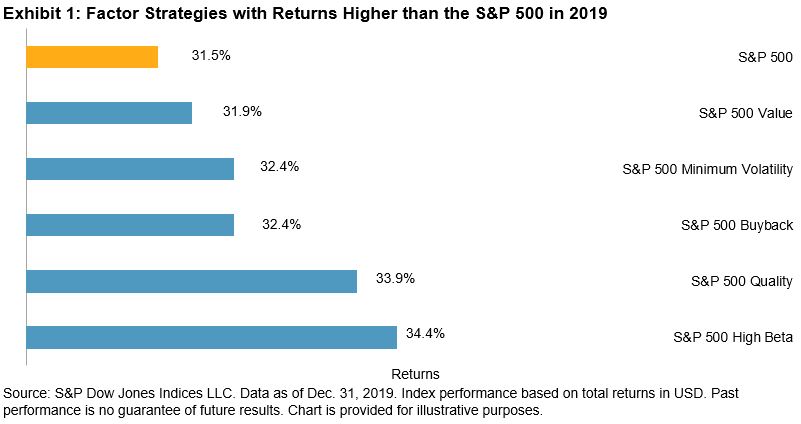

Shariah-Compliant Benchmarks Continued to Outperform Conventional Indices

Global S&P and Dow Jones Shariah-compliant benchmarks finished a standout 2019, a welcomed turnaround in comparison to the lackluster returns of the prior year. Broad-based Islamic indices outperformed their conventional counterparts in 2019 as Information Technology—which tends to be overweight in Islamic indices—led sector returns by significant margins, while Financials—which is underrepresented in Islamic indices—continued to trail behind the broader market. The S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index gained 31.2% and 30.9%, respectively, outperforming the conventional S&P Global BMI by an excess of 400 bps.

U.S. and Europe Outperform YTD, Robust Emerging Market Gains in Q4

Among regions, the U.S. and developed market conventional equities led performance YTD. In the U.S., easing trade tensions and accommodation from the U.S. Federal Reserve renewed optimism about the economic outlook, while European equities prevailed with the help of the central bank stimulus and falling yields amid slowing growth and Britain’s ongoing struggles to map an exit from the EU.

Meanwhile, the DJIM Emerging Markets gained 12.9% during Q4 2019 alone, compared to the 10.0% gain logged by the DJIM Developed Markets during the same period, narrowing the gap between the benchmarks YTD.

MENA Country Results Varied

Although MENA equity returns (in USD) reversed the prior quarter’s losses during Q4 2019, the YTD return of 12.5%—as measured by the S&P Pan Arab Composite—lagged broad emerging market benchmark gains. The S&P Bahrain continued to lead the region YTD, with a gain of 44.1%, followed by the S&P Kuwait, which added 31.3%. The S&P Oman and S&P Qatar lagged the most, gaining merely 1.2% and 1.9%, respectively, YTD.

Varied Returns of Shariah-Compliant Multi-Asset Indices

The DJIM Target Risk Indices—which combine Shariah-compliant global core equity, sukuk, and cash components—generally underperformed the S&P Global BMI Shariah and DJIM World Index YTD. Performance of the comparably more risk averse DJIM Target Risk Conservative Index was constrained by its 20% allocation to global equities in the expanding market environment, ultimately gaining 13.8% YTD. Meanwhile, the performance of the DJIM Target Risk Aggressive Index was driven by its 100% allocation to a mix of Shariah-compliant global equities, favorably returning 31.0%, in alignment with the broader S&P Global BMI Shariah and DJIM World Index.

For more information on how Shariah-compliant benchmarks performed in Q4 2019, read our latest Shariah Scorecard.