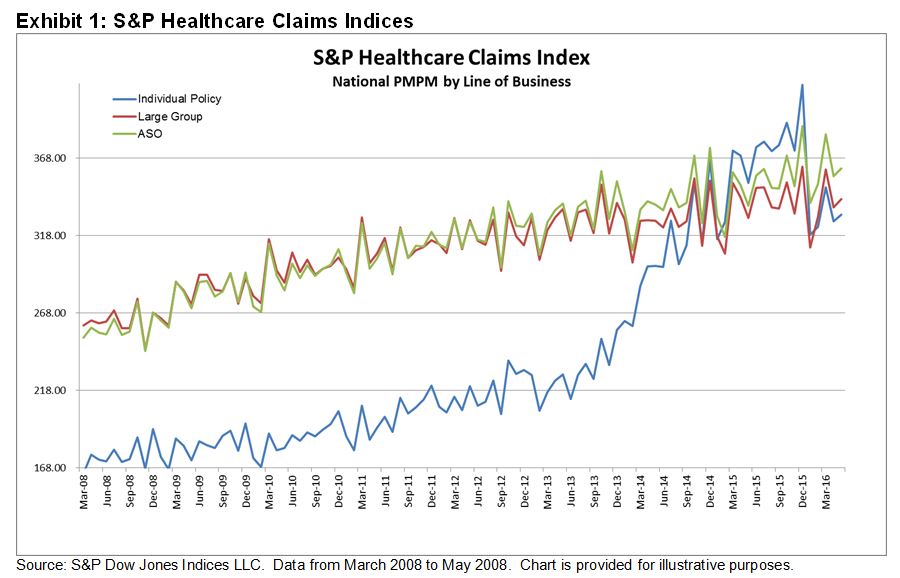

In our last post, we talked about how individual line of business costs have come back in line with employer healthcare costs (see Exhibit 1). In that piece, we discussed that one possible reason for this could be that individuals buying insurance for the first time under the new provisions of the Affordable Care Act (ACA), many of them with pre-existing conditions, are utilizing those benefits to address the conditions they had when they bought insurance. Given these individuals would be subject to plan yearly out of pocket maximum costs, it only makes sense that they would address as many of those issues as possible before the plan year expires. However, there is another possible explanation for the drop in costs.

The second reason why we could be seeing a drop in individual market costs relative to the employer market is the pull back of many larger insurers from the ACA public exchanges. By departing from the public exchanges, these health insurers are essentially opting to terminate coverage of individual policy holders in the state for which they have pulled out. We have seen announcements for the departure of health plans from the public exchanges from large national organizations such as United Healthcare, Aetna, Cigna, and Humana. However, more concerning are the regional plans and Blue Cross Blue Shield organizations, which tend to have a larger focus on the individual line of business. Included in this group of plans that have announced their departure from the public exchanges are BCBS New Mexico, BCBH Minnesota, BSBS Nebraska, and others. According to a Houston Chronicle article, in Texas alone, major plans such as Aetna, Cigna, Humana, United Healthcare, and Scott & White (a local player) have left the individual market void of options for coverage. In addition, according to the Houston Chronicle, Blue Cross Blue Shield of Texas has asked for a nearly 60% increase in premiums just to cover the increased costs of care for new enrollees under the ACA. The S&P Healthcare Claims Indices show enrollment was down nearly 20% in January 2016 for the individual market, and this is without taking into account the additional members expected to be pushed aside when many of the plans mentioned above are scheduled to either partially or entirely leave the public exchanges in January 2017. According to a U.S. News article, Alabama, Alaska, and Oklahoma are among the states that will have one health insurer selling individual coverage on their exchanges next year. South Carolina and most of North Carolina could join that list due to the Aetna decision. A key reason why insurers state they are leaving the public exchanges is that they are failing to attract enough healthy individuals to pay for the high cost of care for new enrollees entering the market, leaving them with huge losses for this market segment. If we look closer though, large insurers such as Aetna and United are not pulling out of all markets, only those they deem to be loss leaders. We are also seeing this with smaller regional plans. This means that they continue to participate in markets where costs are reasonable relative to expectations, or lower cost markets. This is another possible explanation as to why costs fell so dramatically in January 2016, and why we may yet see another decline in January 2017 as high cost enrollees are pushed out of the market.

Though both scenarios likely contributed to the significant drop in per member per month costs in January 2016, it is more likely that the real cause is a combination of both, as well as several other marketplace factors.

The posts on this blog are opinions, not advice. Please read our Disclaimers.