On Wednesday, July 30th, S&P cut the credit rating on Argentina’s foreign currency bonds to “selective default” after they failed to reach a deal with holdout bondholders from their last default in 2001. US Treasuries initially sold off only to recover, investment grade corporate bond markets had a somewhat muted reaction, while high yield and Credit Default Swap markets widened considerably. On Friday, August 1st, ISDA ruled Argentina’s failure to pay bondholders a “credit event”.

U.S. Treasuries finished lower on Wednesday as markets expected a last minute deal to come through, decreasing the need for the safety of U.S. Treasuries. The (duration 3.92) yield closed wider on July 30th by 4 bps from 1.10% to 1.14% before tightening to 1.09% by employment Friday’s close. The S&P/BGCantor Current 10-Year U.S. Treasury Index widened 10 bps on July 30th from 2.46% to 2.56% before tightening to 2.50% due to the weaker than expected employment figures on Friday.

Corporate bonds were lower Wednesday with the S&P U.S. Investment Grade Corporate Bond Index yield widening 7 bps from 2.75% to 2.82%. U.S. Corporate CDS spreads lagged the trend, with the S&P/ISDA U.S. 150 Credit Spread Index ending mostly unchanged on Wednesday at 49.03, and widening only on Thursday July 31st to 51.44. CDS spreads widened further to Friday to 52.74 after ISDA’s decision and the employment number failed to impress.

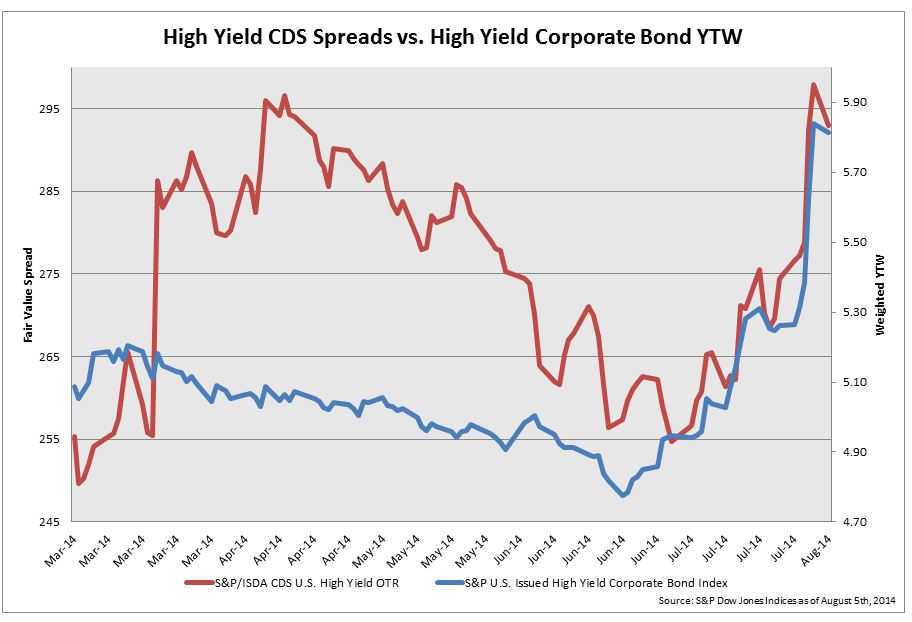

The high yield market naturally took the most dramatic response to Argentina. The S&P U.S. Issued High Yield Corporate Bond Index yield widened only 8 bps from 5.31% to 5.39% on Wednesday, as again the market anticipated a last minute deal, only to widen further on the 31st to 5.62% and then again on Friday to 5.84% for a total move of 53 bps. High yield CDS spreads barely reacted Wednesday, with the S&P/ISDA CDS U.S. High-Yield Index widening only 1.6 bps to 278.83. Spreads caught up on Thursday widening to 292.38 and then another 5.5 bps on Friday to close at 297.89. That is 19 bps – a spike the S&P/ISDA CDS U.S. High-Yield Index has not seen since Janet Yellen’s stimulus program comments in March caused a 31 bps jump. High yield CDS spreads have snapped back since Friday, closing Monday August 4, at 292.88, 5 bps tighter.

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.

The divergence between CDS spreads and actual high yield bond yields show that the bond market has not followed CDS spreads movements due to the appetite for yield supporting the high yield market and pushing bond yields down. Argentina’s default caused bond yields to move more in line with the direction of CDS.