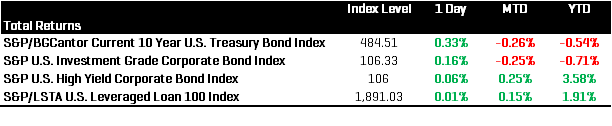

Closing out a short week before the U.S. fourth of July holiday, the yield-to-worst of the S&P/BGCantor Current 10 Year U.S. Treasury Index closed at 2.38% on Thursday, July 2, 2015. The yield-to-worst was 9 bps lower than the 2.47% close of the previous Friday (June 26, 2015), as concerns over the Greek bailout vote on July 5, 2015, moved some investors to the safety of treasuries. The index lost 1.86% for June, and it was down 0.26% for the first two days of July. The YTD return of the index has been in negative territory since June 3, 2015, and the index had returned -0.54% YTD as of July 2, 2015.

The past week’s news affected the S&P U.S. Investment Grade Corporate Bond Index similarly, as the yield-to-worst closed before the holiday at 3.19%, 3 bps lower than the previous Friday’s 3.22%. Investment-grade yields followed U.S. Treasury yields lower, as investors reacted to continued information about the negotiations between Greece and its creditors. The index closed out June down 1.53%. For the beginning of July, the index had returned -0.25% MTD and -0.71% YTD as of July 2, 2015.

High-yield issuance was slow before the holiday weekend, as two smaller deals came to market, pricing on June 30, 2015. SS&C Technologies Inc. issued USD 600 million of an eight-year bond with a coupon of 5.875%. The second deal was issued by DAE Aviation Holdings and was USD 485 million of an eight-year bond with a coupon of 10%. High-yield bonds, as measured by the S&P U.S. High Yield Corporate Bond Index, lost 1.41% in June, but the index had returned 0.25% for the first two days of July and 3.58% YTD.

Unlike the high-yield index’s -1.41% slide in June, the S&P/LSTA U.S. Leveraged Loan 100 Index was down for the past month, but by only 0.86%. As of July 5, 2015, the index had returned 0.15%, while it was returning 1.91% YTD.

Source: S&P Dow Jones Indices LLC. Data as of July 2, 2015. Leverage loan data as of July 5, 2015. Past performance is no guarantee of future results. Table is provided for illustrative purposes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.