The relentless drive for yield has caught up with U.S. high yield bond investors. Junk bond holders have been beaten up by the one risk they did not want to see: credit spreads widening. High yield bonds have seen compressed yields for some time as the relentless drive for yield had shifted flows toward yield producing assets. Unfortunately, that segment of the bond market has endured sector risk (energy and materials) as well as signs the default rate is rising back toward historical norms.

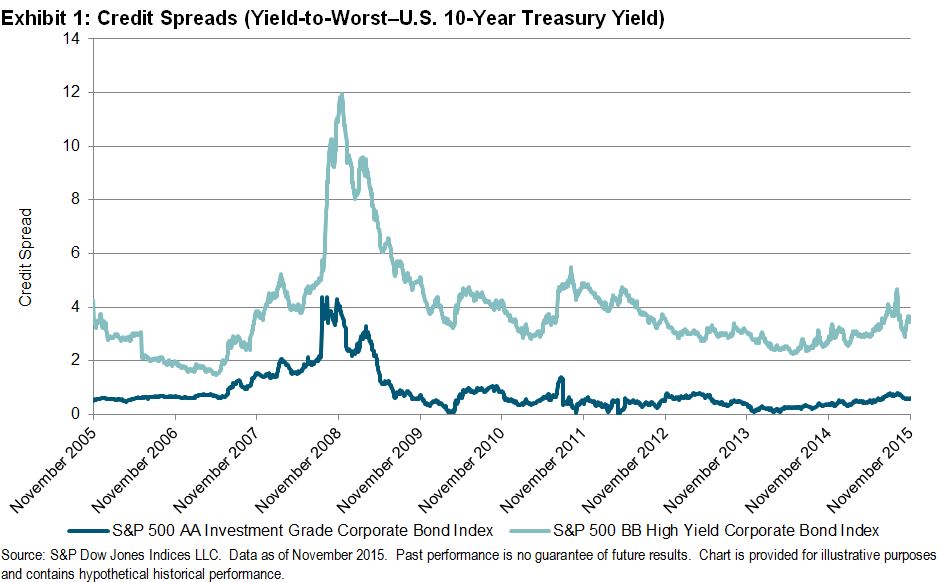

Credit spreads of bonds in the S&P 500 Bond Index have jumped. Yields of bonds in the S&P 500 BB High Yield Bond Index have risen 165 basis points since July 1st driving the total return down by over 5.3% during that time.

Chart 1: Select index yields (Yield to Worst)

Source: S&P Dow Jones Indices, LLC. Data as of December 21st, 2015.

As yields rise, bond prices have fallen erasing gains seen earlier in the year. Year-to-date total return for the S&P 500 BB High Yield Corporate Bond Index is – 4.4%.

Table 1: Select index Year-to-Date Returns:

Source: S&P Dow Jones Indices, LLC. Data as of December 21st, 2015.

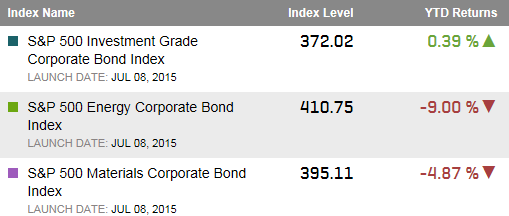

The energy and materials sectors of the bond markets have been a real drag on performance on the junk bond markets as bond prices have fallen. The S&P 500 Energy Bond Index is down 9% year-to-date and the S&P 500 Materials bond Index is down over 4.8% year-to-date.

Table 2: Select Bond Sector Indices Year-to-date Returns:

Source: S&P Dow Jones Indices, LLC. Data as of December 21st, 2015.

The posts on this blog are opinions, not advice. Please read our Disclaimers.