Quality is a factor that is frequently disputed and debated. Academics and practitioners often argue whether quality is a factor at all in the traditional risk factor framework. Often times, the debate stems from the fact that there is no one consistent, overarching definition or metric to measure quality.

For example, some market participants see low accruals (accounting related) or low earnings variability as signs of earnings quality. At the same time, there are market participants who see profitability as a sign of a high-quality company, and they use measures such as gross profit margin, return on equity (ROE), or return on assets (ROA) as quality proxies.

Solvency measures such as the debt-to-assets ratio or debt-to-equity ratio assess the “safeness” and quality of a company. In recent years, good corporate governance, as part of the greater trend in ESG investing, is viewed as an indicator of quality as well.

As another sign of the academic community recognizing that differences in quality factors lead to differences in stock returns, Nobel Laureate Eugene Fama and fellow researcher Ken French added two new quality factors—profitability and investment—to their asset pricing model in 2015.[1] Therefore, higher-quality companies, regardless of the definition of quality, on average earn higher risk-adjusted returns than lower-quality companies in both cross-sectional and time series analyses.

To demonstrate this point, we used the S&P 500® Quality Index, which is a composite measure of ROE, accruals, and leverage, as an example. We can see that profitability, as measured by ROE, was rewarded over a long-term investment horizon (see Exhibit 1).[2] Quartile 1—which comprised the most profitable securities or those with the highest ROE—earned higher returns than the other quartiles.

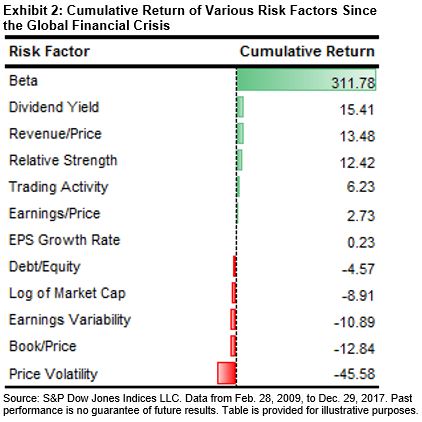

Earnings quality is another desirable characteristic, as shown by long-term premium earned by companies with low earnings accrual ratios over those with higher earnings accrual ratios (see Exhibit 2).[3] Low earnings accruals indicate that earnings are representative of the company’s true earnings power, and that they are more likely to persist in the future.

The financial prudence of a company or its use of leverage is another indicator of quality. Unlike other factors, leverage usage does not necessarily have a linear relationship with returns (see Exhibit 3). While highly leveraged companies can potentially result in financial distress, a low leverage ratio can indicate that a firm may be relying too much on equity financing to finance future business opportunities.

Lastly, we formed quartile portfolios ranked by overall quality score.[4] The results show that higher-quality companies outperformed lower-quality companies (see Exhibit 4).

As with all factors, quality goes through performance cycles. Even though higher-quality companies outperformed lower-quality companies over the long-term investment horizon, there may have been periods when lower-quality companies performed better. In upcoming blogs, we will discuss quality rotation in conjunction with market environments when quality premium is positive.

[1] Profitability is represented by robust minus weak (RMW), which is the average return on the two robust operating profitability portfolios minus the average return on the two weak operating profitability portfolios, as shown by the following equation.

[2] In our analysis, we ranked all the securities in the S&P 500 universe on a monthly basis by ROE and then divided them into quartiles

[3] We define accruals as the change in the company’s net operating assets (NOA) over the last year, divided by its average NOA over the last two years, as shown by the following equation.

[4] We ranked constituents of the S&P 500, the underlying universe, on a monthly basis using the winsorized average z-score and calculated the back-tested returns of the ranked portfolios. For more information on the quality factor calculation, see https://spindices.com/documents/methodologies/methodology-sp-quality-indices.pdf.

The posts on this blog are opinions, not advice. Please read our Disclaimers.