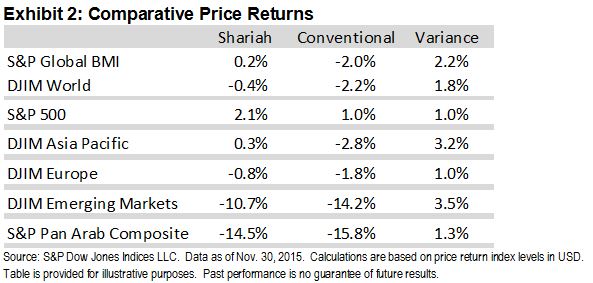

Most Major Islamic Indices Outperformed Conventional Benchmarks in 2015

Most S&P Dow Jones Shariah-compliant benchmarks outperformed their conventional counterparts through November 2015, as the financial sector—which is underrepresented in Islamic indices—has underperformed, and information technology and health care—which tend to be overweight in Islamic Indices—have been top performers.

The S&P Global BMI Shariah and Dow Jones Islamic Market World Indices have been nearly flat year-to-date (YTD) as of Nov. 30, 2015, outperforming their conventional counterparts by about 2% each in U.S. dollar terms. Over the same period, the S&P 500 Shariah gained 2.1%, beating the 1.0% gain of the S&P 500. Islamic indices covering the Asia-Pacific region, Europe, emerging markets, and Pan-Arab equities all outperformed their conventional counterparts as well.

Global Equity Markets Recovered in October Led by U.S. Equities

Following a major summer downturn, global equity markets recovered in October, led by the U.S., which stands as the only major global region in positive territory as of the end of November in U.S. dollar terms. It is important to note that the strengthening U.S. dollar has weighed on unhedged, non-U.S. equity returns. Asia-Pacific and European markets are well in positive territory in local currency terms, as the Dow Jones Asia/Pacific Index and Dow Jones Europe Index have gained about 5% and 8% YTD, respectively. Despite some recent stability in emerging market equities and currencies, the Dow Jones Emerging Markets Index remains down double-digits YTD.

MENA Equities Underperform as Oil Weakness Continues to Weigh on Returns

In contrast to other regions, MENA equities have continued to weaken in the first two months of the fourth quarter, as oil prices have continued to decline. The S&P Pan Arab Composite Shariah has fallen nearly 15% YTD in U.S. dollar terms, trailing all other regions by a substantial margin, despite not experiencing the adverse currency effects versus the U.S. dollar that have affected other regions.