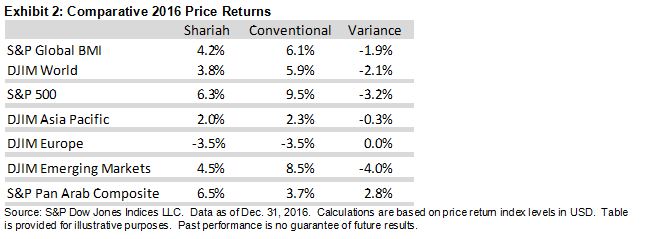

Most of S&P Dow Jones Indices’ Shariah-compliant benchmarks lagged their conventional counterparts for the year, as the financials sector—which is largely absent from Islamic indices—outperformed, and health care—which tends to be overweight in Islamic Indices—was the worst-performing sector globally.

The S&P Global BMI Shariah and Dow Jones Islamic Market World finished the year up 4.2% and 3.8%, respectively, lagging their conventional counterparts by approximately 2% each. Meanwhile, in the U.S., the S&P 500® Shariah gained 6.3% in 2016, underperforming the conventional S&P 500 by 320 bps. The Dow Jones Islamic Market (DJIM) Europe Index and DJIM Asia/Pacific Index performed relatively close to their conventional counterparts.

U.S. Equities Lead All Major Regions for the Year

U.S. equity markets led all major regions for the year, driven by enthusiasm following the U.S. presidential election in November. Emerging markets experienced declines in the fourth quarter, as prospects for higher U.S. interest rates and concerns about increased protectionism weighed on emerging market currencies and equities. Despite weakness late in the year, the DJIM World Emerging Markets Index finished 2016 up 8.5%. Europe was the only major region to close the year in the red, as uncertainty over BREXIT and continued economic weakness contributed to declining equity markets.

MENA Equities Close 2016 Strong, Reversing Losses From Earlier in the Year

After declining nearly 8% through the end of September, the S&P Pan Arab Composite gained 12.6% in the fourth quarter, closing the year up 3.7%. The S&P Pan Arab Composite Shariah gained an even stronger 16.5% in the fourth quarter, outperforming the conventional S&P Pan Arab Composite by nearly 3% in 2016 due to the S&P Pan Arab Composite Shariah’s greater exposure to Saudi Arabia.