The godfathers of value investing, Graham and Dodd, pioneered the approach back in the 1930s. Since then, academics and practitioners have documented the value effect. However, given its widespread adoption and implementation, there is still no single consensus as to why value stocks provide above-market returns. Explanations broadly fall into two camps: the rational and the behavioural.

Rational theories explain how the value premium arises from investors requiring compensation for bearing higher systemic risk in the form of financial distress (Fama and French 1996).[1] For example, in recessionary environments, value firms (like manufacturing) find it difficult to shift their activities to more profitable ones. By contrast, growth firms (such as technology) can disinvest relatively easily, as a large proportion of their capital is human capital. Hence, value firms are perceived as being riskier than their growth counterparts and, as such, should command a premium.

Behavioural theories argue that the value risk premium might be driven by investors incorrectly extrapolating the past earnings growth rates of companies (Lakonishok et al. 1994).[2] High profile, glamorous stocks that have high valuations are bought by naïve investors expecting continued high growth rates in earnings. This pushes up their prices and, as a consequence, lowers their rates of return. At the same time, value stocks are cheap, as investors underestimate their future growth rates. Their cheapness does not arise from the fact that they are fundamentally riskier.

There are many ways to define value. For example, cash-flow yield and earnings yield examine cheapness while emphasizing profitability. Dividend yield provides insight into management’s assessment of future profitability. Using the balance sheet item of net assets (book) gives a measure of liquidation value. Other value measures include predicted earnings yield and EBITDA[3]-to-enterprise value. Equity products that aim to harvest the value premium can be constructed by using one or a combination of these measures.[4]

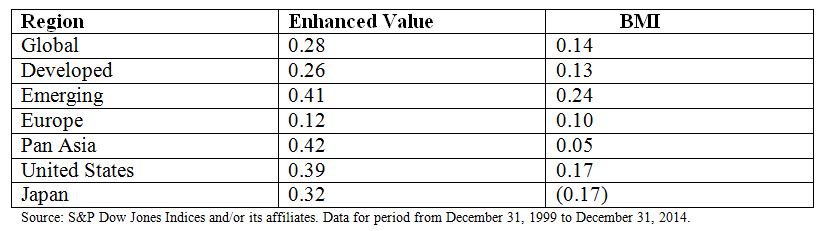

The soon-to-be-launched S&P Enhanced Value Indices* are an example of indices seeking to capture the value risk premium. They combine price-to-book, price-to-earnings, and price-to-sales (using the Z-score method) and select the top quintile of cheapest stocks. Constituent weights are computed as the product of the overall value score and the float-adjusted market capitalisation. Exhibit 1 displays the Sharpe ratios of the S&P Enhanced Value Indices and the relevant S&P BMI Indices over the past 15 years.

Exhibit 1 shows the successful capture of the value risk premium over the analyzed period.

For further insights, please register for one of our complimentary European seminars, entitled “Is Factor Investing a New Haven?”

*Index launch expected no later than April 2015.

[1] Fama, E.F. and French, K.R., (1996). Multifactor Explanations of Asset Pricing Anomalies. Journal of Finance. 51, 55-84.

[2] Lakonishok, J., Shleifer, A.,Vishny, R. W., (1994). Contrarian Investment, Exptrapolation, and Risk. Journal of Finance. Vol 69 (5), 1541-1578.

[3] EBITDA: earnings before interest, tax, depreciation, and amortization.

[4] Combining different factors (measures) can be achieved through the Z-score method. A Z-score is a stock’s standardized exposure to a factor. For each stock in an investment universe, subtract the universe’s mean factor exposure from the individual stock’s factor exposure. Then divide this number by the standard deviation of the factor exposures for the universe. Z-scores can then be added to derive an overall score and subsequent exposure to a set of factors.

The posts on this blog are opinions, not advice. Please read our Disclaimers.