Think you’re saving money by holding onto that old car? Think again.

Since the recession, Americans have gradually held onto their cars for longer and longer because they have not wanted to spend money on new cars. Therefore, the average age of cars on the road has accelerated according to a recent survey from IHS Automotive. Also according to R.L. Polk, for 11 consecutive years ending in 2013, the average age of cars on the road has been increasing and is now 11.4 years old. Unfortunately, the intention of saving money by holding onto old cars may not be met since old cars may actually cost more.

Below is a list of America’s Top Ten Used Cars and their fuel economy estimates by MPG of the current 2014 models compared with 2002 models, to capture the gas usage from old cars versus new. Notice today’s models give on average 2.5 more MPG, so it may not be worth hanging onto an old clunker.

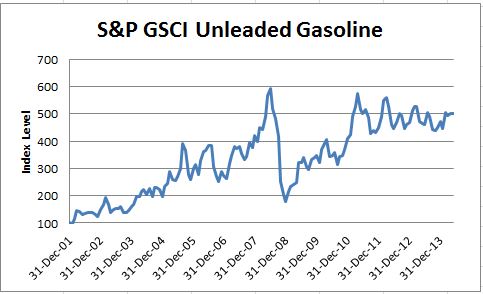

Not only might older cars have lower fuel efficiency but the price of gasoline as measured by the S&P GSCI Unleaded Gasoline has increased five-fold since the end of 2001.

Although the biggest price spikes historically occur in the winter from the transportation difficulty of petroleum, the prices typically heat up in the summer. The hottest summer month for gas prices is historically in July with an average monthly return of 2.8% since 2002.

Despite this, since 2002, the prices have gone up through time regardless of seasonality. See below the chart that measures prices by month through time. From Jan 2002- May 2014, prices have increased whether looking at every February, July or October.

With generally rising gas prices and lower fuel efficiency that are costly in terms of dollars, holding onto an old car may not be an optimal choice.

Further, keeping an old car with less gas mileage may be bad for the environment. According to the U.S. Department of Energy, one gallon of gasoline creates 20 pounds of carbon dioxide. With cars of an average age of 11.4 years, that use 2.5 MPG less than the new models of today, that adds up to 50 incremental pounds on average of carbon dioxide per mile. Given, there are 252.7 million cars on the road today, that is a lot of additional carbon dioxide. See below for annual tons of carbon dioxide per MPG. Just another reason to by a new car (or just ride a bike like I do.)

*Source: S&P Dow Jones Indices. Data from Dec 2001 to May 2014. Past performance is not an indication of future results. This chart reflects hypothetical historical performance. Please note that any information prior to the launch of the index is considered hypothetical historical performance (backtesting). Backtested performance is not actual performance and there are a number of inherent limitations associated with backtested performance, including the fact that backtested calculations are generally prepared with the benefit of hindsight.

The posts on this blog are opinions, not advice. Please read our Disclaimers.