On the surface, the most basic commodity beta, the S&P GSCI, hasn’t done much in 2015. It is down just 21 basis points (bps) for the year after losing 11 bps in June. Further, only 9 of 24 commodities are positive year-to-date with the overall term structure in contango after two years of structural backwardation. Coffee, lean hogs and nickel are the biggest losers for the year, down 24.6%, 24.5% and 21.5%, respectively. However, unleaded gasoline, cocoa and cotton that are up the most of 20.3%, 12.4% and 10.7%, respectively, have gained significantly.

Please see the table below for sector performance through June 30, 2015:

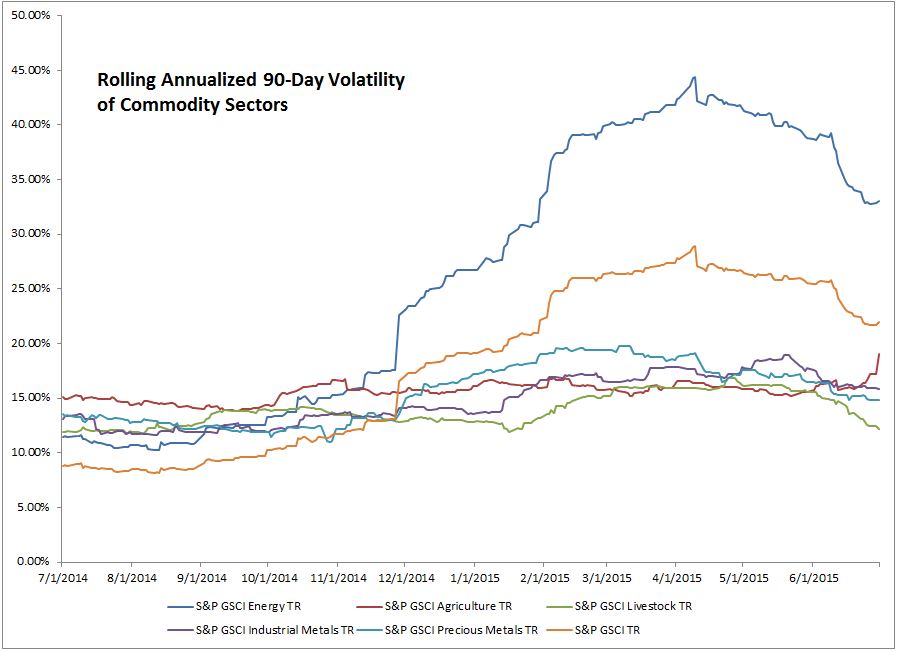

Most interesting in 2015 thus far is the volatility in commodities with 9 of 24 commodities posting double-digit moves for the year. The volatility in energy peaked in early April followed by an industrial metals spike in May. The performance of energy has been so dominated by oversupply that its response to the economy has been masked. However, industrial metals, also known for its economic sensitivity had spiked together with energy in April – that was indicative of a contraction, and these sectors followed with weak performance. The volatility with the poor performance was finally enough to drive a new wave of investor selling that may be just the catalyst needed to stabilize the market. If open interest collapses, then production may slow as insurance in the futures market becomes too expensive. Historically in high volatility periods, open interest needs to collapse before oil finds stability again.

The one sector that is picking up volatility is agriculture. Extreme weather from El Nino may be the biggest driving force in the solid gains for every single one of the eight commodities in the sector in June. The grains were up 20.0% in June, its fourth best month in history (since July 1982) and best June since 1988. Even with lesser performance of only 3.1% in June, agriculture posted its biggest monthly gain in three years with its sixth best month in history.

Going into the summer there is generally an increase in demand for gasoline to support more driving; however, the bad news for consumers is that gas prices rise much quicker with oil prices than they fall when oil falls. Cheaper natural gas and livestock are other summertime favorites that may help consumers maintain demand for gasoline through the driving season. However, livestock is now showing seasonal shortages (is the only sector in backwardation) so the prices may start to rise – and at an accelerated pace from the increasing prices of grains used to feed the livestock.

The posts on this blog are opinions, not advice. Please read our Disclaimers.