For the first time, our SPIVA® Europe Year-End 2022 Scorecard measures the performance of actively managed fixed income funds, covering 11 categories across currencies and credit quality. Fixed income funds had a better record than their equity brethren in 2022, with a majority of funds outperforming in five reported categories over a one-year horizon (compared to none of our 22 equity categories). At the front of the pack, just 23% of euro-denominated government bond funds underperformed the iBoxx Euro Sovereigns in 2022. Admittedly, the results were less impressive as the time horizon extended: a cross-category average of 84% of active fixed income funds underperformed their assigned benchmark over the 10-year period, including 88% of euro-denominated government bond funds.

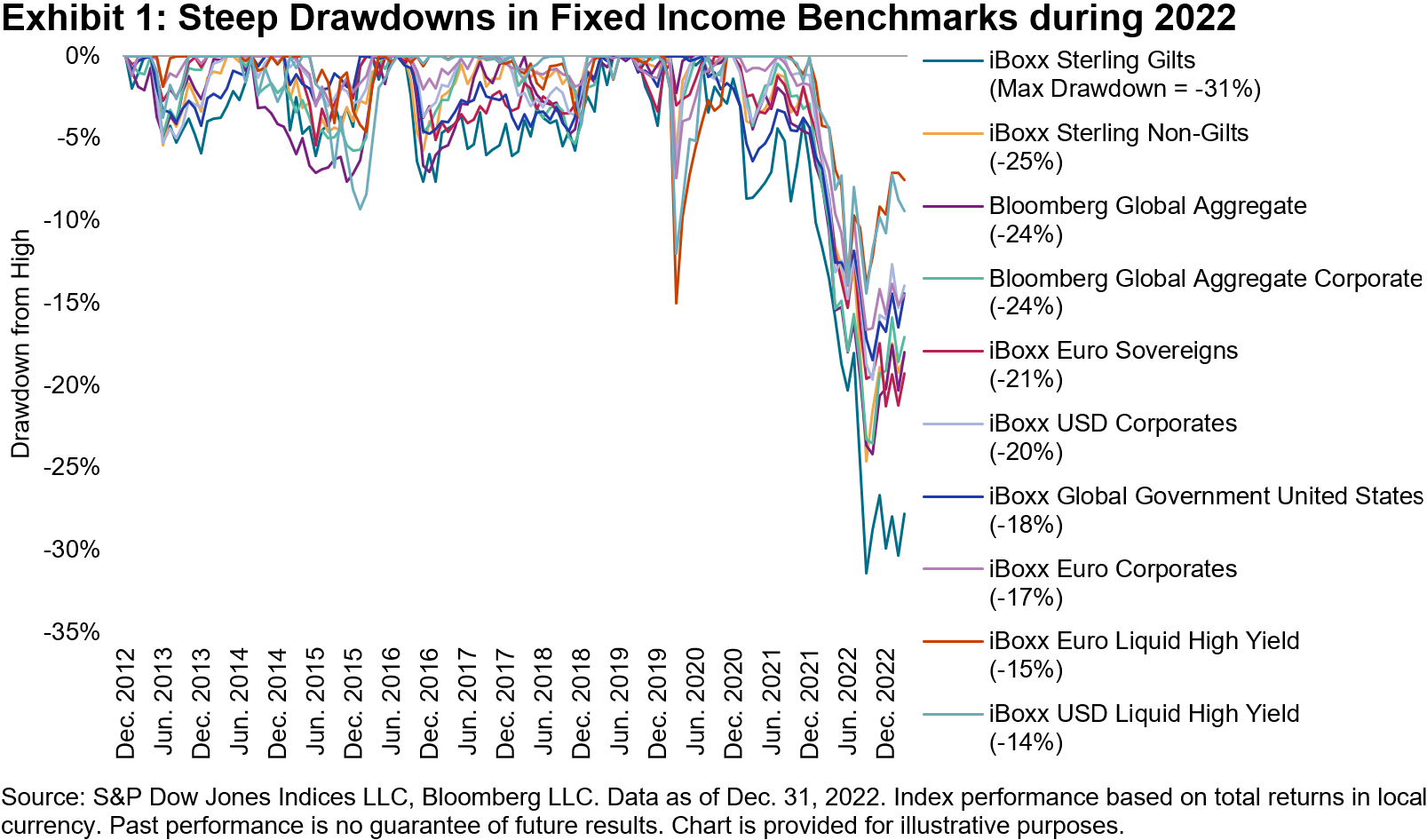

To say that 2022 was a challenging year for bonds globally is an understatement. Central banks around the world tightened interest rates to combat inflation, leading to double-digit losses for most European fixed income