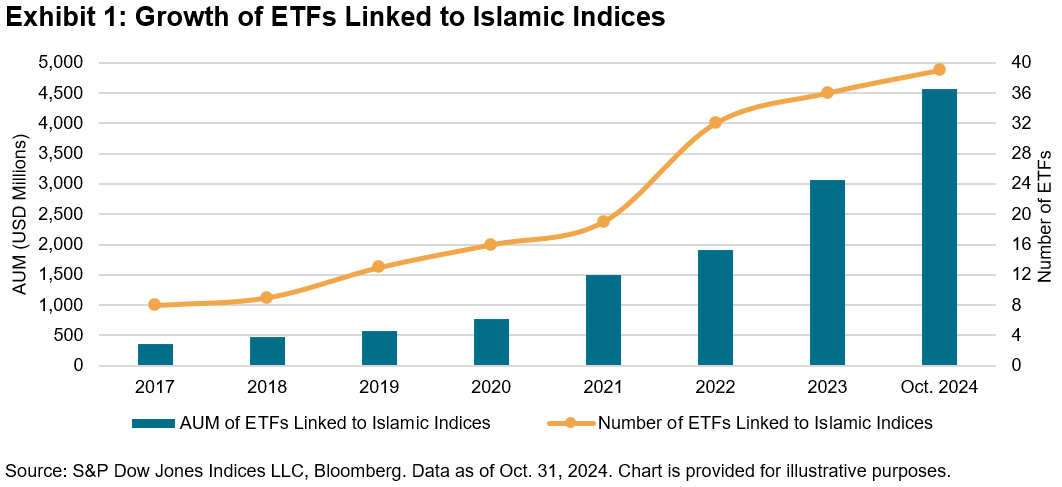

Indices play a crucial role in Islamic finance by identifying the universe of securities eligible for Shariah-compliant investments, establishing the benchmarks by which Islamic market participants assess performance and increasingly serving as the basis for index-linked investment products. Islamic finance has also embraced the global trend toward index-based or “passive” investing,1 with assets in exchange-traded funds (ETFs) linked to Islamic indices reaching USD 4.6 billion in 2024, a 49% increase YTD (see Exhibit 1).

