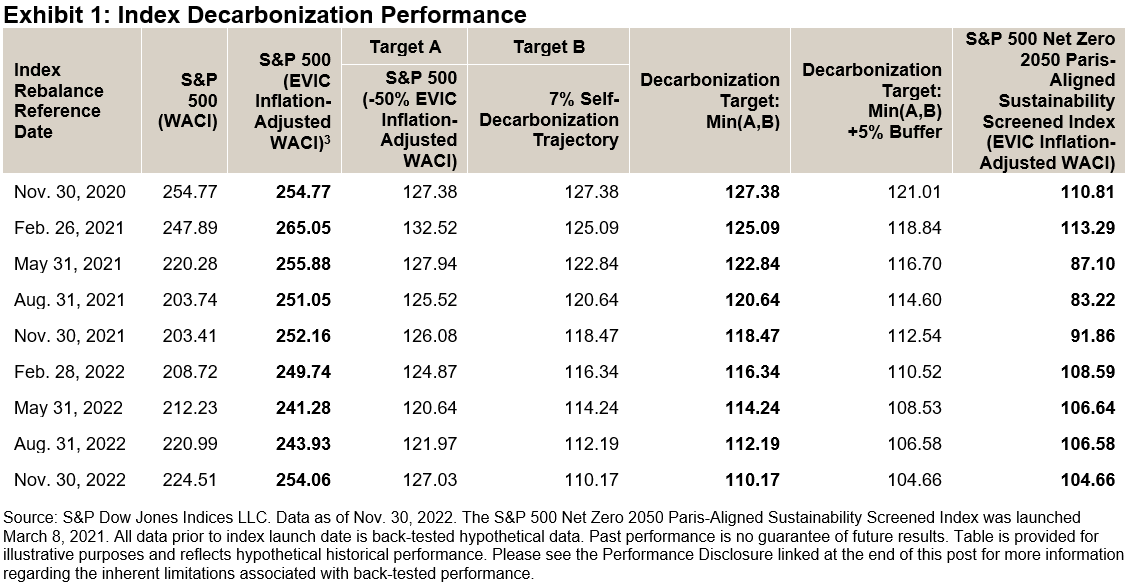

The S&P U.S. Style Indices are designed to provide broad and exhaustive exposure to the market’s value and growth segments. Our index methodology bifurcates a parent index’s market capitalization into roughly equal portions on the third Friday in December, using six measures shown in Exhibit 1.

