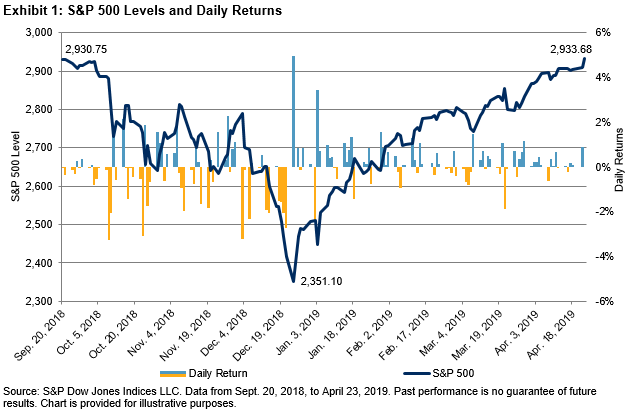

We recently updated our paper asking Is the Low Volatility Anomaly Universal? The alert reader (and we have no other kind) will have guessed that it is. This is an empirical conclusion, but a theoretical digression might help explain why this is so remarkable.

Low volatility strategies explicitly seek to lower the risk of a portfolio. We learn in basic finance that risk and return go hand in hand. We might therefore expect that with lower risk comes lower return. Except that it doesn’t, as Exhibit 1 below shows. In every market where we’ve developed a low volatility index, it has increased return as well as decreased risk — hence the academics’ description of low volatility’s performance as “perhaps the greatest anomaly in finance.”

Exhibit 1: Universally, Low Volatility Strategies Have Outperformed Respective Asset Class Benchmarks with Lower Risk

Source: S&P Dow Jones Indices LLC. Data through Dec. 31, 2018. Data start date varies for each index (see Appendix A of Is the Low Volatility Anomaly Universal?). Standard deviations are computed by annualizing the standard deviation of monthly returns. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with back-tested performance.

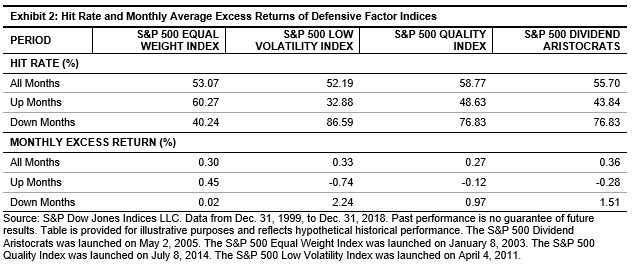

Our paper explores the characteristics of low volatility strategies, the most important of which, by far, is that they attenuate the magnitude of market returns — in both directions. Exhibit 2 below highlights the performance pattern of the S&P 500 Low Volatility Index®.

Exhibit 2: Low Volatility Strategies Tend to Offer Protection in Down Markets but Won’t Participate Fully in Up Markets

Source: S&P Dow Jones Indices LLC. Data from Dec. 31, 1990, to Dec. 31, 2018. Biggest declines were months when the benchmark was down more than 2.46%, moderate declines were months when the benchmark returned between -2.46% and 0%, moderate gains were months when the benchmark returned between 0% and 2.45%, and biggest gains were months when the benchmark gained more than 2.45%. Past performance is no guarantee of future results. Chart is provided for illustrative purposes and reflects hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with back-tested performance.

When the market is down, Low Volatility is highly likely to outperform; if the market is up substantially, Low Volatility is likely to underperform. Small positive months are close to a toss-up. Exhibit 2 summarizes data with respect to the S&P 500 Low Volatility Index, but our paper documents nearly-identical patterns for every other index in our low volatility family. Our claim that the low volatility anomaly is universal rests not only on its long-term performance, but also in its common response to moves in the underlying market.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices LLC. Data as of Apr. 19, 2019. Data has been based at 100. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

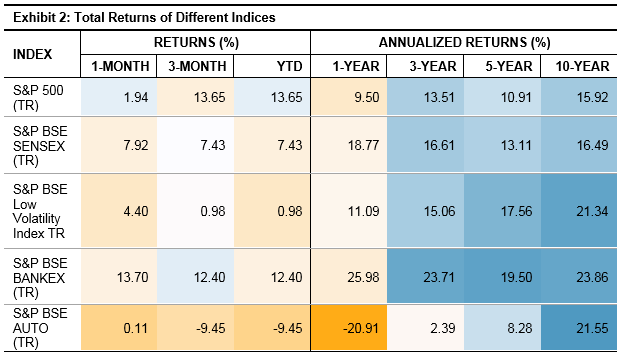

Source: S&P Dow Jones Indices LLC. Data as of Apr. 19, 2019. Data has been based at 100. Past performance is no guarantee of future results. Chart is provided for illustrative purposes. Source: S&P Dow Jones Indices LLC. Data as of Mar. 29, 2019. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

Source: S&P Dow Jones Indices LLC. Data as of Mar. 29, 2019. Past performance is no guarantee of future results. Table is provided for illustrative purposes.