Although 2020 was a year that offered ample opportunities for stock pickers to shine, most Canadian active fund managers in five of the seven categories tracked by the SPIVA® Canada Year-End 2020 Scorecard underperformed their benchmarks over the past year.

The Canadian equity market was not spared from the COVID-19 shock in 2020. Nevertheless, major local equity benchmarks finished positive, with the exception of the S&P/TSX Canadian Dividend Aristocrats® Index. Among actively managed Canadian equity funds, 88% lagged the S&P/TSX Composite Index. Canadian Small-/Mid-Cap Equity funds had a banner year, as just 22% failed to beat the S&P/TSX Completion Index. Canadian Dividend & Income Equity funds took second place among fund categories, with just 44% lagging the S&P/TSX Canadian Dividend Aristocrats Index.

Results were more uniform and bleaker over longer horizons. At least 84% of funds underperformed their benchmarks in all but one category over the past decade.

Equity funds looking outside of Canada performed better than their domestic-focused peers on an absolute return basis, but still generally underperformed the benchmarks. Thanks to a strong rebound in the U.S., equity funds there posted the highest returns over the past year among all categories, with a 13.6% gain on an equal-weighted basis. However, this was still below the 16.3% return of the S&P 500® (CAD), and 69% of the funds still fell short of their benchmark.

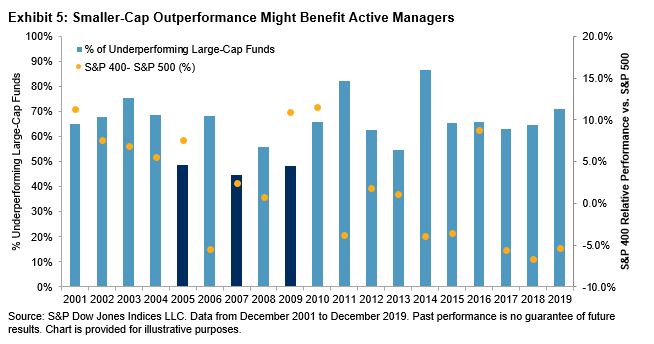

Larger funds in Canada tended to outperform their smaller counterparts, as 22 of the 28 results showed higher asset-weighted returns across the seven fund categories and four investment horizons in the report.

The data from the SPIVA Canada Year-End 2020 Scorecard show disappointing performance of active funds relative to their respective benchmarks. Over the past decade, most funds in all categories failed to beat index investing.

The posts on this blog are opinions, not advice. Please read our Disclaimers.