Review of 2024

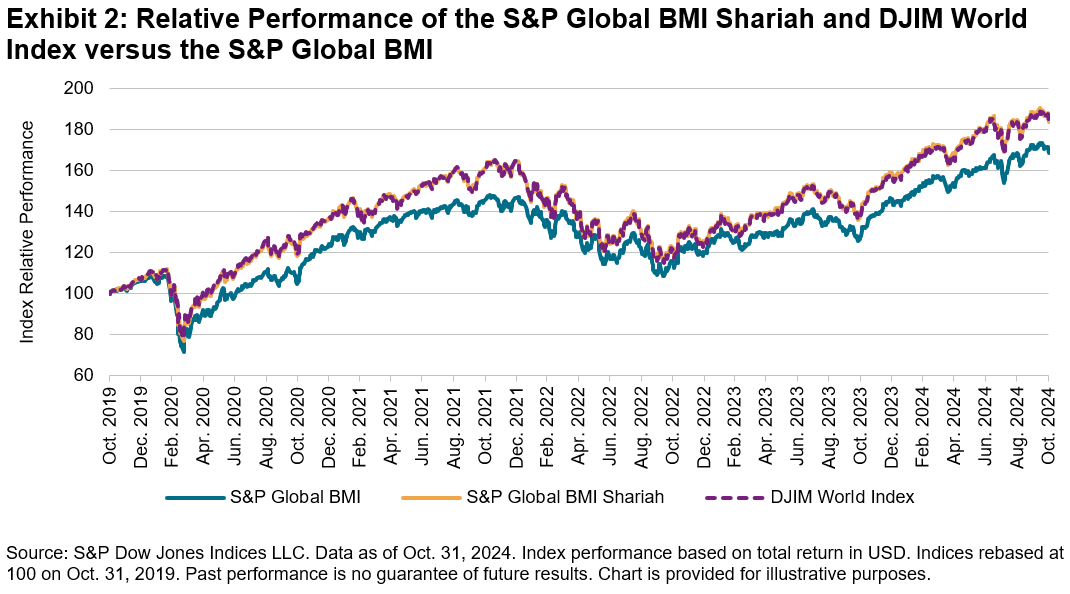

Global equities had a robust year, with the S&P Global BMI returning 15.4% by the end of October 2024. Shariah-compliant global equities outperformed slightly, with returns of 15.7% and 15.9% for the S&P Global BMI Shariah and Dow Jones Islamic Market (DJIM) World Index, respectively. Over the past five years, Shariah equity benchmarks have generated an excess return of more than 15% (2.0% annualized) over their conventional counterparts, as Exhibit 2 illustrates.

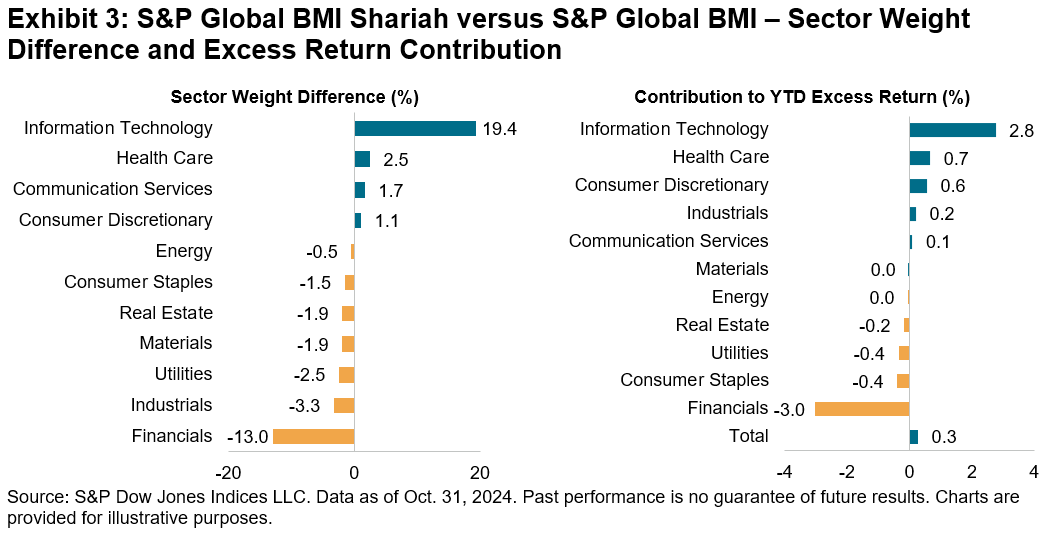

The relative performance of Islamic indices is partly attributable to their differing sector allocations. Information Technology, which accounts for 42.8% in the S&P Global BMI Shariah versus 23.4% in the S&P Global BMI, contributed 50% of the Shariah index’s return. This sector alone helped to generate an excess return of 2.8% against the conventional benchmark YTD. On the other hand, Financials brought the most significant negative effect on the index with a -3.0% excess return. This was due to its reduced weightings (3.6% in the S&P Global BMI Shariah versus 16.6% in the S&P Global BMI) as well as the underperformance of Shariah-compliant Financials companies against non-compliant ones (see Exhibit 3).

