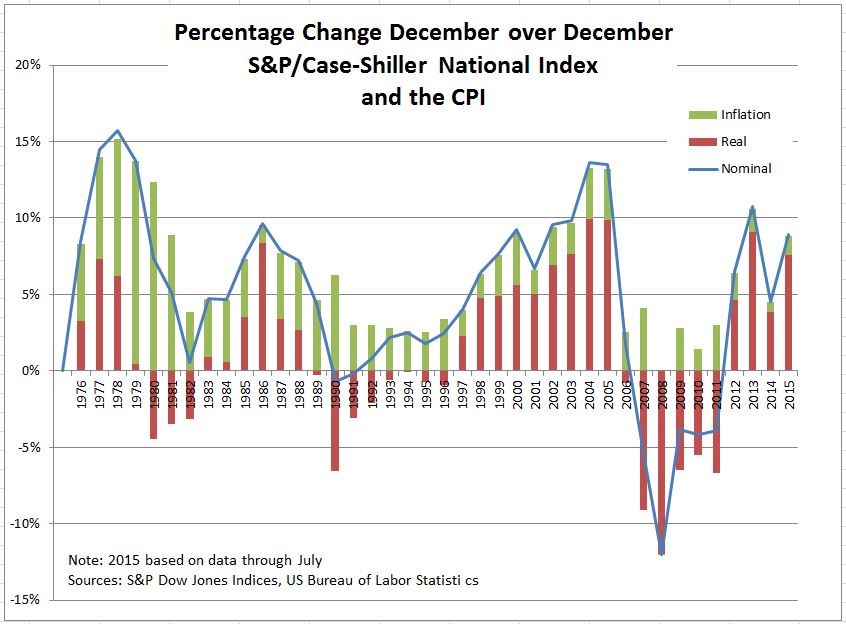

Prices of existing single family homes, as measured by the S&P/Case-Shiller National Home Price index, are rising is single digit terms. However, the price changes that matter – the real or inflation adjusted changes – may be higher than many suspect. Backing out inflation, as shown in the chart, gives real increases averaging 6.3% annually in 2012-20015. The compares to real increases of 6.8% annually during 1998-2005, the peak years of the housing boom. With two percent wage increases and one percent inflation, a real increase of 6% or more can make a difference. These numbers may offer one explanation for the recent popularity of apartments and renting.

The chart shows the rate of inflation (green bars), the real increase in the S&P/Case-Shiller National Home Price Index (red bars) and the nominal increase in the index (blue line). The data for 1976 through 2014 are the 12 months ended in December; for 2015 data for December 2014 to July 2015 are used and annualized.

The Next S&P/Case-Shiller Home Price Release is Tuesday, October 27th

The posts on this blog are opinions, not advice. Please read our Disclaimers.