The Exchange Traded Fund (ETF) landscape in Australia continues to grow and mature in assets under management (AUM) and in number of ETF products offered. As of June 2015, the Australian ETF Market was reported to be at A$18.1 Billion in AUM and 107 ETFs traded on the ASX. As an index provider with deep roots in the Australian market, S&P Dow Jones Indices takes interest in this, because Exchange Traded Funds which are index-trackers are the delivery vehicles of index effectiveness and index-based innovations.

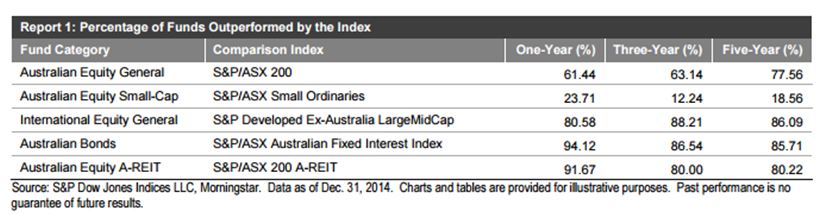

Index Effectiveness*: One way to judge if an index is effective is to determine if it measures an asset class or a market in an investible manner. For years, S&P DJI has conducted analysis and published a research report named S&P Index vs Active, or SPIVA®. The purpose of the SPIVA report is to compare the field of actively managed mutual funds against an apples-to-apples index benchmark in size and style. We now calculate SPIVA for several markets, including Australia. Here are some of the latest results for Australia:

With our index benchmarks demonstrating that they are hard for many actively managed mutual funds to beat (with the notable exception of Australian Small-Cap), we conclude that indices are effective in measuring markets and asset classes, which can be accessed by ETFs that track these indices.

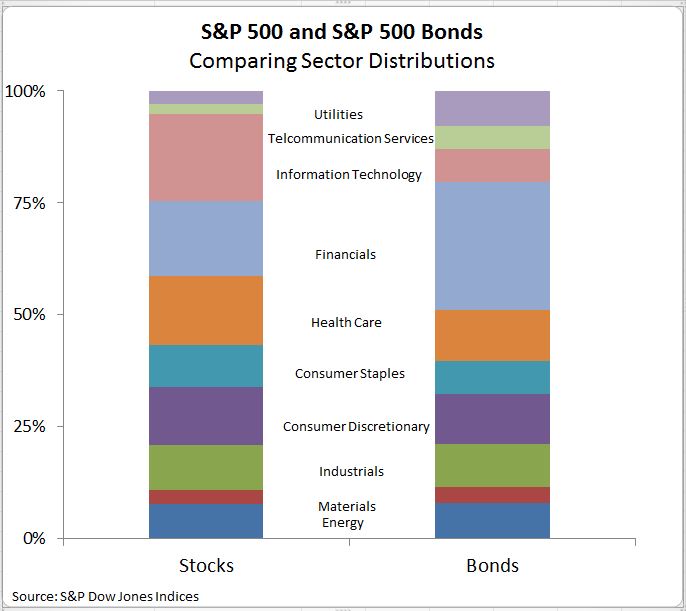

Index-based Innovations: Indexing measures international markets and asset classes beyond Australia’s shores. One of the presenters at our recent 5th Annual ETF Masterclass in Sydney and Melbourne said that “Australians may be the champions of home bias.” Several International ETFs list in the Australian market, providing the means to mitigate the risks of that home bias. The largest of these by size are tracking the S&P 500® index, measuring Large-Cap U.S. companies. Indices and the ETFs tracking them in Australia have also advanced to cover asset classes beyond equities. The Australian ETF market now offers ten fixed income ETFs which are index-trackers. Two of those, issued by State Street Global Advisors, are tracking S&P DJI fixed interest indices. Real Assets such as Real Estate and Commodities are covered by indices and there are a number of these available now as ASX-listed ETFs. You might expect to see Australian ETFs in the future covering infrastructure equity and debt Indices or other real assets that were formerly only accessible to institutional investors in illiquid ways. In this manner, the growth and advance of the Australian ETF market will democratize access to financial solutions.

The latest index-based innovations may be found in what some are calling smart beta indices. From an indexing perspective, smart beta may be partially described as an index designed to deliver a particular factor (value, quality, momentum, etc.) or an index which alternatively weights an asset class or both those features at the same time. In the Australian ETF Market, these smart beta strategies may be managed fund ETFs. A new ETF product provider to the Australian market, ANZ ETFS has announced the launch and listing of two new smart beta ETFs which are index-trackers: one of these ETFs tracks the S&P 500 High Dividend Low Volatility Index, the other tracks the S&P/ASX 300 Shareholder Yield Index.

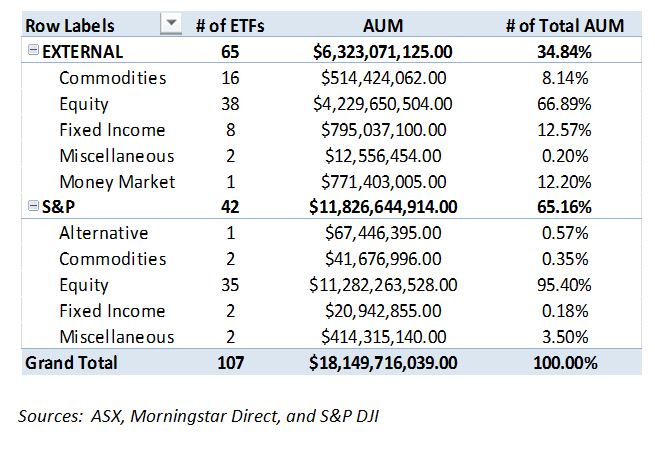

We judge that indexing effectiveness and indexing innovation may be beneficial for financial markets. However, as the Australian ETF market grows in number of ETF offerings and the complexity of these ETF offerings, an increasing burden of due diligence is placed on Aussie planners, wealth managers, and institutional investors who seek to benefit from what ETFs may offer. As the index provider for 39% of these ETFs by number and 65% by AUM (please see table below), we believe that we have a part to play in the education component of that due diligence.

By education, I specifically mean that we are in the position to share with you how index construction and other index rules and characteristics matter to the ETF tracking them. To that end, we can also share index historical performance data and analysis on that performance as a further guide to those seeking a better understanding of ETFs. An example of this type of education is “Why Does the S&P 500 Matter to Australia.” Also, a current list of S&P Dow Jones Indices which have been licensed by ETF providers and listed on the ASX may be found on spdji.com.

Source: S&P Dow Jones Indices. Ten years of daily data ending July 7, 2015.

Source: S&P Dow Jones Indices. Ten years of daily data ending July 7, 2015.