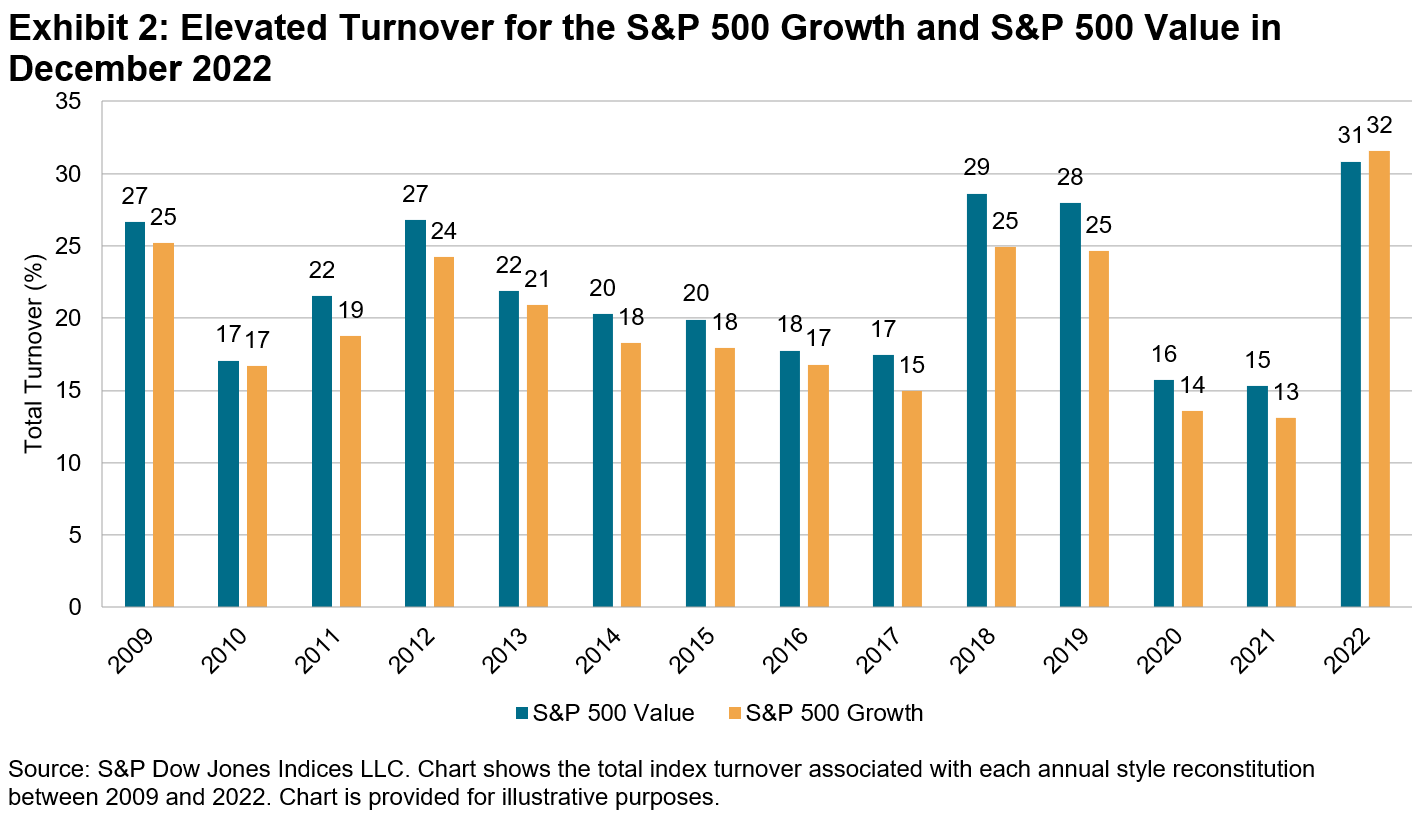

Although the composition of style indices changes every year, Exhibit 2 shows that the 2022 reconstitution saw record turnover. For example, 31% and 32% of the market capitalization of the S&P 500 Value and the S&P 500 Growth, respectively, was affected by the December 2022 style review. These one-way turnover figures were higher than for any annual reconstitution since the current style measures were adopted in 2009.

