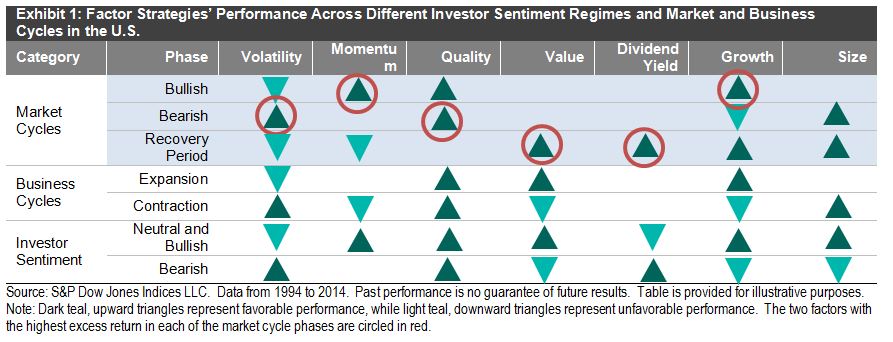

Historically, factor-based strategies have generated significant risk-adjusted returns in the long run, but they can also exhibit a high amount of cyclicality in the short run. Based on our studies of factor performance under different financial regimes—the market cycle, the business cycle, and the investor sentiment regime—we found that factor strategies historically have been most responsive to market cycle analysis, while business cycle and investor sentiment analysis have served as good complements to market cycle analysis (see Exhibit 1).

Overall, value and high-dividend stocks generally produced the highest outperformance during both bull markets and market recovery periods. However, they underperformed the market during the 1994-2000 market rally, partly because of their low exposure to information technology stocks. On the other hand, growth stocks displayed strong performance after the market had bottomed out at the beginning of 2003, and their streak continued in the ensuing bull market—but they vastly lagged the S&P 500® in bear markets.

Quality stocks generally produced positive performance in rising markets, but their defensive characteristics came to the foreground in bearish markets and recovery periods. Nevertheless, the defensiveness of quality stocks did not match that of low-volatility stocks, which beat the S&P 500 by the highest margin in falling markets. Low volatility underperformed the most when the market rebounded from its troughs.

Conversely, momentum stocks delivered consistent and material excess return during bull markets, but they underperformed in recovery periods because of large price trend reversals. Small-cap stocks outperformed the market in both bearish periods, and although they beat the market during recovery periods, they did not deliver consistent or significant excess return in bullish periods

In sum, factor strategies had distinct cyclicality and performed differently in various market and economic conditions. Apart from strategic implementation to achieve targeted portfolio risk exposure, single-factor smart beta indices can also be implemented tactically to express macro-investment views.

For more information on how smart beta strategies performed in different financial regimes, download the research piece or watch our smart beta video series.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

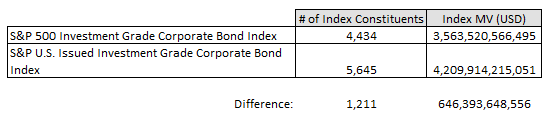

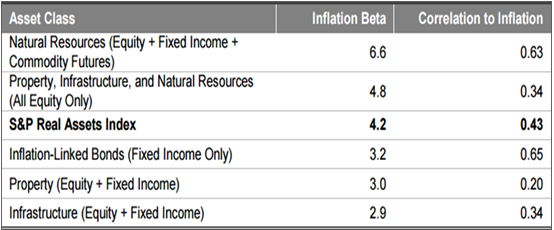

Source: S&P Dow Jones Indices LLC. Data as of Jan. 22, 2016. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

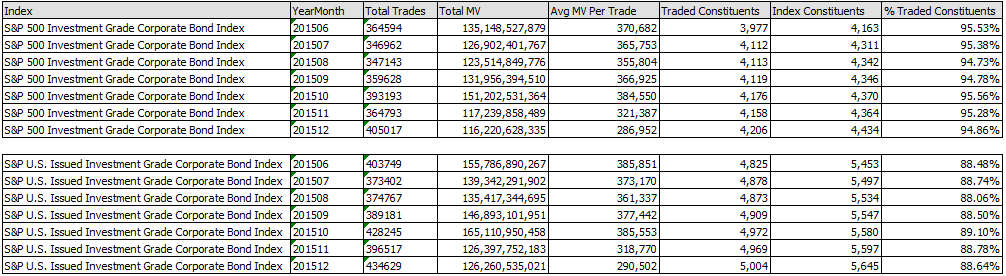

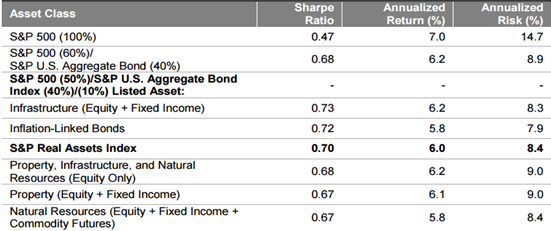

Source: S&P Dow Jones Indices LLC. Data as of Jan. 22, 2016. Past performance is no guarantee of future results. Table is provided for illustrative purposes.