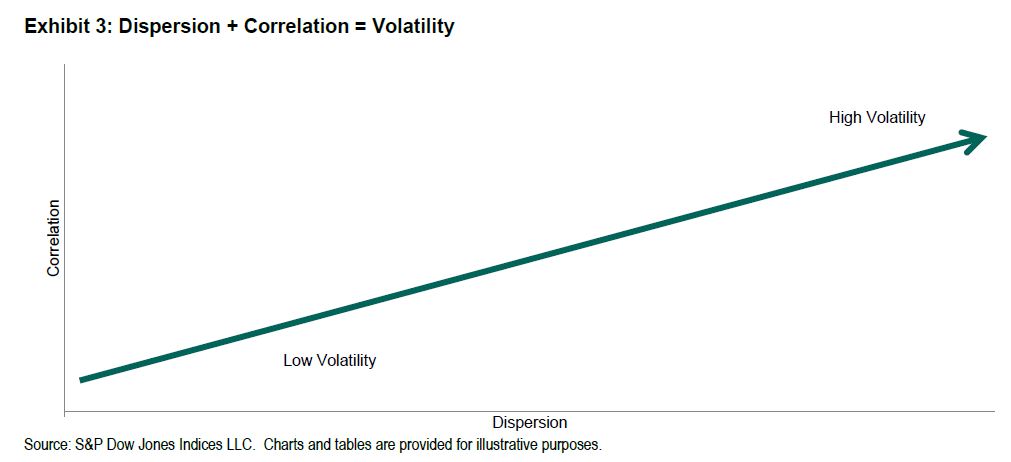

Market volatility is a function of both dispersion and correlation, as shown in this schematic:

Dispersion measures the degree to which the components of an index perform similarly. If the components are tightly bunched, dispersion will be low and, other things equal, the index’s volatility will be low. Correlation is a measure of timing; it measures the tendency of index components to rise or fall at the same time. If the components tend to move together, correlation will be relatively high, and volatility will rise. If component moves tend to offset, correlation and volatility will be lower. In terms of our simple schematic, the farther from the origin an index is, the higher its volatility will be.

Dispersion measures the degree to which the components of an index perform similarly. If the components are tightly bunched, dispersion will be low and, other things equal, the index’s volatility will be low. Correlation is a measure of timing; it measures the tendency of index components to rise or fall at the same time. If the components tend to move together, correlation will be relatively high, and volatility will rise. If component moves tend to offset, correlation and volatility will be lower. In terms of our simple schematic, the farther from the origin an index is, the higher its volatility will be.

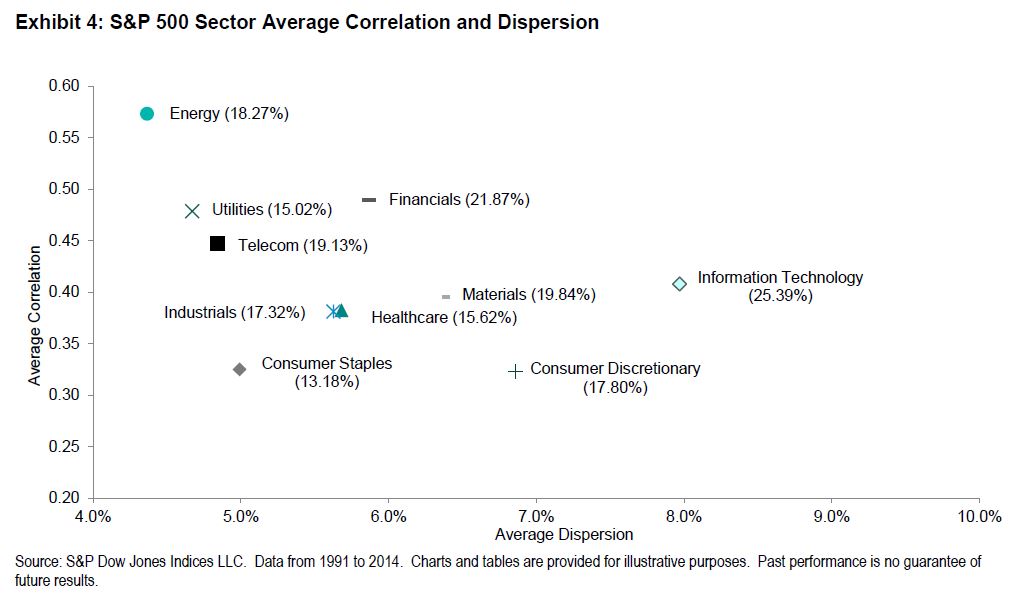

Dispersion, correlation, and volatility can be measured at the market index level, of course, but can equally well be measured at a finer level of granularity. Below we’ve graphed these metrics for each of the 10 sectors of the S&P 500:

We immediately notice that the highest volatility sectors tend to be the farthest from the origin and the lowest volatility sectors the closest — confirming our intuition about the interaction of dispersion and correlation. But these data — ironically, perhaps, derived entirely from passive benchmarks — can also provide some useful guidance for active investors.

We immediately notice that the highest volatility sectors tend to be the farthest from the origin and the lowest volatility sectors the closest — confirming our intuition about the interaction of dispersion and correlation. But these data — ironically, perhaps, derived entirely from passive benchmarks — can also provide some useful guidance for active investors.

First, since dispersion measures the potential benefit of stock selection, an active stock picker might wish to concentrate his efforts on high-dispersion sectors. There is, e.g., more potential benefit to choosing among technology stocks than among energy companies or utilities. If analytic resources are scarce, in fact, there’s an argument to be made for simply indexing the low-dispersion sectors. (We know at least one major institutional investor which does exactly that.)

Second, the nature of the most relevant analytic input differs across sectors. For low-dispersion, high-correlation sectors, the most important decision is the sector call, not individual stock recommendations. The returns of the constituents of these sectors tend to cluster relatively tightly, so stock selection is of relatively little value. On the other hand, where correlations are high, it means that most stocks in the sector move up and down together. A correct sector call will be reflected more consistently across all sector components.

An analyst who follows utilities or energy would be well advised to spend most of his time and effort deciding whether to be in or out of the sector. An analyst who follows technology or healthcare may be better off trying to separate the sectoral wheat from the sectoral chaff. Dispersion and correlation not only provide insight into the volatility of sector returns, but offer guidance for active analysts as well.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices, LLC. Data as of April 2, 2015. Past performance is no guarantee of future results. Charts and tables are provided for illustrative purposes and may reflect hypothetical historical performance. Please see the Performance Disclosures at the end of this document for more information regarding the inherent limitations associated with back-tested performance.

Source: S&P Dow Jones Indices, LLC. Data as of April 2, 2015. Past performance is no guarantee of future results. Charts and tables are provided for illustrative purposes and may reflect hypothetical historical performance. Please see the Performance Disclosures at the end of this document for more information regarding the inherent limitations associated with back-tested performance.