benchmarks, accompanied by particularly large declines in longer-dated bonds, which are more sensitive to changes in interest rates. Exhibit 1 shows the extent of 2022’s declines in our fixed income benchmarks in a decade-long historical context. At the back of the pack, the iBoxx Sterling Gilts recorded a maximum drawdown equal to a 31% decline from its 2020 high, finishing the year not far from its lows.

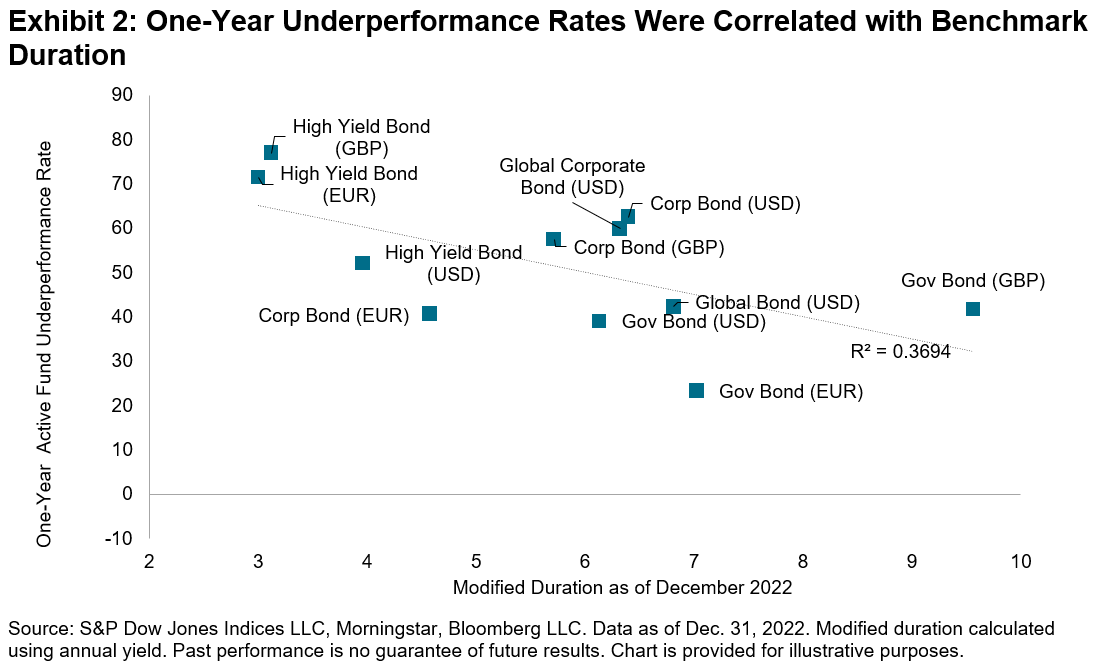

Despite the carnage, there were a few bright spots for actively managed funds, particularly in categories with benchmarks that were more sensitive to changes in the yield environment. Exhibit 2 plots the relationship between the one-year active underperformance rate in each fixed income category and rate sensitivity in that category’s benchmark, as measured by modified duration. The two series are negatively correlated, which suggests that some active managers may have generated their relative outperformance by holding bonds with shorter maturities, on average, than their category benchmark.