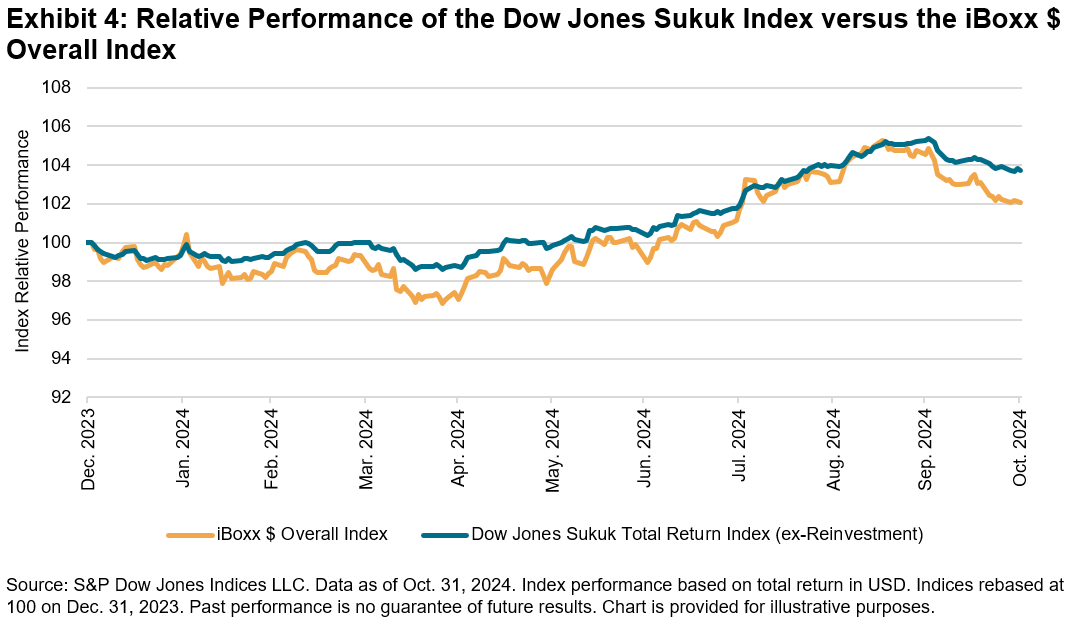

Meanwhile, fixed income markets were sluggish initially but rose in Q3, with U.S. dollar-denominated investment grade bonds (as measured by the iBoxx $ Overall Index) gaining 2.1% YTD as of the end of October 2024. Its sukuk equivalent, the Dow Jones Sukuk Index, had a higher return of 3.7% due to a larger compression in credit spreads and the lower duration of sukuk issues, which made them less sensitive to the repricing of rates2 (see Exhibit 4).

Against this backdrop, as already indicated by Exhibit 1, ETFs linked to Islamic indices have seen notable inflows. While the largest portion (46%) of assets under management are associated to U.K. primary listings, assets in U.S.-listed ETFs grew by 82% YTD and now account for 42% of the total. Islamic ETFs are predominantly in the broad-market equities space (94% of the total assets under management), while sukuk ETFs are growing fast with a 73% YTD increase as of the end of October 2024.

