How do active managers in Latin America stack up to their benchmarks? Discover the key takeaways from the latest SPIVA Latin America Scorecard with S&P DJI’s Tim Edwards and Ericka Alcántara.

https://youtu.be/fAw4GaEao1Q

The posts on this blog are opinions, not advice. Please read our Disclaimers.

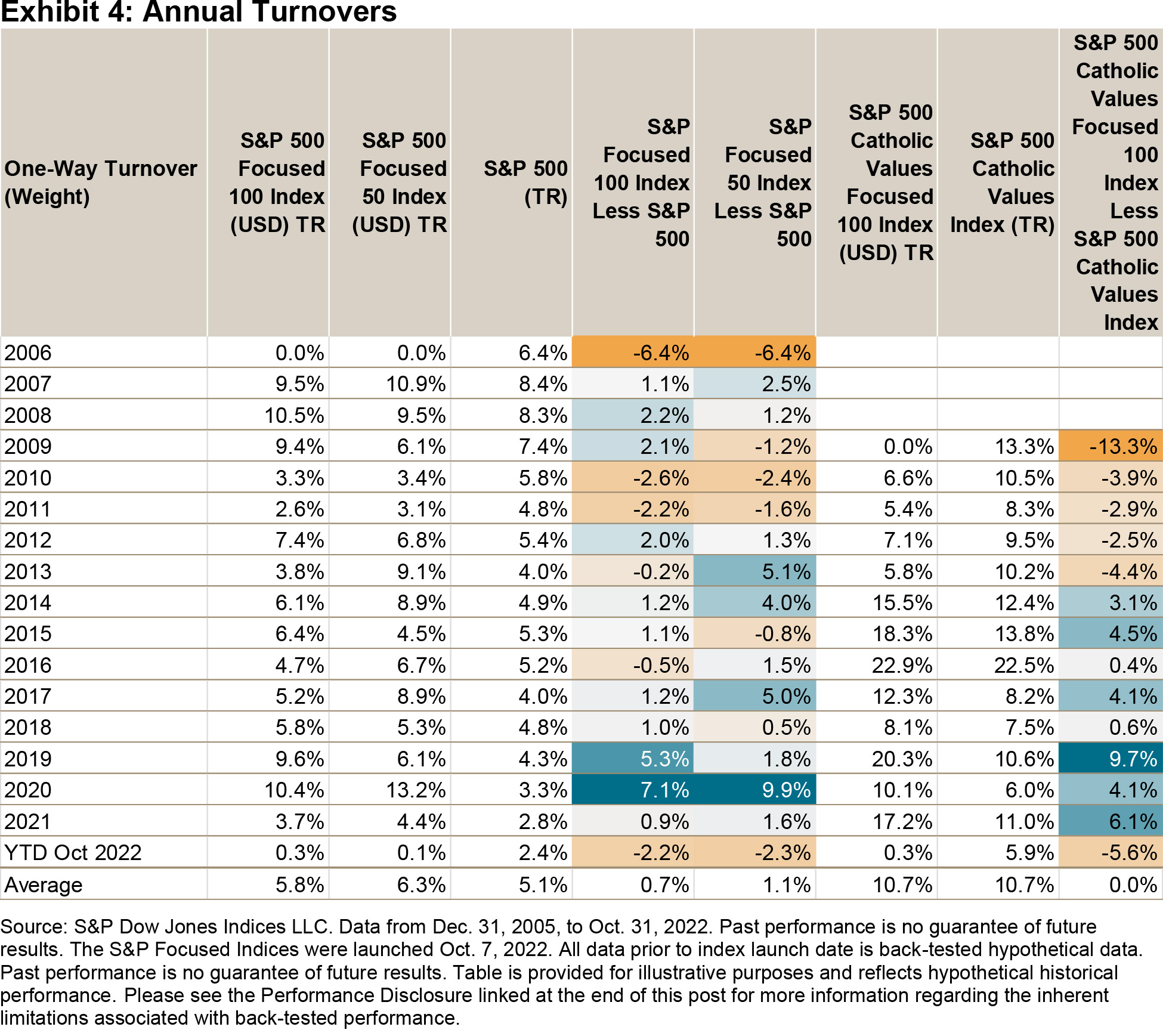

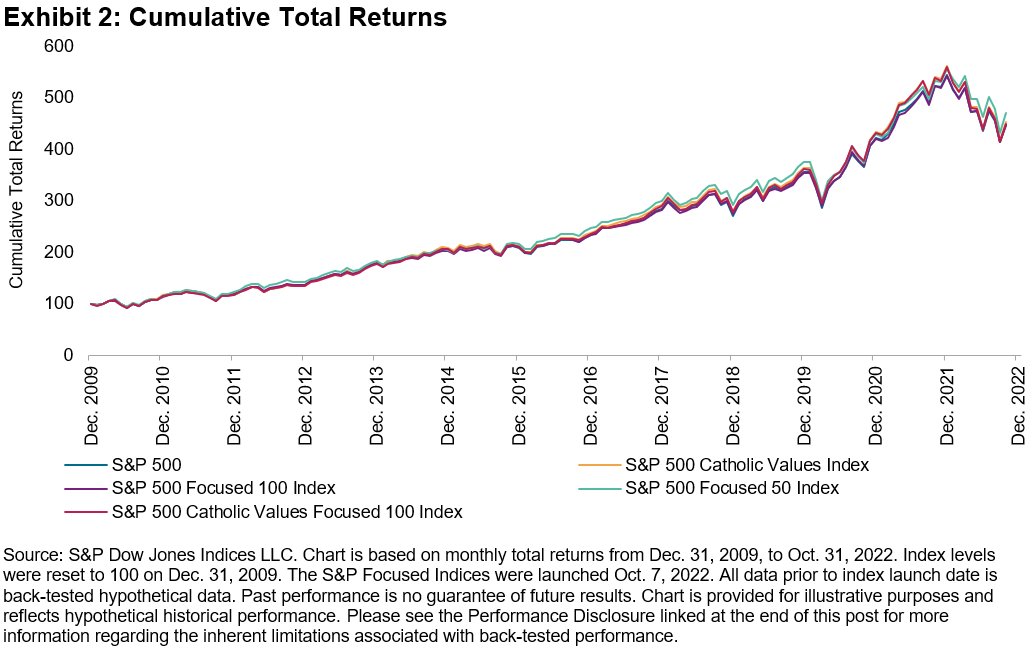

Exhibit 4 shows that the S&P Focused Indices’ construction provided similar turnover figures as their benchmarks, historically.

Exhibit 4 shows that the S&P Focused Indices’ construction provided similar turnover figures as their benchmarks, historically.