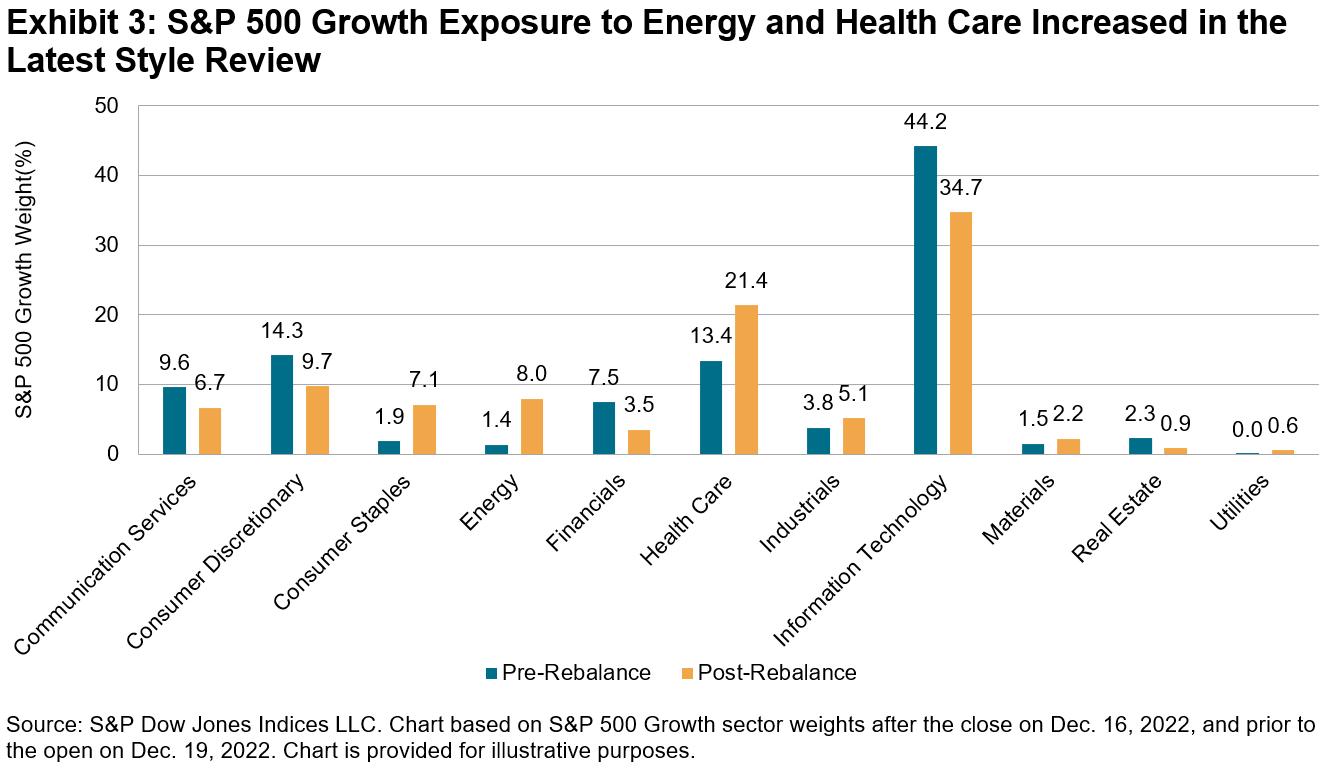

Exhibit 3 shows that there were several notable shifts in S&P 500 Growth’s sector exposures as a result of the latest style reconstitution. For example, Energy’s weight increased from 1.4% to 8.0%. Although Energy’s post-rebalance weight was not unprecedented—Energy companies accounted for more than 12% of the growth index in 2009 and 2011—the 6.6% increase in the sector’s weight was the largest increase at a style reconstitution since 2009. Health Care’s representation also rose by its biggest amount since 2009, by 8% to 21.4%, leaving the sector with its highest post-rebalance weight over the same horizon.

