Every conversation I’ve had today with people from Nashville to Toronto has started with how cold it is outside. After the shock of the cold and when the heating bills come due, the conversation may turn to how expensive heat was in January. That, of course, is at least for those who don’t invest in commodities to offset price spikes.

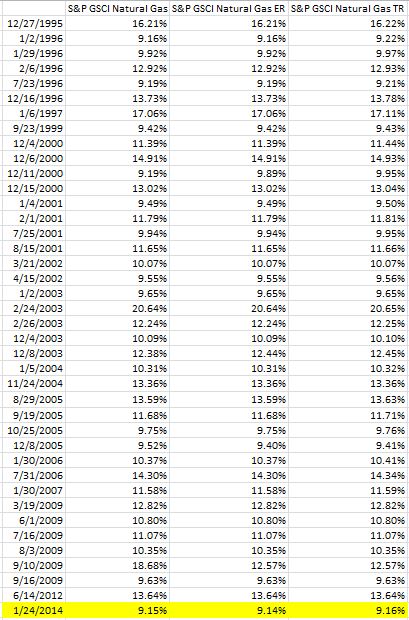

After natural gas posted the biggest one-day gain of 9.2% on Jan 24, 2014 since June 14, 2012, the S&P GSCI Natural Gas has gained 19.3% this year. It has gained 25.9% in just 10 days since Jan. 9, 2014 and is also up 44.6% since it’s low for the prior year on Nov. 4, 2013.

In the history of the index since Jan 8, 1994, it has been calculated on 5,053 days and only 39 of 5,053 days have had a higher gain than the 9.2% seen on Friday – that is only 0.77% of days. That puts Friday’s gain in the top 1% of big daily gains for the natural gas index. See the table below for days gaining more than 9.2%:

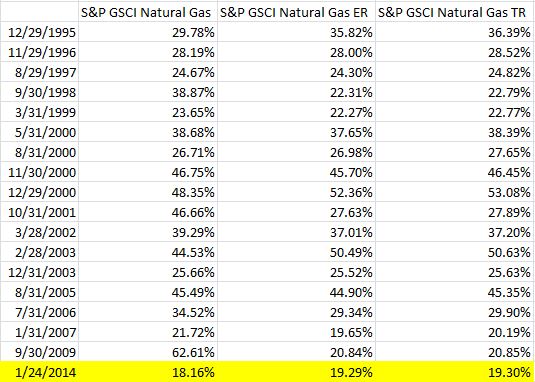

Also, January 2014 MTD has posted the biggest monthly gain since September 2009. Only 17 months of the 240 in the history of the index have seen bigger gains than 19.3%. Although natural gas can be considered in a bull market from the bottom, many will watch to see if natural gas will earn the bull market stamp in January by breaking break the mark of a 20% gain for the month. Please see below for the table of natural gas bull market months:

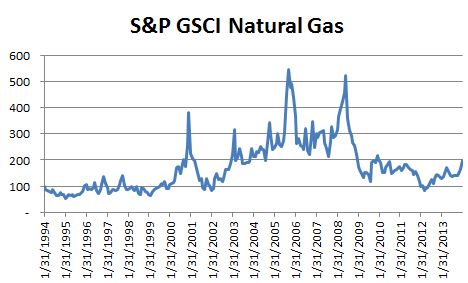

Last, below is a chart of the index, where you can see the level is highest since Jan. 29, 2010.

The posts on this blog are opinions, not advice. Please read our Disclaimers.