For decades, traditional wisdom held that U.S. investors seeking stable income should turn to bonds. However, after more than a third of a century of declining yields, the current market environment may require a less traditional approach.

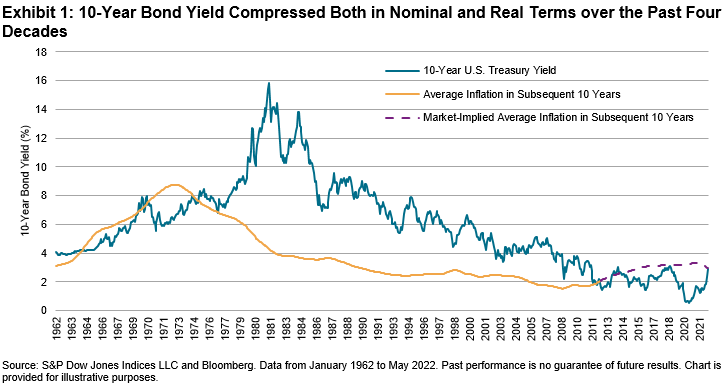

Until recently, U.S. Treasuries have been a vehicle of choice for income-seeking investors: they provide a fixed stream of payments during their full tenor, and they offer the near-perfect certainty of both coupon and principal payments (a U.S. Government default is possible, but is perceived to be so unlikely that their payments are traditionally considered “risk free” in investment literature). In the three and a half decades before 2010, these characteristics were coupled with inflation-beating real returns, too. As Exhibit 1 shows, an investor who had bought 10-year U.S. Treasury bonds in September 1981 and held them to maturity would have realized a whopping 11.5% real return per year over the bond’s lifetime.

However, the post-Volcker bond bull market, often dubbed the “Great Moderation,” compressed both real and nominal returns available on U.S. Treasuries. Starting around 2010, the real returns on 10-year Treasuries that were bought at inception and held to maturity actually turned negative. The prospects haven’t improved much by now either: based on the relative prices of inflation-protected and standard Treasury bonds, real returns for 10-year Treasury bonds bought today are expected to be around 0.[1]

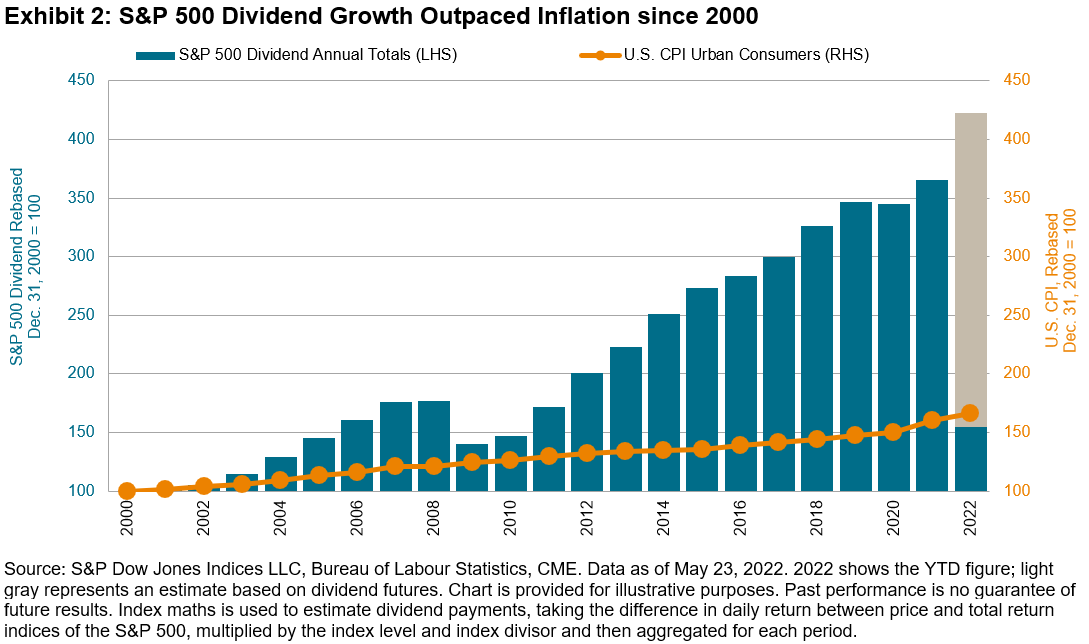

One alternative that has emerged as a potential source of regular and progressively increasing income is dividend-paying equities. Equity dividends have provided inflation protection over the medium to long term, with dividend growth surpassing the inflation rate historically. Taking a closer look at the S&P 500®, dividends paid out by index constituents rose from USD 140.1 billion in 2000 to USD 511.5 billion in 2021, corresponding to an increase by a factor of 3.7x and a compound annual growth rate of 6.4%. The rise in consumer prices, on the other hand, averaged just 2.3% over the same period. Exhibit 2 illustrates the significant spread between the dividend growth rate and the inflation rate over the past two decades, which translated to an increase of over 130% in the purchasing power of dividends paid out by S&P 500 constituents.

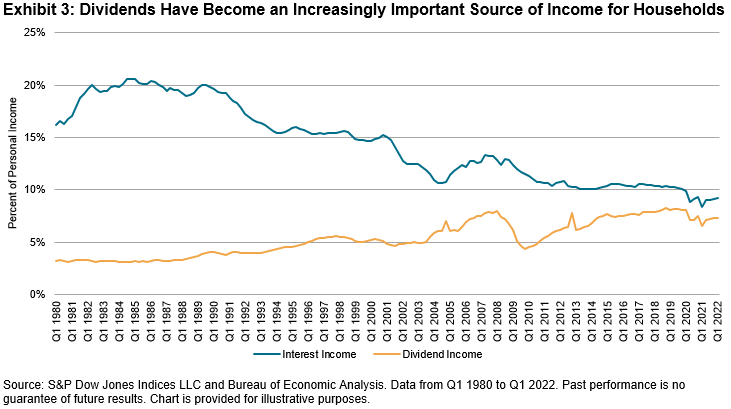

At least in aggregate, dividends have become a much more important potential source of income. But are investors taking advantage? According to data from the Bureau of Economic Analysis, dividends as a share of Personal Income have climbed from 3.2% in Q1 1980 to 7.3% in Q1 2022, whereas interest income has declined in share from 16.2% to 9.2% over the same period. In other words, dividends are indeed becoming more important, in both absolute and relative terms, to the average U.S. household’s “income statement.”

Given the significant shift in the relative importance of interest and dividend income, dividend-focused equity strategies may have an important role to play in income-focused investors’ portfolios. Dividend strategies, of course, come in many shapes and forms: S&P DJI’s range of dividend index offerings are designed to help investors achieve a variety of income goals by measuring the performance of strategies that seek to deliver high yield or stable payouts. Subsequent blogs in this series will take a closer look at some of S&P DJI’s dividend strategies available to the U.S. and international equity investors.

[1] Using U.S. inflation breakevens—calculated by subtracting the real yield of the inflation-linked maturity curve from the yield of the closest nominal Treasury maturity—as a proxy for inflation in the next 10 years. Source: S&P Dow Jones Indices LLC, Bloomberg as of May 31, 2022.

The posts on this blog are opinions, not advice. Please read our Disclaimers.