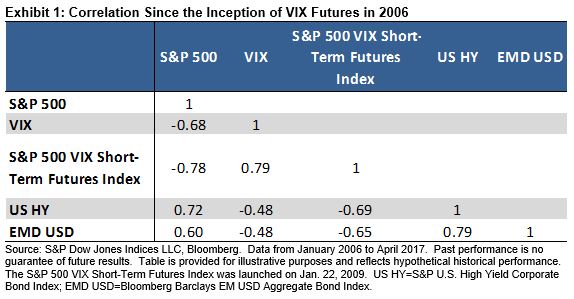

The CBOE Volatility Index® (VIX) measures the implied volatility of the S&P 500® over a 30-day period. It is widely followed by market participants across asset classes to gauge market sentiment. Traditionally, fixed income market participants have incorporated it into macro analysis.

Can VIX-related products be used as hedging tools for some bond sectors that exhibit certain equity-like features? For high yield and emerging market bonds, credit and liquidity risks are more defining than duration risk. Dor and Guan (2017) demonstrated that equity futures can be used to hedge high yield portfolios. We investigated a correlation analysis of high yield and emerging market bonds to VIX and VIX futures.

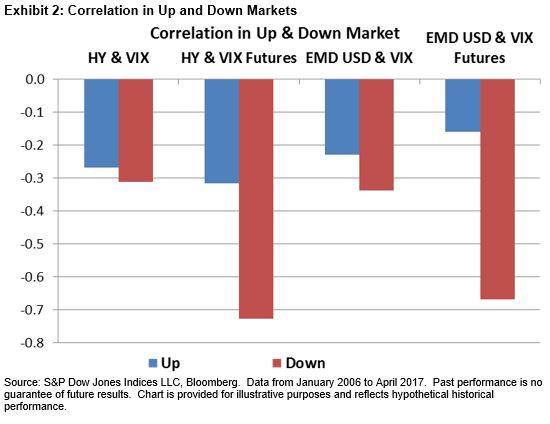

Based on the correlation analysis, we can make the following observations.

There is a strong correlation between high yield and emerging market bond returns (0.58 and 0.79). This could be due to the fact that emerging market countries and corporations that issue U.S. dollar-denominated bonds are likely to be closely tied to the strength of the U.S. economy and U.S. companies. The overlapping investor base for high yield and emerging market bonds may also compound the return correlation between these two sectors.

There is a strong correlation between high yield and emerging market bonds and the S&P 500. In other words, returns from U.S. large-cap stocks can explain a large part of variance in high yield and emerging market bond returns. In our observation period, 51% of (square of correlation) variance in high yield bond returns and 36% of variance in emerging market bond returns can be explained by the variations in the returns of U.S. equities.

There is a negative correlation between VIX and VIX futures and high yield and emerging market bonds. This demonstrates that as high yield and emerging market bonds have more exposure to credit spreads than duration risk, they tend to exhibit more equity-like properties and a strong correlation with equity volatility.

It is noteworthy that VIX futures exhibits stronger negative correlation with credit bonds than VIX spot, and therefore argues for a stronger case of VIX futures as a hedging instrument for bonds. In fact, when correlation analysis is conducted for up and down market periods separately, it can be seen that this stronger negative correlation of bonds to VIX futures than to VIX spot comes mostly from down markets (see Exhibit 2).