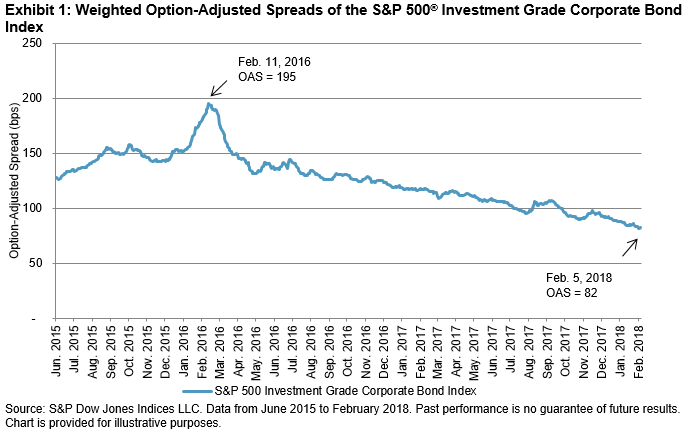

Broad-based equity markets have been on a rollercoaster ride since Jan. 30, 2018, as market participants appear to be reassessing the impact of inflation and potential consequences from the recent tax reform. While volatility appears to be back, high-grade corporate bond spreads have tightened to levels not seen since 2007. Compared with the last episode of substantive volatility in equities, there is a noticeable difference in how credit markets are reacting (see Exhibit 1).

In 2016, equity indices began the year down double digits, as oil prices plummeted and contagion spread, while multiple energy companies filed for bankruptcy. As a result, investment-grade credit spreads widened by 50 bps, with high-yield spreads jumping over 200 bps.

2018’s volatility is showing markedly different results in the bond market. As of Feb. 5, 2018, investment-grade spreads had tightened 6 bps and were more than 110 bps tighter compared with February 2016, as measured by the S&P 500 Investment Grade Corporate Bond Index.

There were several factors contributing to this.

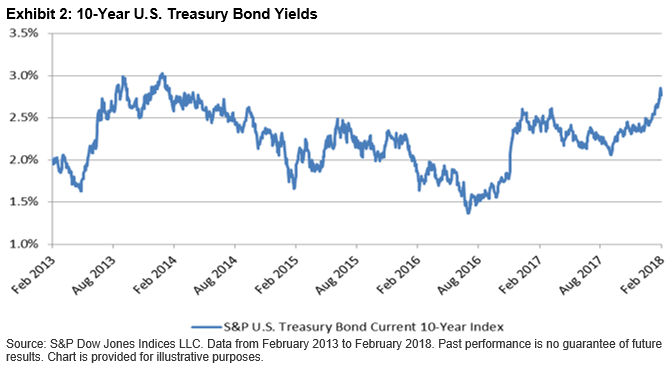

1) Increased U.S. Treasury Yields: Inflationary pressures from global growth, increasing wages, and quantitative tightening have driven yields higher throughout the curve. The yield on the 10-year U.S. Treasury bond (as measured by the S&P U.S. Treasury Bond Current 10-Year Index) rose 30 bps in January and hit 2.70% for the first time since 2014 (see Exhibit 2).

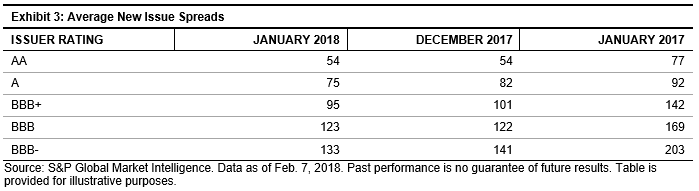

2) Market Technicals: High-grade issuance was relatively sparse in January, specifically in the non-financial space. Total issuance volume was down over 30% compared with January 2017, with non-financials sectors capped at USD 27 billion—a 45% reduction from 2017. Many market participants anticipate that the repatriation and tax changes in the new laws may potentially affect borrowing patterns with high-quality issuers, and that sentiment was reflected in average new issue spreads (see Exhibit 3).

3) Credit Fundamentals: Investors appear comfortable with current corporate credit fundamentals. The bullish argument asserts that the reduction in corporate tax rates will have a front-loaded impact. Since these rates become effective in 2018, many corporations will have an immediate increase in their level of free cash flow. Additionally, changes in the tax code could also allow companies to use repatriated cash to delever, further reducing credit risk.

The posts on this blog are opinions, not advice. Please read our Disclaimers.