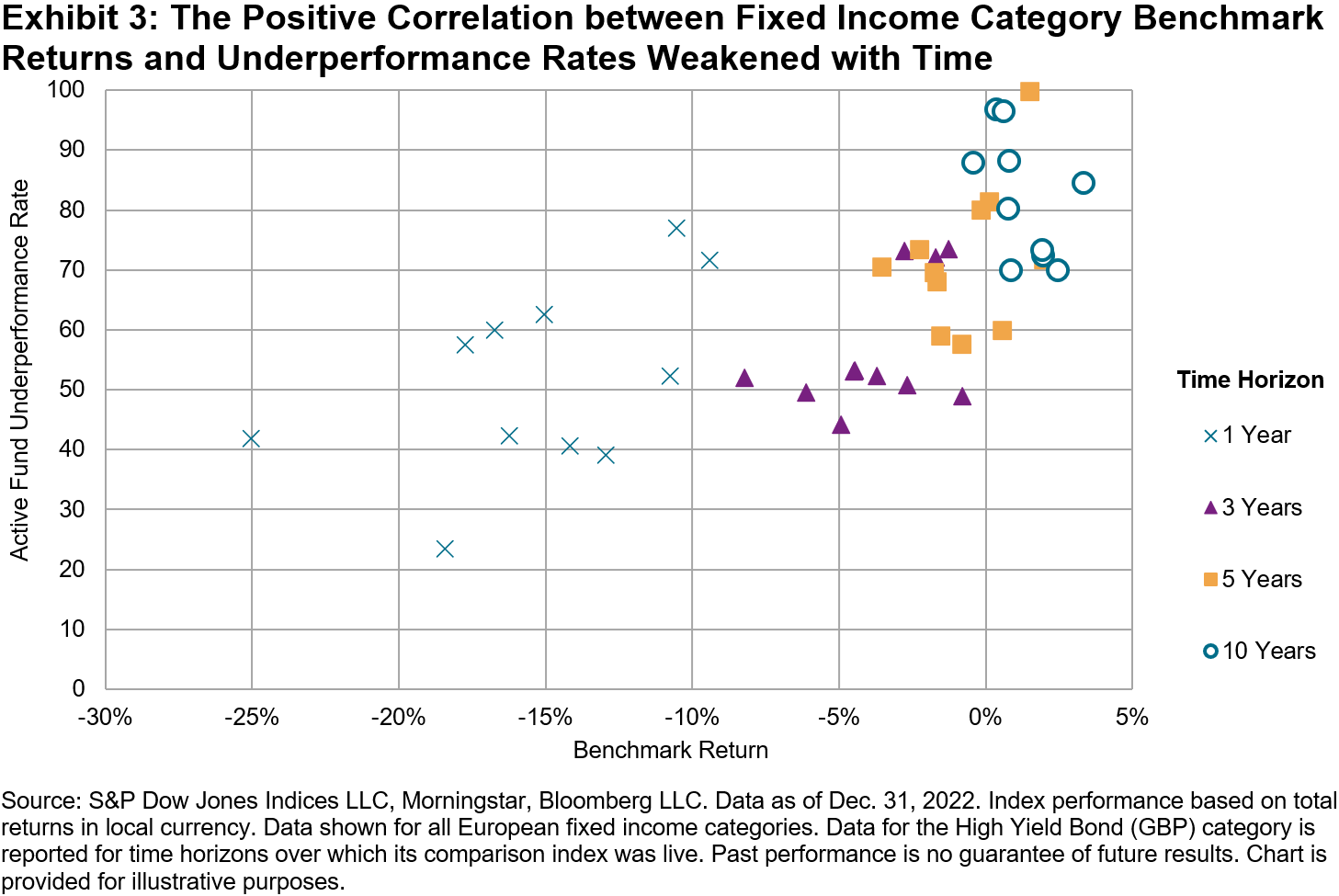

While conditions were particularly auspicious for fixed income managers with poorly performing benchmarks in 2022, such tailwinds may not persist over the long-term. Exhibit 3 shows that the relationship between benchmark returns and underperformance rates progressively weakens as the time horizon extends to 3, 5, and then 10 years. Just as Tim Edwards observes within European equities, the evidence suggests that is no easy task to identify active fixed income managers who can beat benchmarks over the long term.

The posts on this blog are opinions, not advice. Please read our Disclaimers.