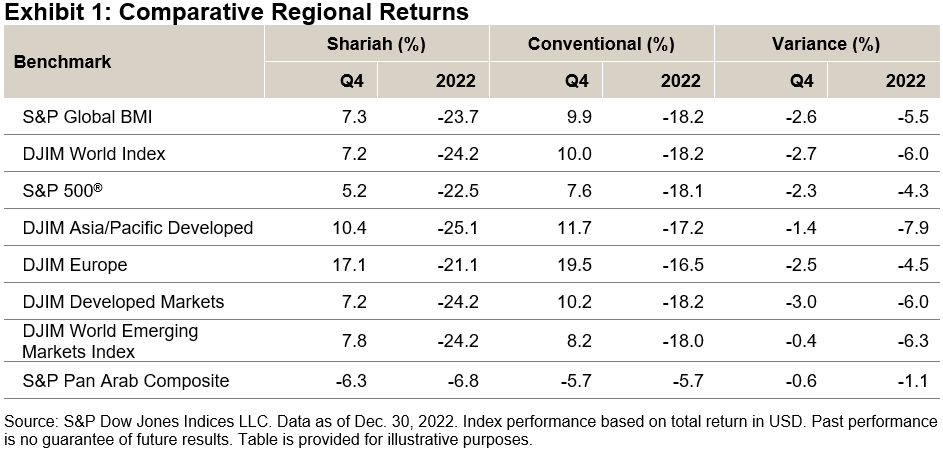

The posts on this blog are opinions, not advice. Please read our Disclaimers.Global Islamic Indices Declined Over 20% YTD, Underperforming Conventional Benchmarks in 2022

- Categories Equities, Thematics

- Tags Dow Jones Islamic Market (DJIM) World Index, equities, GCC indices, global equities, islamic benchmarks, Islamic equities, Islamic indices, MENA, MENA equities, Pan Arab, S&P Global BMI, S&P Global BMI Shariah, S&P Pan Arab Composite, Shariah, shariah index performance, thematics

Global equities partially recovered from the losses accumulated throughout the year by increasing 9.9% during Q4, as measured by the S&P Global BMI, ending 2022 with a loss of 18.2%. Meanwhile, Shariah-compliant benchmarks, including the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index, also increased during the quarter, but they underperformed their conventional counterparts by 2.6% and 2.7% respectively.

Overall regional broad-based Shariah and conventional equity benchmarks posted a positive quarter, as inflation started to cool down across the world. However, the Pan Arab region declined 5.7% in Q4, and its Shariah benchmark finished the quarter with a decrease of 6.3%.

Drivers of Shariah Index Performance in Q4 and in 2022

While 2022 was a negative year in terms of equity index performance, Q4 saw a partial recovery. Nevertheless, Shariah benchmarks underperformed their conventional counterparts during the quarter and over the year. Sector composition can provide some explanation to this quarter’s results. Higher exposure to Information Technology stocks within Islamic indices continued to weigh on returns, as IT shares didn’t benefit as much from this rally, up only 5.7% in Q4, while the sector was down 31.6% for the year.

Meanwhile, other sectors posted double-digit gains. For example, Energy went up by 19.6% in Q4 and finished the year with a gain of 45.7% but had a relatively small weight of 3.6% in the S&P Global BMI Shariah. The same can be said for Materials, which gained 14.6% during the quarter but only represented 6% of the index’s weight.

Consumer Discretionary and Communications Services were the only sectors that decreased during Q4. The impact from the latter was muted by its small weight; however, Consumer Discretionary made a negative contribution of 0.7% to the index’s return owing to its larger share of 13.3%.

Mixed Results in MENA Equities in 2022

MENA regional equities experienced mixed results in Q4 and in 2022. The regional S&P Pan Arab Composite ended the year down by 5.7%. GCC annual country performance was also mixed, with positive returns for Oman (up 25.8%) and Bahrain (up 9%), and losses in Qatar (-8.3%), Saudi Arabia (-7.2%) and the UAE (-3.7%).

For more information on how Shariah-compliant benchmarks performed in Q4 2022, read our latest Shariah Scorecard

This article was first published in IFN Volume 20 Issue 2 dated Jan. 11, 2023.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Style, Size, and Skewness

Two of the biggest reversals of 2022 compared to 2021 were the outperformance of smaller caps and the outperformance of value compared to growth. Both of these factors helped drive the S&P 500® Equal Weight Index’s recovery last year, as well as a decline in market concentration.

As sector and style exposures are not independent, another consequence of the turnaround in value’s performance and the demise of growth stocks was a seismic shift in the sector composition of our value and growth indices, resulting in record turnover for both the S&P 500 Growth and S&P 500 Value indices in their December reconstitution.

To understand better the interaction between the decline in market concentration and the shift in style index composition, we can examine concentration trends through a style lens using the Herfindahl-Hirschman Index (HHI), which reveals striking results. While S&P 500 Value’s concentration levels ticked up slightly, Exhibit 1 illustrates that after a dramatic rise since 2019, S&P 500 Growth concentration declined significantly, not seen since the burst of the tech bubble starting in 2000.

The plummeting of Growth concentration was reflected in shifts in the factor composition of the index, the most prominent of which was a reduction of the strategy’s large-cap bias. In addition, Exhibit 2, which depicts S&P 500 Growth’s factor tilts relative to the S&P 500, shows its reduced exposure to the Momentum and High Beta factors.

We can attempt to understand the implications of the increase in Growth’s small-cap exposure for active managers by analyzing the index’s distribution of returns. Exhibit 3 illustrates that in 2021, which was a stellar year for S&P 500 Growth, given the dominance of its mega caps, the distribution of the index’s stock returns was positively skewed, with the average return above that of the median, implying that only a minority of constituent stocks outperformed the index. In contrast, in 2022, S&P 500 Growth was the worst performing factor index, and the distribution of stock returns became negatively skewed as a result of the relative outperformance of smaller caps, lowering the threshold for success.

But despite this tailwind, the H1 2022 SPIVA results for growth managers were consistently discouraging across the cap spectrum, perhaps also indicating the potential inability of growth managers to tilt toward outperforming value stocks. While it remains to be seen whether managers were able to take advantage of the relatively more hospitable skewness environment during the latter part of last year, one thing is certain—the changing nature of our indices’ style, size and skewness characteristics.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Understanding an Icon: 30 Years of Indexing the S&P 500

- Categories Equities

- Tags Elizabeth Bebb, equities, ETFs, global equities, indexing, sectors, Tim Edwards, U.S. equities

How has the adoption of passive investing grown since the first U.S. ETF on the S&P 500 launched 30 years ago? S&P DJI’s Tim Edwards and Elizabeth Bebb join SPDR ETF’s Rebecca Chesworth to discuss the global role of the S&P 500.

The posts on this blog are opinions, not advice. Please read our Disclaimers.