Large-cap, Australian-listed companies have continued their robust 2022, outperforming the small- and mid-cap segments YTD as of April 30, 2023. However, a fast-changing economic environment may support considering small and mid-cap indices in Australia.

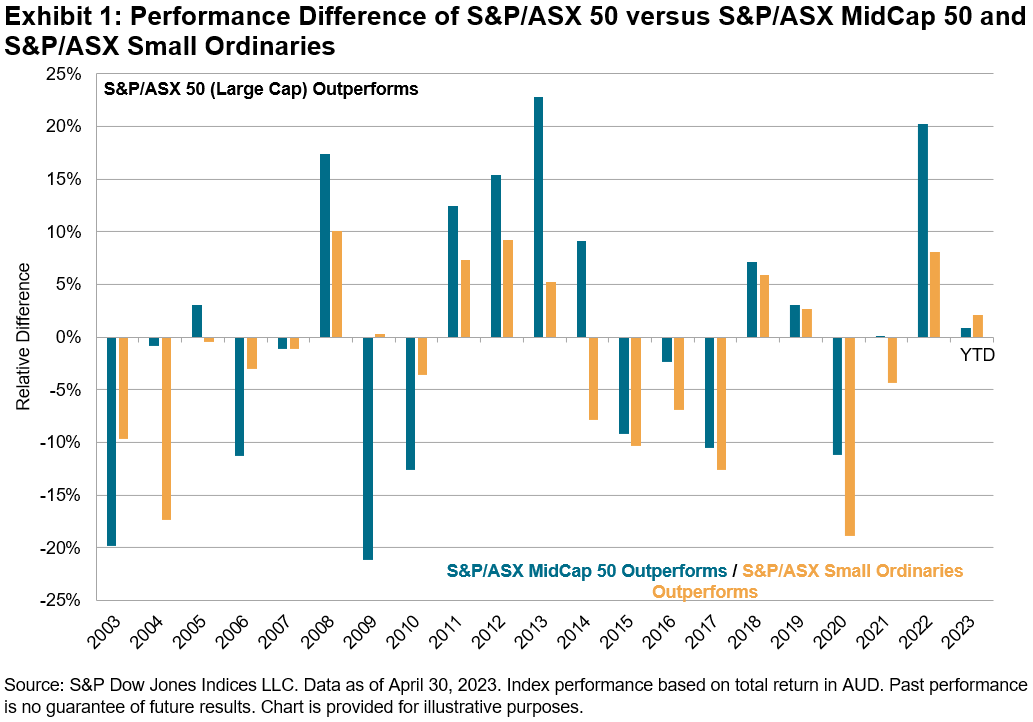

The range of returns for Australian-listed companies in 2022 was among the widest seen in 20 years. Broad dispersion was exhibited across sector, style and market cap segments. The calendar year outperformance of large (S&P/ASX 50) versus small- and mid-cap companies (S&P/ASX Small Ordinaries and S&P/ASX MidCap 50) was 20.28% and 8.14%, respectively. This is the second-largest outperformance of large versus small and mid-caps over the past 20 years.

Mid- and Small-Cap Indices Offer Sector Diversification

Financials make up over 30% of the S&P/ASX 50 and 5 of its top 10 companies by index weight. The big four banks (CBA, NAB, ANZ and WBC) have benefited from rising interest rates and investor preference for dividend income in an inflationary environment. Different segments and sectors may out- or underperform during the various stages of an economic cycle. As inflationary pressures abate and interest rates seemingly level out, mid- and small-cap indices may offer diversification benefits away from the banks.

Presently, the S&P/ASX Small Ordinaries has more exposure to Consumer Discretionary and Real Estate companies, while the S&P/ASX MidCap 50 has more weight in Industrials and Information Technology companies relative to the small- and large-cap indices.