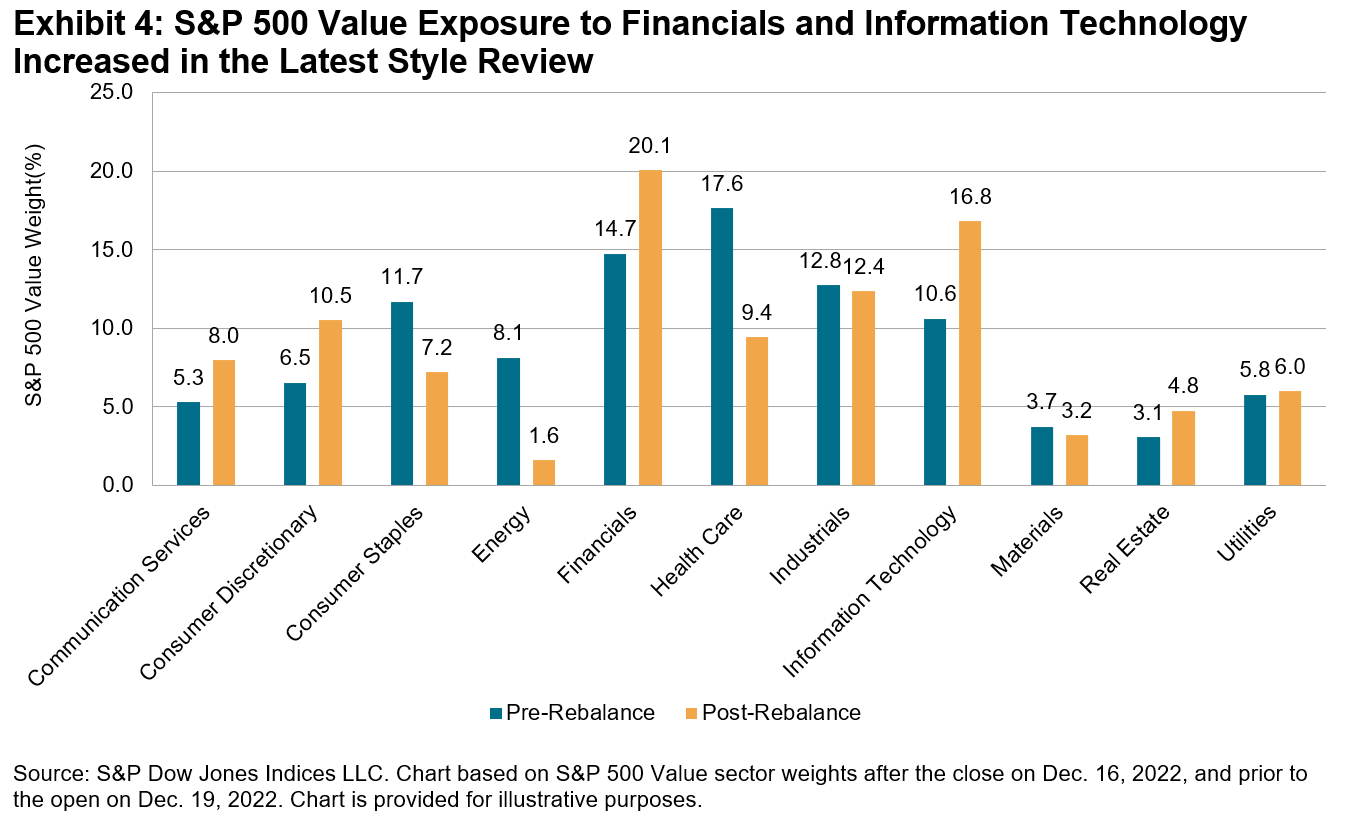

Similarly, Exhibit 4 shows large sector shifts in the S&P 500 Value. Its exposures to Financials, Consumer Discretionary and Communication Services increased by their largest margins since 2009, rising by 5.3%, 4.0% and 2.6%, respectively. And while Information Technology’s post-rebalance weight (16.8%) was not unprecedentedly high—it represented a greater portion leading into the December 2019 style review—the 6% increase in its weight was second only to its 8% increase during the 2018 rebalance.

