According to the second law of thermodynamics, the state of disorder or chaos of a system, also known as entropy, increases over time, defining the so-called arrow of time. Applying this analogy to Earth, is the world headed into chaos as climate change unfolds? Not necessarily. Just as entropy can decrease if useful work is put into it—think of a freezer turning water to ice—so is the world able to prevent the worst impacts from climate change.1

Measuring Temperature Alignment

S&P Global Trucost models temperature alignment by translating past emissions and forward-looking targets into a common and intuitive metric, which not only measures companies’ historical emissions at a given point in time, but also takes their (de)carbonization trajectory into account.2

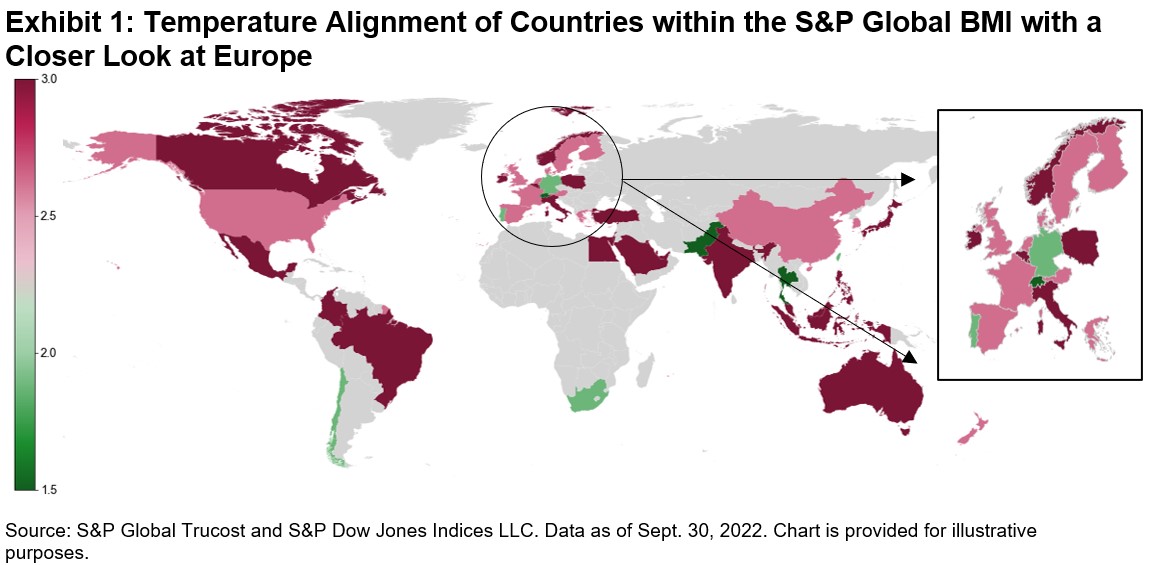

How does the transition pathway look globally? It doesn’t look bright, with few countries being aligned with below 2°C (e.g., Portugal and Germany) or below 1.5°C (e.g., Switzerland and Thailand). Most countries are lagging on the climate front, with a forward-looking pathway close to 3°C by 2100 (see Exhibit 1).