Small Caps Offer Most Compelling Relative Valuations

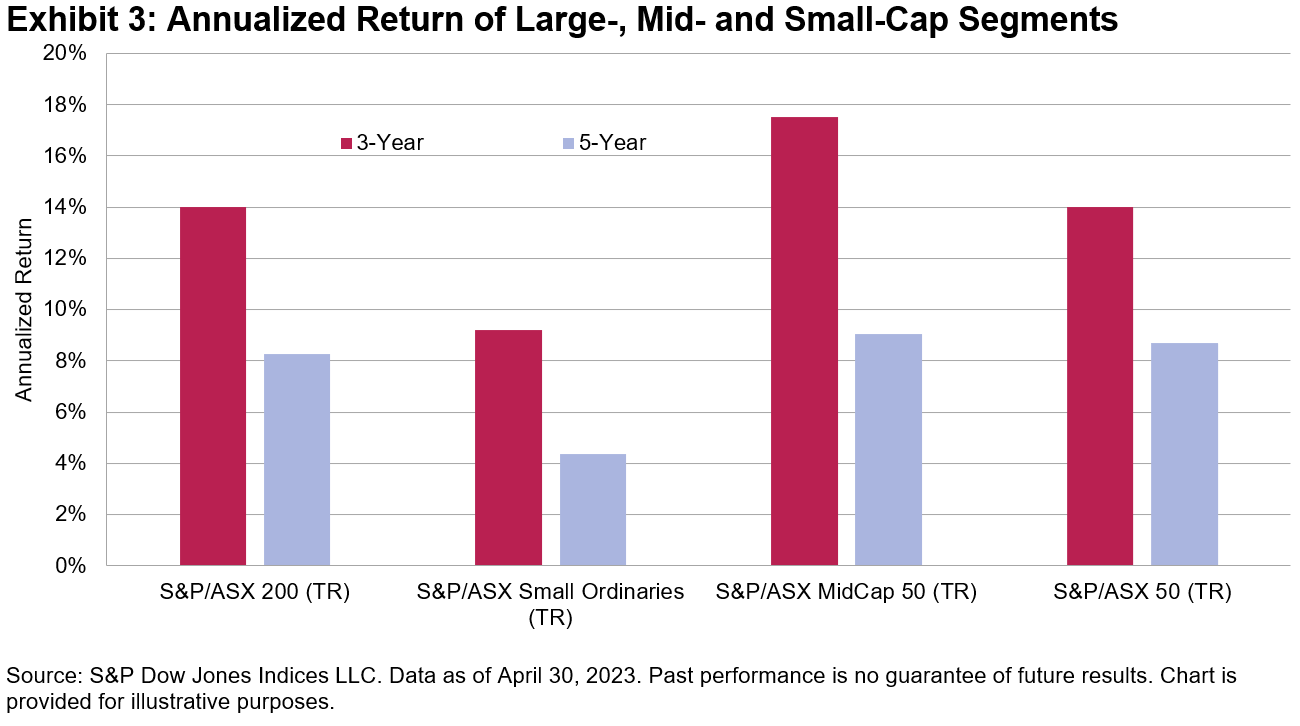

The different composition of the market cap segment indices has resulted in distinctive performance outcomes. As of April 30, 2023, mid-caps were the best-performing market segment over the three- and five-year periods. The S&P/ASX Small Ordinaries has underperformed during this period, however, it does exhibit the most compelling relative valuations.

The trailing 12-month price/earnings ratio for the S&P/ASX Small Ordinaries and S&P/ASX Mid Cap 50 are well below their long-term average, at approximately 9x and 14x earnings, respectively. Meanwhile, the three-year average of the 12-month trailing P/E ratio for the S&P/ASX Small Ordinaries recently moved lower than the S&P/ASX 50 for the first time in over 10 years.

Mid- and Small-Cap Active Managers Underperformed in 2022

Advocates of active management often argue there is more alpha to be found in the mid- and small-cap space. Furthermore, the broad dispersion of returns exhibited in 2022 is said to provide more of an opportunity set for skilled stock picking. However, S&P DJI’s SPIVA® Australia Year-End 2022 Scorecard shows just 23.4% of Australian Equity Mid- and Small-Cap active funds beat the S&P/ASX Mid-Small in 2022, while over 80% underperformed on a risk-adjusted basis. Funds in this category lost 19.8% and 22.0% on equal- and asset-weighted bases, respectively, for the same period.

The posts on this blog are opinions, not advice. Please read our Disclaimers.