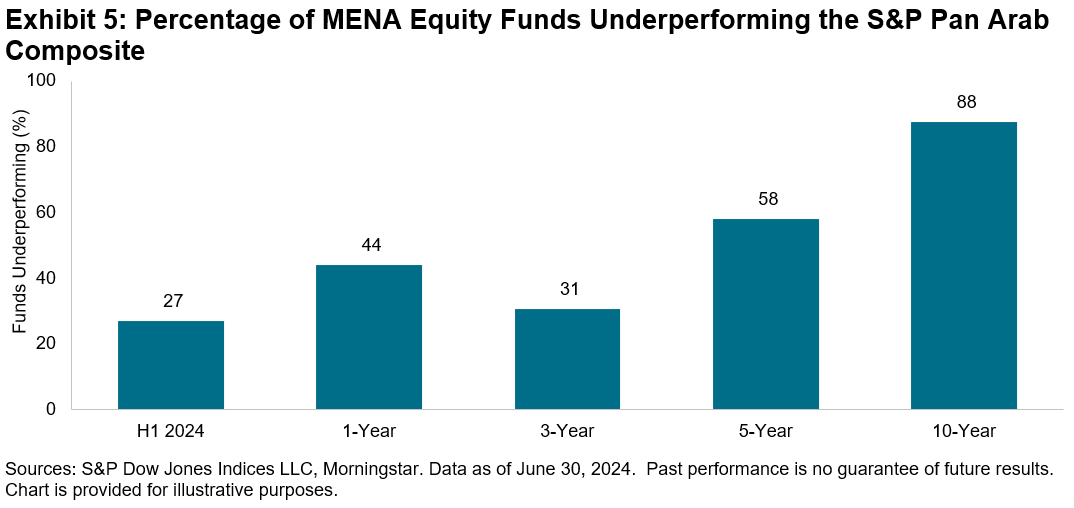

In the Middle East and North Africa (MENA) region, passive investing is still in its early stage. However, the U.A.E. and Saudi Arabia have been leading the development of the local ETF markets and introduced several new ETFs this year. The benefits of passive investing are resonating with MENA-based market participants, supported by empirical evidence from the S&P Indices versus Active (SPIVA®) research. Despite relatively encouraging results in H1 2024, actively managed MENA equity funds largely underperformed the S&P Pan Arab Composite over a 10-year period, as illustrated in Exhibit 5.3

Looking Ahead

A significant trend in Islamic indexing is the emergence of ESG Shariah solutions and increased interest in this space. Shariah and ESG principles share some common goals, such as promoting social and environmental stewardship. The S&P Pan Arab Composite ESG Shariah Capped Index exemplifies this concept, as the index measures the performance of the 40 companies with the highest-ranking ESG scores among the 60 largest constituents of its benchmark, the S&P Pan Arab Composite Shariah Index. Since its launch in May 2022, the index has achieved ESG score improvements and better temperature alignment, along with marginal outperformance compared to its benchmark.4 We will continue to observe how indexing evolves to help align Islamic values and ESG goals.

There are also some challenges ahead. In late 2023, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), the Bahrain-based supervisory body for Islamic finance standards, released a draft standard aimed at redefining the concept and structure of sukuk.5 The proposal requires that sukuk be backed by underlying assets rather than merely referencing these assets in their structure, as has been the practice. S&P Global Ratings has stated that adopting this new standard could disrupt the market, lead to further market fragmentation, dampen the appetite of both investors and issuers, and potentially halt new issuance until sukuk structures find a middle ground.6 The publication and effective date of the standard are still unknown, and it remains to be seen how the final standard will be enforced and how the sukuk market will adapt in 2025.

Conclusion

The landscape of Islamic index-based investing is evolving, driven by increasing market participant demand and the adoption of global market trends. The outperformance of Shariah-compliant indices and the rapid growth of associated ETFs underscore the potential for passive investment strategies in this sector. However, challenges such as regulatory changes and market fragmentation must be addressed to maintain this momentum. As the market continues to adapt, ongoing innovation and alignment with market participant values will be essential for the future success of Islamic indexing.

This article was first published in IFN Annual Guide 2025.

1 See It’s Official: Passive Funds Overtake Active Funds, Morningstar, January 2024

2 As of the end of October 2024, the Dow Jones Sukuk Index had 4.35 years of effective duration and a yield of 4.89% with a 67 bps spread over U.S. Treasury bonds. In comparison, the iBoxx $ Overall Index had 5.99 years of duration and a yield of 4.85% with a 40 bps spread.

3 See SPIVA Global Mid-Year 2024, S&P Dow Jones Indices, October 2024

4 See Where Shariah Meets ESG, S&P Dow Jones Indices, July 2024

5 See AAOIFI Shariah Board Ratifies Landmark Sukuk Standard Draft, Solicits Banking and Regulatory Sector Feedback, AAOIFI

6 See Sukuk Market: The Calm Before the Storm?, S&P Global Ratings, July 2024

The posts on this blog are opinions, not advice. Please read our Disclaimers.