Stocks closed down today with the S&P 500 and the Dow Jones Industrials both down 1.8% despite yesterday’s stronger-than-expected GDP report, numerous earnings reports which beat Street expectations and no hints of early interest rate moves from the Fed. Bearish or negative news stories weren’t much different from the day or week before – unrest in the Middle East, sanctions on Russia in response to fighting in the Ukraine and an on-going argument between Argentina and a hedge fund over debt. There was no single event to send the market down for the worst loss in years.

Fear, greed, anxiety and the madness of crowds really do drive markets. While it is often possible to cite shifts in the economy, corporate earnings or political events for market moves that extend over months or years; short term day-to-day shifts are driven as much or more by emotion than by reason and news. Robert Shiller, the author of Irrational Exuberance, describes surveys of investors down in the days following the 1987 market crash. Clearly today’s dip is nothing like the 1987 event when the S&P 500 dropped over 20% in a day, but then investors couldn’t point to a news story or major event that sent the market plunging. The most common news stories cited by investors were about falling stock prices, not some external change in fundamentals or the economy.

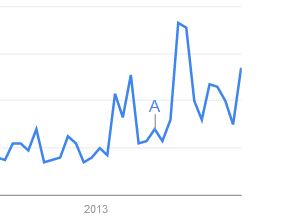

Was today’s drop driven by emotion or anxiety with little news or analysis of fundamentals? The market has drifted in the last few days and closed flat on the best economic news in the last few years. The chart shows a rise in the frequency of searches for the phrase “stock market bubble” on Google Trends and the biggest news story seems to be a lack of action in the Congress. It will take several weeks or months to see if today’s drop was caused by more worried people selling than confident people buying. Unless news and the fundamentals turn much worse the best explanation may be simply worried investors.

Google Trends shows the relative frequency of searches for specific terms. The letter A indicates the publication of an article in Forbes on Where to Invest When the Market Bubble Bursts.

The posts on this blog are opinions, not advice. Please read our Disclaimers.