Data as of May 1, 2014

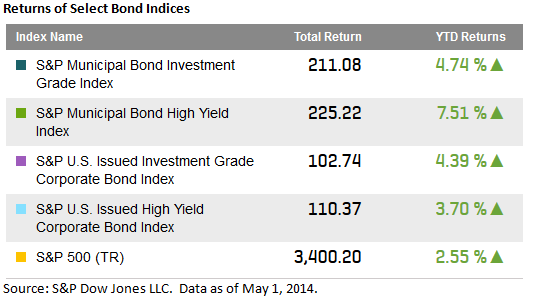

2013 was a not a fun year for municipal bond investors with bond prices and returns being pushed down by events in Detroit and Puerto Rico. 2014 is a different story, demand has shifted back to municipals as the S&P Municipal Bond Index has recorded a 4.91% total return, year to date. Yields of municipal bonds have come down at a faster clip than their counterparts in the U.S. Corporate bond markets. Since year end, investment grade municipal bonds tracked in the S&P National AMT-Free Municipal Bond Index has seen its yield drop to 2.24% (down 87bps) while the S&P U.S. Issued Investment Grade Corporate Bond Index yield ended at 2.82% (down 28bps). High yield municipal bonds, Puerto Rico and Tobacco Settlement bonds while volatile this year have shown strength as investors continue to seek incremental yield over low rate alternatives.