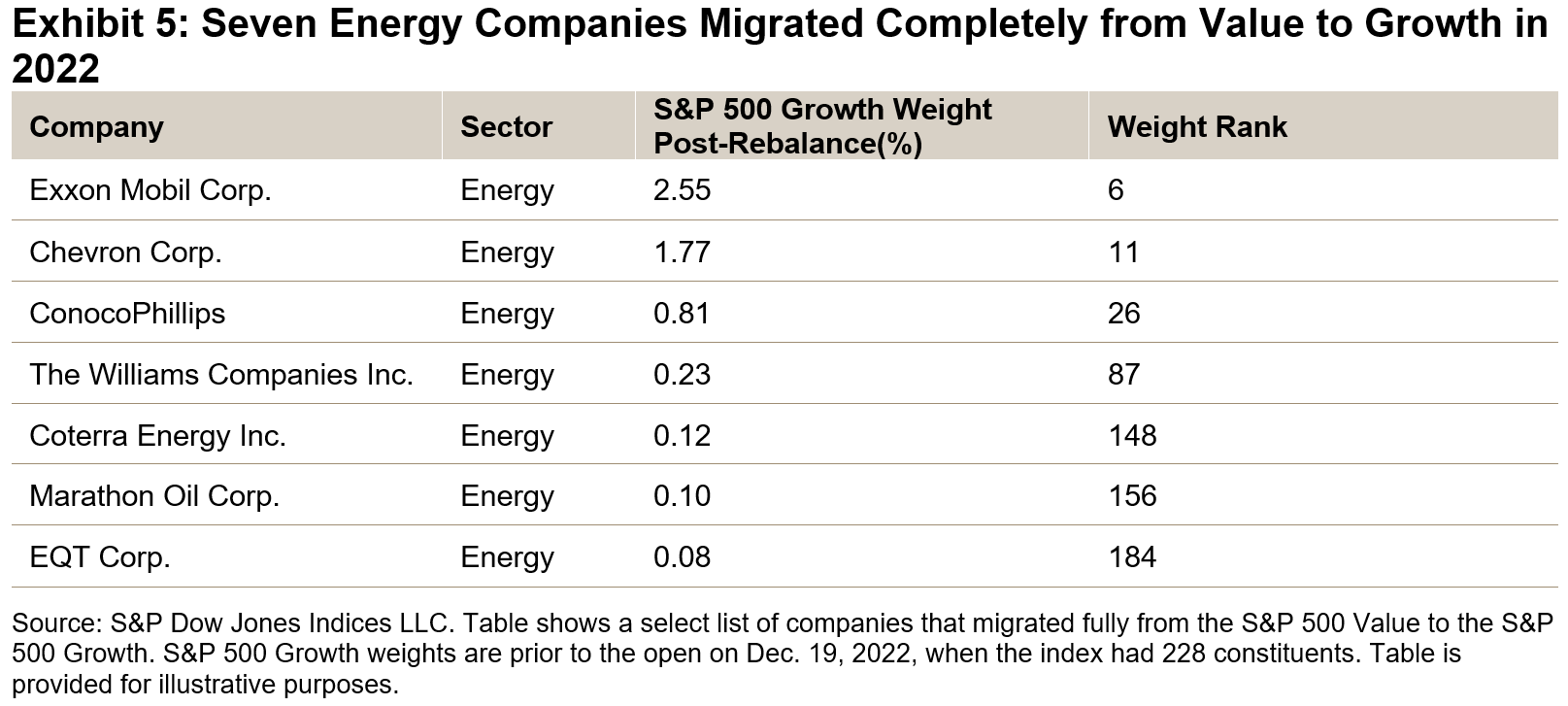

These sectoral shifts reflect the impact of 2022’s trends on companies’ latest style classifications. For example, Energy companies benefited from surging commodity prices last year, as the S&P 500 Energy sector recorded its highest calendar year total return ever (up 66%). This dynamic contributed to seven Energy companies migrating fully from the S&P 500 Value to the S&P 500 Growth. Their momentum scores were all winsorized to the highest value, and their earnings change and sales growth figures also ranked highly. Exhibit 5 shows that some of these Energy companies were among the largest in the S&P 500 Growth post rebalance.

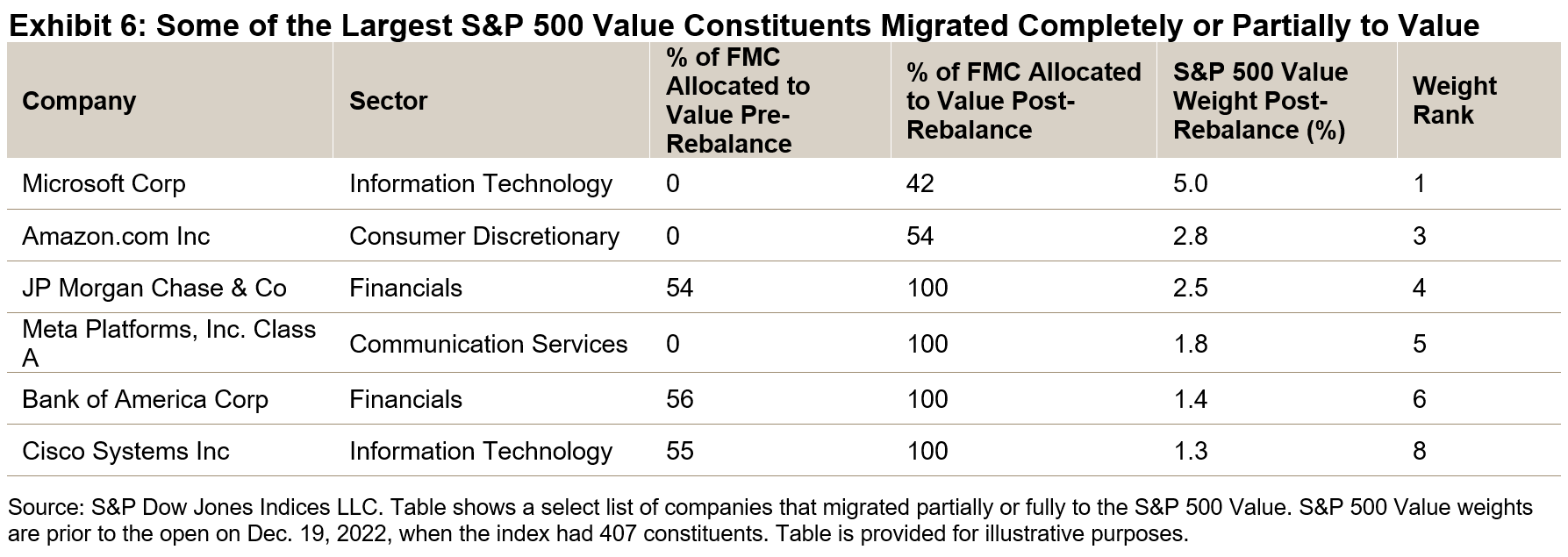

Exhibit 6 shows that 6 of the 10 largest constituents in S&P 500 Value had a greater proportion of their float market cap (FMC) allocated to S&P 500 Value after the latest rebalance. Some of the largest, historically growth-oriented companies in Communication Services, Consumer Discretionary and Information Technology were particularly affected by rising interest rates in 2022. Unsurprisingly, the momentum descriptor contributed to these companies becoming more value-oriented. Meanwhile, the earnings of several Financials companies benefited from higher interest rates, lowering their earnings-to-price ratios and thus contributing to their becoming more value oriented.

2022’s market trends affected companies’ style classifications and led to sizeable changes in sector exposures for the S&P 500 Growth and S&P 500 Value. These changes are important to understand the evolution of the indices’ characteristics and when assessing their performance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.