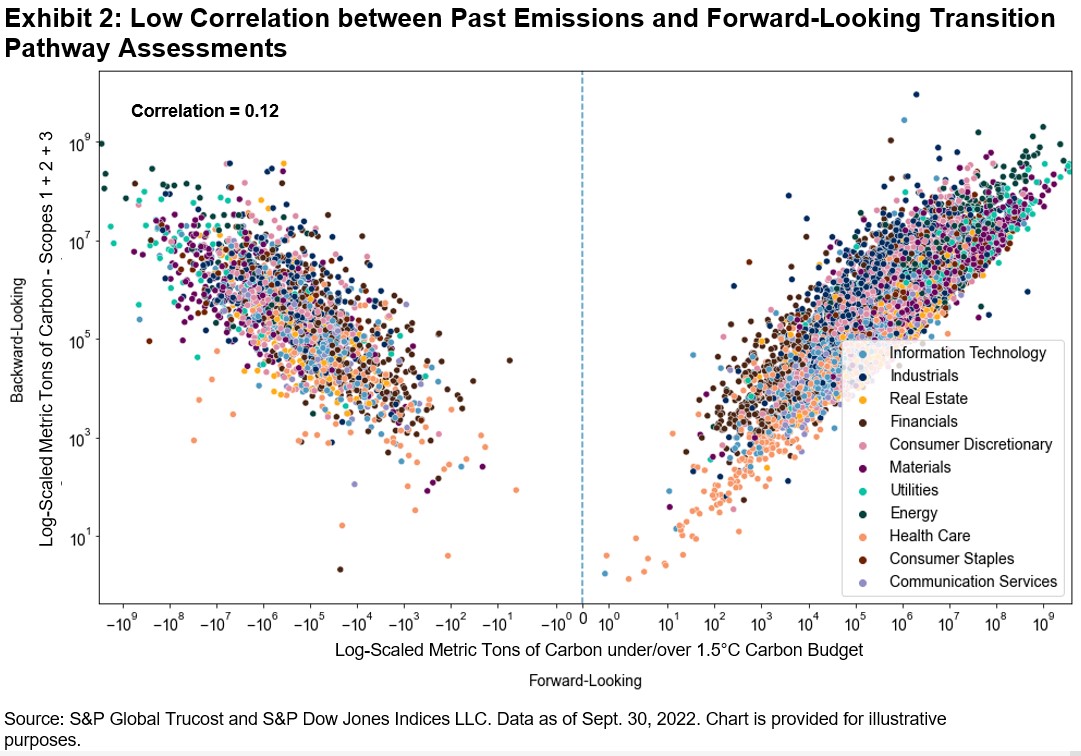

A common misconception is that low-carbon sectors are more prepared to meet the Paris Agreement’s goals of net-zero emissions by 2050. However, historical emissions and forward-looking transition pathway assessments are largely uncorrelated (see Exhibit 2). The Utilities sector provides an example: while its emissions are among the highest due to its operational nature, companies can still be well below their 1.5°C carbon budget.3 In fact, high carbon emitters can be well positioned to meet the Paris goals, where the decarbonization potential from the adoption of green technologies is highest.

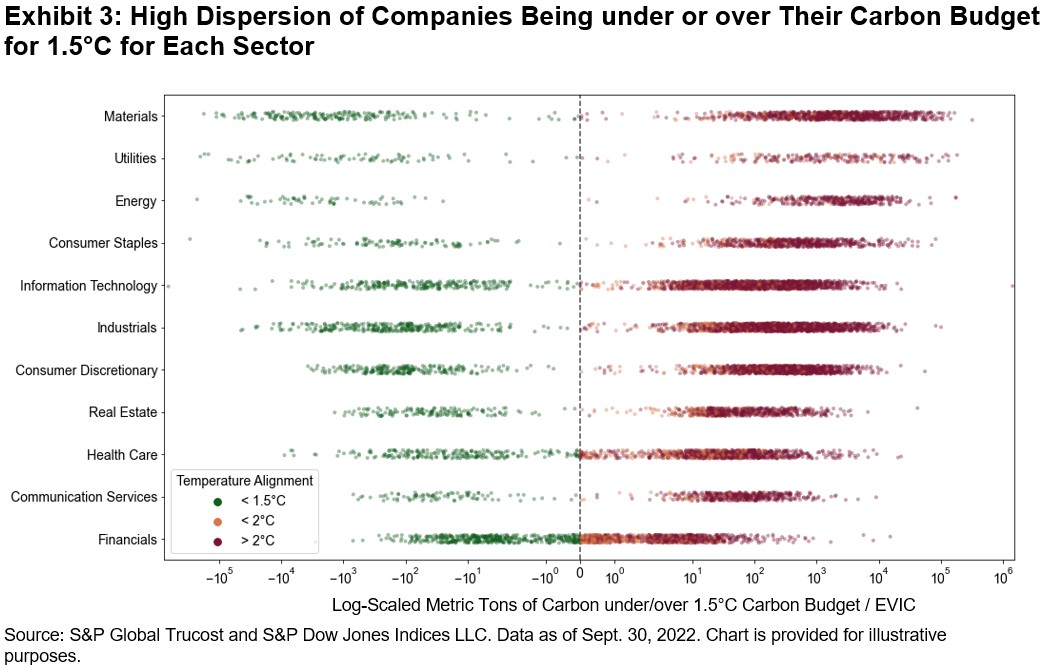

From a sectoral lens, there is a wide dispersion of companies under or above their carbon budgets (see Exhibit 3). While companies below their 1.5°C carbon budget are aligned with the Paris Agreement, as companies get further above (right of dashed line), they are likely to be aligned with higher temperature scenarios. As the increasing density of horizontal scatter points indicates, aligned companies accounted for only 25% of the universe as of Sept. 30, 2022.4

How Hot or Cold Are S&P DJI Indices?

