I have a neighbor who is cooler than me. He is braver than me. He also has more expansive and expensive medical and auto insurance than I do. How do I know all this? Well, he races street motorcycles.

The other day I asked him what was the fastest he had ever gone. His answer: “Very fast, but that’s not where the thrill is. The adrenaline rush comes from handling and powering through the curves.”

The movements in the CBOE Volatility Index (VIX) the past few weeks have made me reflect on this conversation. We know the VIX’s approximate top speed — somewhere around 80 — but it’s the changes in direction, the twists and turns, which test your skill.

Recently, the VIX took investors on a treacherous hairpin turn. It looked like this:

Did you get thrown off your motorcycle? It seems that many investors handled this deftly, seeing this jump in the VIX as a wicked but ultimately short-term movement. We know this by the performance of the VIX futures market.

VIX Futures in Times of Big Crises

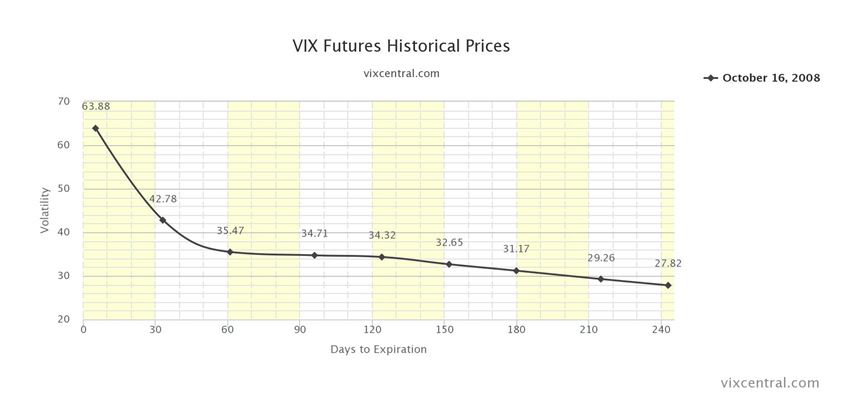

First, to get some context, let’s look at the behavior of the VIX futures during the standard for all recent crises, the 2008 meltdown. In that time, when the whole market went to heck, the VIX shot up and the futures term structure went into backwardation across all maturities.

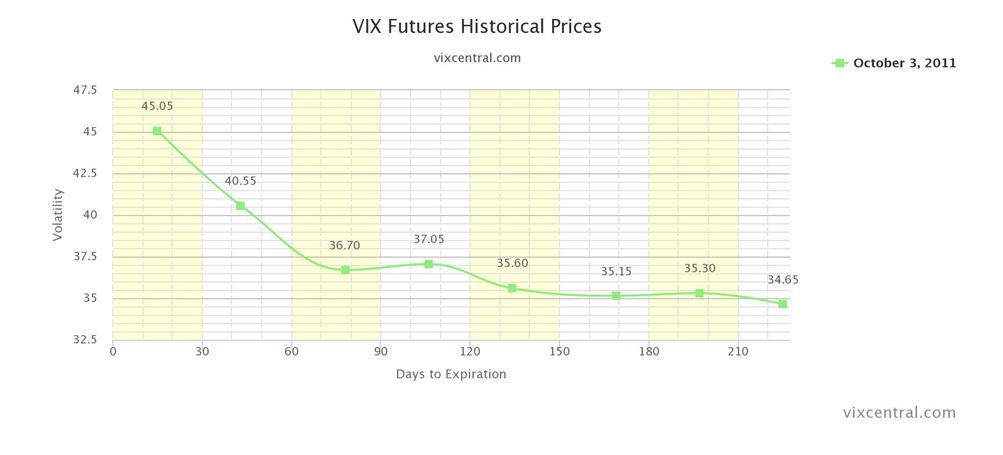

The VIX futures term structure assumed a similar shape during the standoff over the government debt ceiling in 2011.

The Hairpin Turn

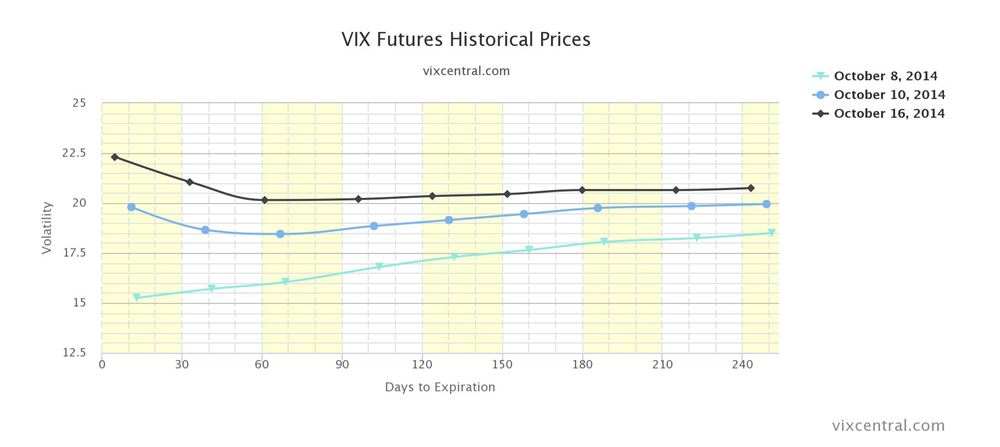

Now let’s see what happened during the recent shakes and tremors in the market. The term structure shifted up and developed a kink around the second and third months, after which the rest of the term structure remained upward sloping, in contango. The shift up indicated that investors expected greater volatility across all periods, but the kink showed that they didn’t necessarily expect the very high levels the VIX had reached to persist.

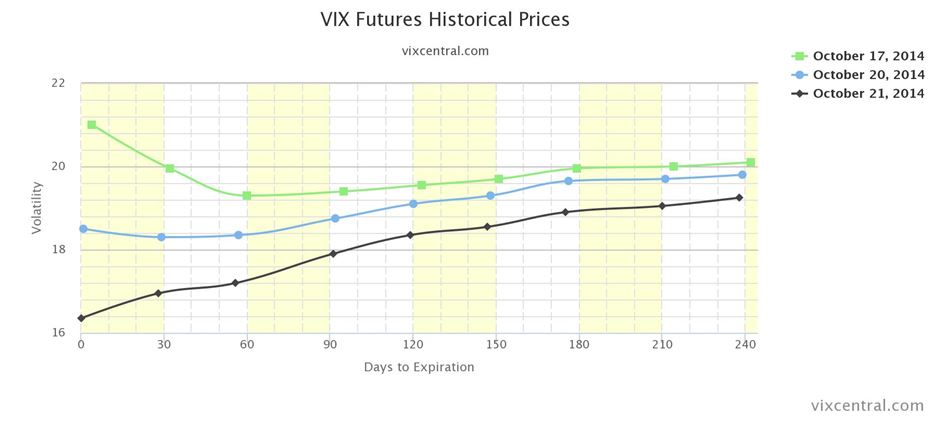

Over the next few days, investors became even less worried about high volatility in the S&P 500 continuing. The VIX futures curve shifted downward and adjusted back into its most typical shape, which is contango across all maturities.

The investors betting on volatility subsiding to a degree have turned out to be right, at least for now. But there will undoubtedly be more turns on the way – both hairpin and more traditional curves – to test their driving skills.

The posts on this blog are opinions, not advice. Please read our Disclaimers.