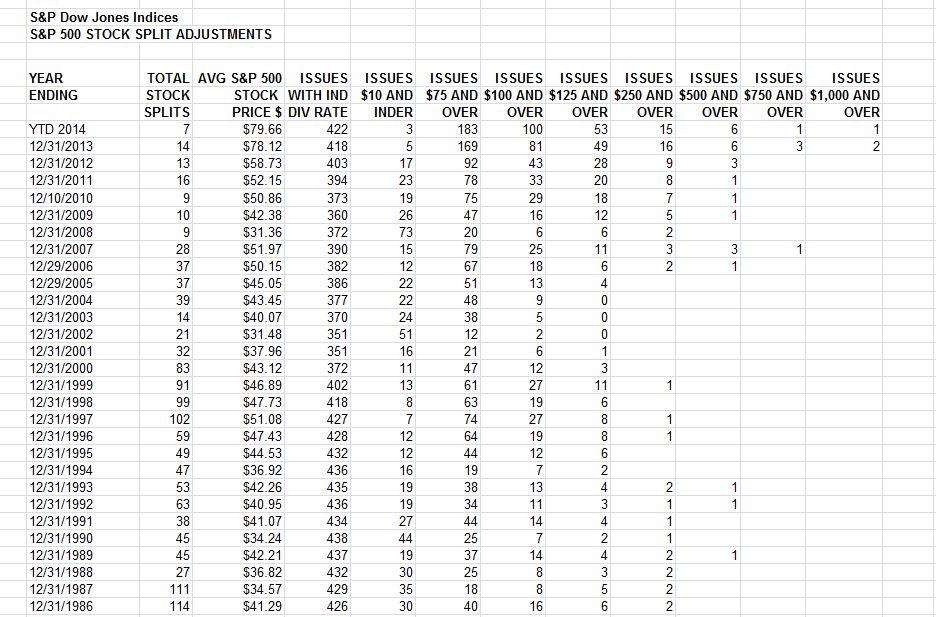

The key bar-room conversation this week has not been the stock market highs, or concern over elevated P/Es, or when a correction might arrive (the last one being in 2011 for big-caps), or even the increased M&A premiums being paid. It was stock splits, inspired by Apple’s 7-for-1 and the recollection, for those who have been on the Street for a few decades or more, and those newcomers who listened in, that in the 80s and prior, stock splits were money makers. Back then you actually paid cash for a service that sent a message (pre-twitter) to your beeper that a company had announced a planned split – and you would then purchase the stock – because it would go up (most likely).

The situation back then was that companies liked to keep their stock in a comfort zone, say $50 (for illustration), where investors felt comfortable buying and holding it. Additionally, old lots were inefficient in price and high in commissions (commissions were de-regulated in 1975, when brokerage consolidation slowly started and regulatory review was very show and long). Companies liked a broad base of individuals, which many felt gave support to the company; as compared to institutions which could be difficult (to put it nicely), or down-right unfriendly (Gulf & Devour). So when a stock reached a certain level, the company would split it, returning it to the comfort level (note: if $50 was the desired level, a 2-for-1 would most likely take place at $110 or higher, giving the company some protection in case the stock experienced a downdraft after the split – either because of company events or just market conditions). That thought process declined as quick trades came in along with the concept of capital appreciation only. Higher priced stocks were also becoming more acceptable, and the ability to purchase a dollar amount was made easier via brokerage consolidation, discount houses, and of course – the internet. Once we got past Y2K two recessions kept splits at bay (with the market sometimes splitting your stock in price, even though you did not get the extra shares).

Which brings us to Apple’s 7-for-1. There are many reasons why Apple split, but many believe it was to make its stock price, which was $646 per share before the split and $94 now, more attractive to individual investors, and broaden its investor base. Some even joked about a rebate program – buy a full-priced iPhone and get a share (not sure how that would work with disclosure or compliance). Also accepted was the idea that a border individual investor base could insulate the company from institutions and activists, who have been a bit more busy as company assets (especially cash) have grown. So, the question is – IF, yes IF, the lower price brings in more individuals (which would also add to buying and support the stock), and ‘assists’ with ‘dealing’ with certain holders, will more companies do it? Don’t know the answer, but as the Fed told the banks – I’ll be watching you.

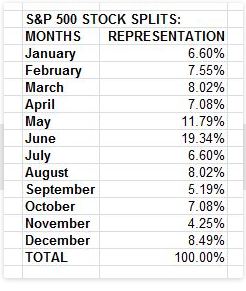

And while we all know that June is the most popular wedding month, it also appears to be the most popular split month (don’t know about divorces – still happy with my first)

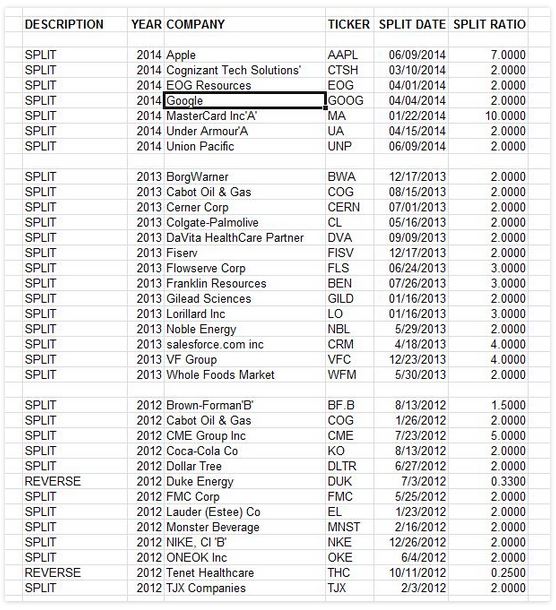

Recent Splits: