Over the past decade, we witnessed the longest economic expansion in history. During that time, risk appetite spiked, elevated largely by deflated interest rates around the globe in the wake of the Global Financial Crisis, as accommodative monetary policy lifted many investors up the risk curve. As in previous crisis periods, elevated risk asset valuations could not hold; today, those levels face the sobering reality of a global pandemic, which has driven global equities into a bear market and threatens to cause a global recession. This drop was different than others before it, however, as it took only a month for stock prices to fall from all-time highs to a deep trough, making it the fastest decline into bear market territory for many major equity benchmarks in history. Investors are now struggling through a rapid reset, looking for the bottom while curtailing their risk appetite.

Though some market pundits repeatedly predicted the collapse of the stock market over the past decade only to be proven wrong time and again with each new market high, during the 2010s, we witnessed one of the least-volatile eras in modern financial markets.

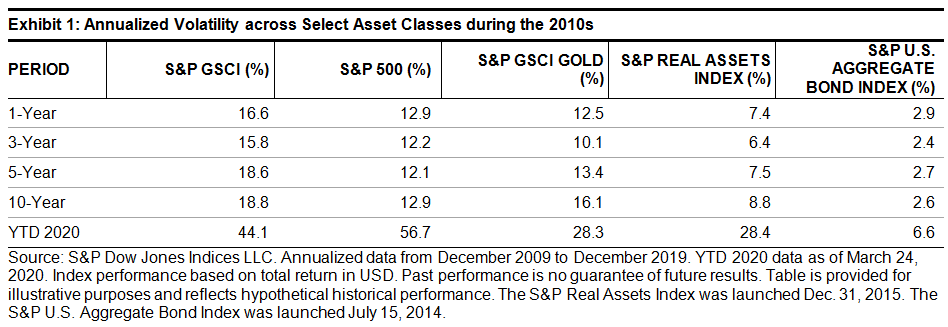

There was one asset class that remained volatile during the past 10 years, however. Commodity market volatility has nearly always been more elevated than that of equities markets, and for good reason: commodities are not anticipatory assets, and spot prices largely reflect the current physical supply and demand dynamics of each underlying commodity. Exhibit 1 highlights that difference in volatility; of particular note is the volatility over the longer term, where the S&P GSCI and S&P GSCI Gold were clearly more volatile than equities or fixed income.

So far in 2020, volatility has spiked across nearly all asset classes. If this holds, these levels would be at least double anything we’ve seen over the past 10 years. While volatility for commodities has jumped this year, due to movements in the oil market, U.S. equity and real asset volatilities ticked up even more in the panic.

Though there has already been a seismic shift in broader risk sentiment across all asset classes, within the commodities market, we may see additional risk re-evaluation. In general, there has been a supply glut across the board for many years, which has depressed price levels. While the primary focus since the start of the COVID-19 pandemic has been on the scale and longevity of demand destruction, supply disruptions will increasingly become a factor in price discovery. Companies involved in the production of commodities are pulling back in response to government-enforced shutdowns and collapsing prices. This is most apparent in the U.S. energy space, where cutbacks in new projects will start to affect oil supply by the end of 2020. The S&P GSCI Petroleum is down a staggering 58.3% YTD, reflecting these depressed price levels, and it is not yet pricing in a supply shortfall. Forced shutdowns are not only affecting the energy sector but metals and mining companies as well. While current stockpiles may meet immediate demand in the short run, once global supply chains start moving again, there will likely be a short- to medium-term drag on supply while firms in many commodities markets restart their operations.

Are we finally at a moment of peak commodities supply? It is impossible to say for certain in the face of an unpredictable pandemic and unprecedented monetary and fiscal stimulus. However, global commodities supply has and will likely continue to fall in the near term, and as levels of economic activity start to pick up, supply will play an increasingly important role in the price discovery process.

The posts on this blog are opinions, not advice. Please read our Disclaimers.