Assigning equal weights to each constituent, such as in the S&P 500 Equal Weight Index, historically would have offered material outperformance over capitalization-weighted benchmarks across a range of markets. Earlier this year, we published a paper examining how this occurred.

There are several perspectives one can take, ranging from factor or sector exposures all the way down to the pattern of contributions from each individual constituent stock. However, one of the most interesting aspects of equal weight outperformance is that it arises primarily not through the differences between equal and cap-weighted sector exposures, but rather through the consequences of equally weighting within each sector.

So, what is going on? We suggest that successful competition within each industry provides a mechanism for outperformance within equal weight indices.

Within a competitive industry setting, if a firm secures an advantage and begins to outperform, then three things will likely follow in consequence. The first is that market capitalization of that firm will likely increase, relative to its peers. The second is that – supposing such outperformance continues – the related sector index will become more concentrated into the outperforming company. The third and final consequence – assuming a high level of competitiveness – is that the peers of that company will find ways to catch up with the prior leader, and reverse the prior concentration.

These consequences should be observable through the relative performance of equal weight indices. If the largest companies in a sector outperform their peers, then a capitalization weighted index will outperform an equal weight index. If the smaller companies in a sector outperform, then the equal weight index will outperform.

High levels of concentration might therefore provide a potential indicator for the future outperformance of equal weight indices in highly competitive sectors, since unusually high concentration in a sector may indicate significant potential for smaller firms to catch up – either through restrictions (regulatory or otherwise) placed on the larger firms, or organically as those smaller firms act catch up with the leaders.

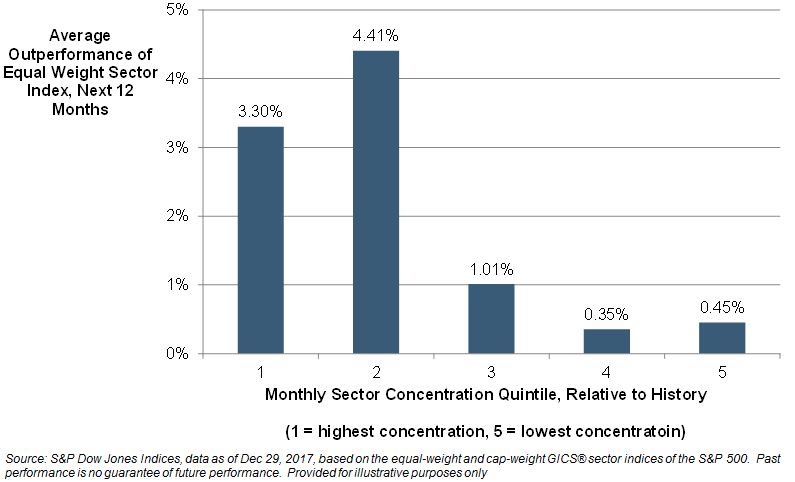

We test this idea by comparing the relative level of historical concentration in each sector to the subsequent performance of equal weight indices. In particular, for every month from December 1995 to December 2016, we first calculate the percentile rank in HHI concentration for each of 10 S&P 500 sectors compared to its (monthly) history since 1990. We then examine the relative total return of the respective equal weight sector index, relative to its capitalization-weight sector counterpart, over the next 12 months. The chart shows the results, split by quartile of relative concentration:

Concentration Versus Subsequent Equal Weight Outperformance in S&P 500 Sectors, 1995-2017

As the chart shows, on average, the strategy of equally weighting within a sector appeared to have been most attractive when that sector was unusually concentrated. With the increasing availability of products linked to equal weight sector or market indices, investors might therefore consider “backing competitiveness” by adopting equal weight strategies in sectors or industries that appear to be more concentrated than usual.

The posts on this blog are opinions, not advice. Please read our Disclaimers.