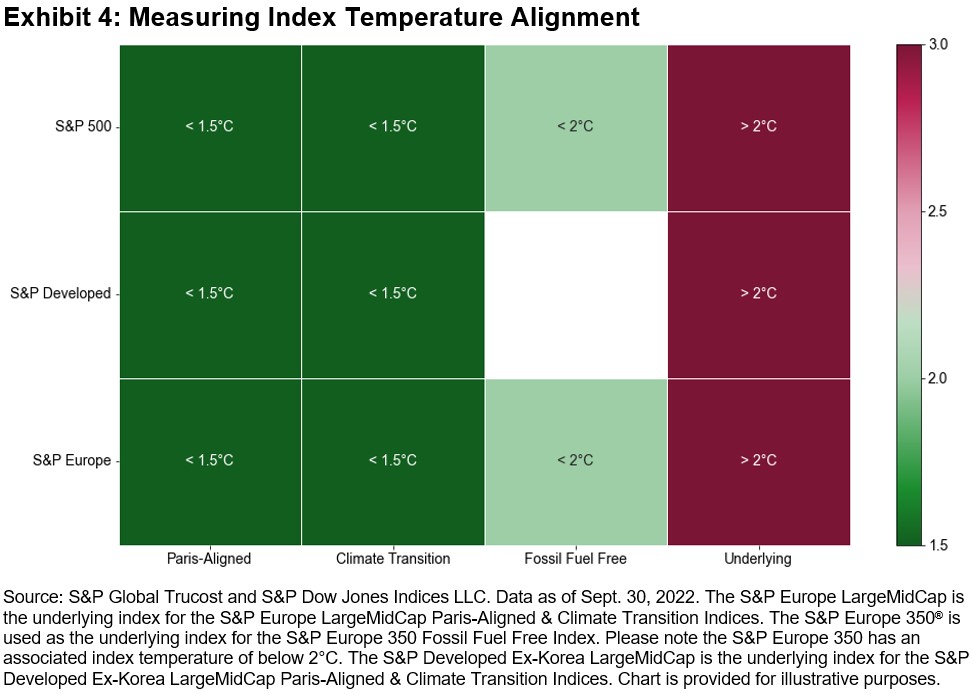

We aggregated index-level temperature assessment, focusing on climate indices (see Exhibit 4). Across universes assessed, market-cap benchmarks are incompatible with limiting warming by 2°C. Whereas excluding the fossil fuel complex (S&P Fossil Fuel Free Indices) reduces relative carbon intensity, that doesn’t necessarily translate into 1.5°C alignment. To align with net zero by 2050, index strategies must follow an absolute decarbonization approach, like the S&P PACTTM Indices (S&P Paris-Aligned & Climate Transition Indices).5 Additionally, the S&P PACT Indices incorporate forward-looking sectoral elements that make them well positioned to navigate the low-carbon transition.

Index temperature alignment offers a starting point for market participants to align their strategies with the Paris Agreement goals. While currently S&P DJI’s market-cap benchmarks fall short of meeting this target; the S&P PACT Indices, which incorporate transition pathway considerations, provide forward-looking alignment. Just as entropy can be reversed with the right inputs, indices can be used to help reduce the negative effects of climate change and align with the Paris Agreement goals of a better, less warm and more orderly future state.

1 According to IPCC’s Sixth Assessment Report, the worst effects of climate change can be prevented if global warming does not exceed 1.5°C above pre-industrial levels.

2 Analysis performed using Trucost’s Paris Alignment dataset.

3 Company’s 1.5°C carbon budget represents the allocated carbon emissions pathway to reach a 1.5°C scenario.

4 Based on the S&P Global BMI as of Sept. 30, 2022, by index weight.

5 The S&P PACT Indices follow a 7% year-over-year decarbonization trajectory, as mandated by the EU Benchmark Regulation.

The posts on this blog are opinions, not advice. Please read our Disclaimers.