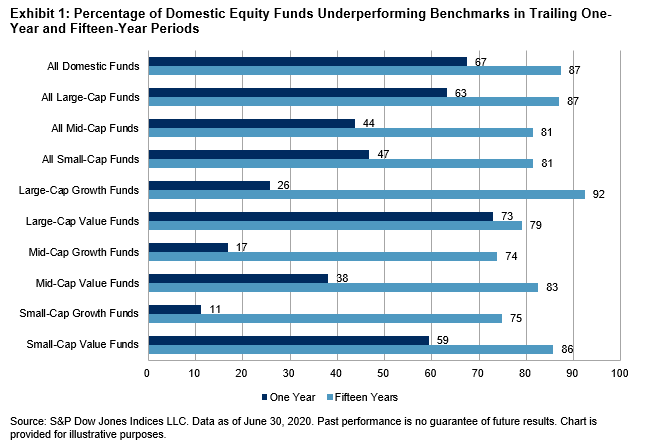

According to the SPIVA U.S. Mid-Year 2020 Scorecard, most active fund managers in the U.S. underperformed the market over the past year. Among actively managed domestic equity funds, 67% lagged the S&P Composite 1500® during the 12 months ending June 30, 2020, and the majority of active managers underperformed their benchmarks in 11 out of the 18 categories of domestic equity funds.

The past year was marked by performance divergence and extreme volatility. For example, while the majority of large-cap and multi-cap funds lagged their benchmarks, mid-cap and small-cap active funds performed better. Similarly, growth funds led across all capitalization segments in the one-year period, while value funds in general continued to lag their benchmarks over all time horizons (see Exhibit 1).

Despite divergent results over the one-year horizon, median fund managers across all domestic equity categories underperformed their benchmarks over the past 15 years. This is not surprising–our latest Fleeting Alpha report shows that, even if an active fund manages to beat the benchmark in one period, it is difficult to keep its positive excess return in the following years. In longer investment horizons, the standard deviation of active fund returns tends to diminish; eventually, a fund’s returns start to resemble a normal distribution with its median below the benchmark’s return.

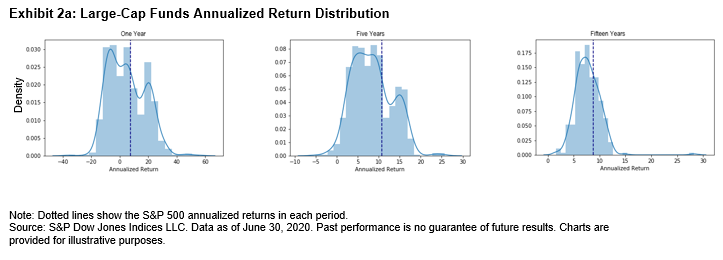

Taking large-cap funds as an example, Exhibit 2a plots the distribution of annualized fund returns in the past 1-, 5-, and 15-year periods, with the S&P 500® annualized returns shown as the dotted lines. In the one-year period, most funds can be sorted into discrete and distinct groups of winners and losers relative to the benchmark. However, as the investment horizon lengthens, these two groups gradually converge and the returns from all funds resemble a continuous normal distribution despite its long tail and skew. Exhibit 2b further confirms that the standard deviation of fund returns decreases steadily as the investment horizon lengthens. In all periods, the average and median large-cap managers underperformed the benchmark.

Data from the SPIVA Mid-Year 2020 Scorecard are clear: short-term outperformance tends not to persist. The most likely path for short-term outperformers is convergence to mediocrity, as most actively managed mutual funds fall short of benchmark returns in the long run.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

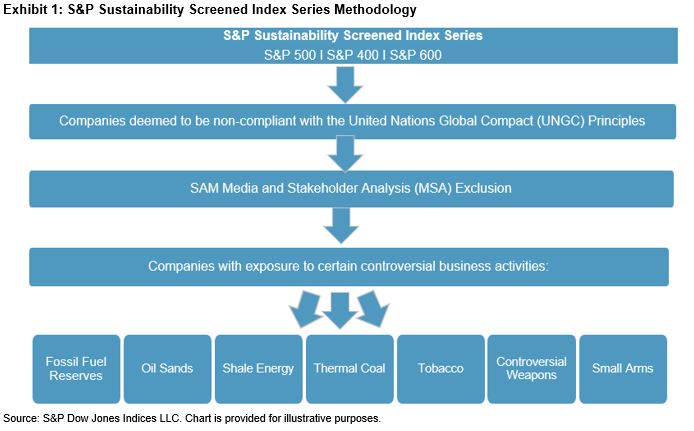

In addition to these key business involvement screens, companies are also assessed based on their compliance with the principles of the U.N. Global Compact.3 Companies that do not act in accordance with the associated standards, conventions, and treaties are ineligible for the index. The addition of this screen allows for the index to account for companies with violations linked to human rights, labor, environment, and corruption abuses.

In addition to these key business involvement screens, companies are also assessed based on their compliance with the principles of the U.N. Global Compact.3 Companies that do not act in accordance with the associated standards, conventions, and treaties are ineligible for the index. The addition of this screen allows for the index to account for companies with violations linked to human rights, labor, environment, and corruption abuses.