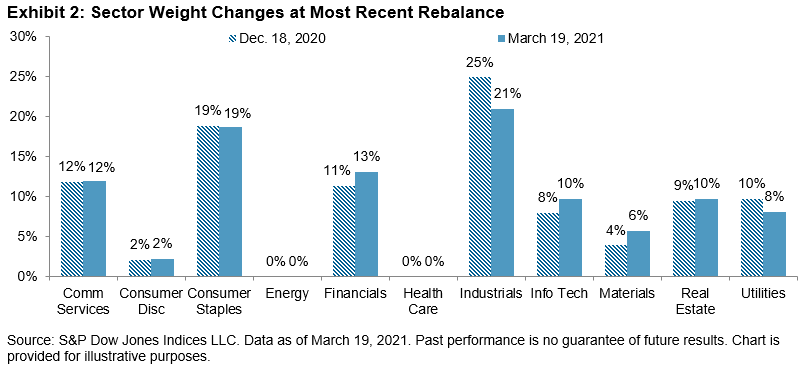

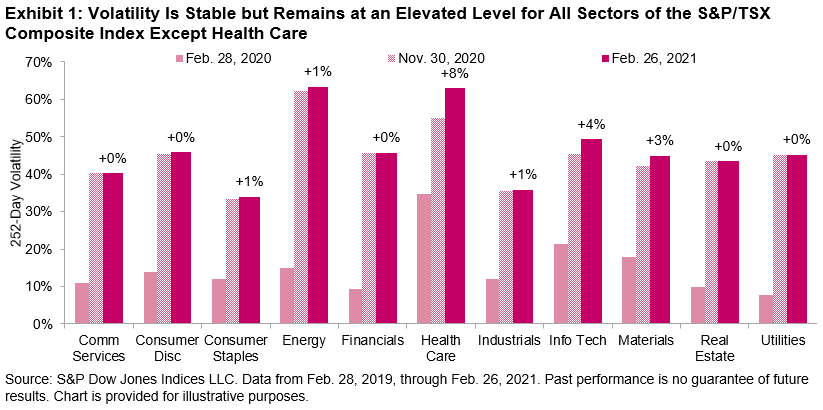

The shock that the onset of the pandemic sent through the financial markets a year ago is mostly a distant memory. The S&P/TSX Composite Low Volatility Index was up 34% for the one-year period ending March 19, 2021, lagging its benchmark index. This is not surprising given that the performance of the S&P/TSX Composite Index has been spectacular, up 60% over the past year (from the lows of the pandemic-related panic last March). Volatility at the sector level, though, remains elevated.

The S&P/TSX Composite Low Volatility Index rebalanced following the close of trading on March 19, 2021, and the changes were minor. But the results of this rebalance point to more idiosyncratic dynamics that may be happening at the stock level. Despite a 3% increase in volatility for the Materials and Information Technology sectors, the low volatility index increased weight in both sectors, while scaling back on Industrials and Utilities. There were only three name changes of the 50 companies in the index.