The inaugural S&P Indices versus Active (SPIVA®) U.S. Scorecard was published in 2002, and has since been extended to Australia, Canada, Europe, India, Japan, Latin America, South Africa and the Middle East & North Africa (MENA), allowing investors to experience the active versus passive debate on a global scale.

The SPIVA Japan Scorecard measures the performance of actively managed funds domiciled in Japan against their respective S&P DJI comparison benchmarks over various time horizons, covering large-, mid- and small-cap, as well as international and global equity funds.

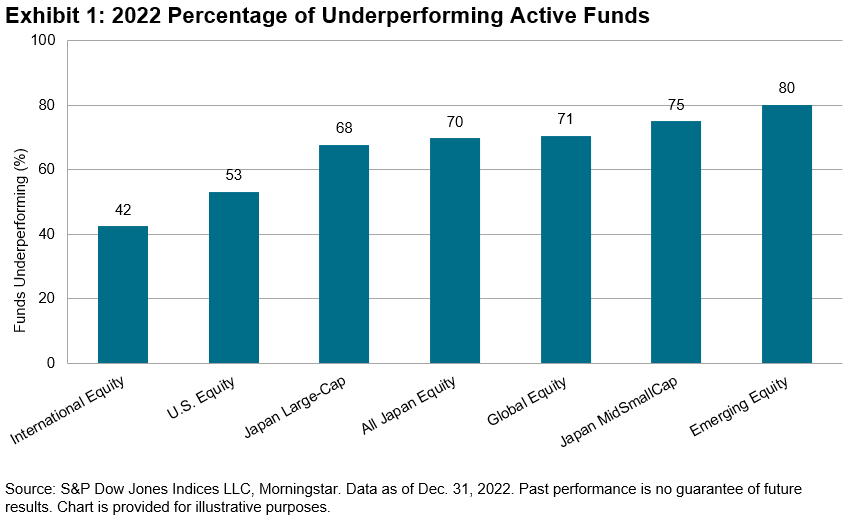

According to the recently published SPIVA Japan Year-End 2022 Scorecard, 70% of All Japanese Equity funds underperformed the broad-based S&P Japan 500 over the full-year 2022, and more than half of equity funds underperformed their benchmarks in every reported category, except for International Equity funds, which had an underperformance rate of 42% (see Exhibit 1).

Several aspects of the market environment in 2022 stood out as potentially indicative of a favorable environment for active managers in Japanese equities over the period. For example, the largest companies (as represented by the S&P/TOPIX 150) had lower returns than small- and mid-sized Japanese companies (as represented by the S&P Japan MidSmallCap; see Exhibit 2). This potentially created a tailwind for active managers, as funds are typically less likely to own all the largest stocks at market weight.

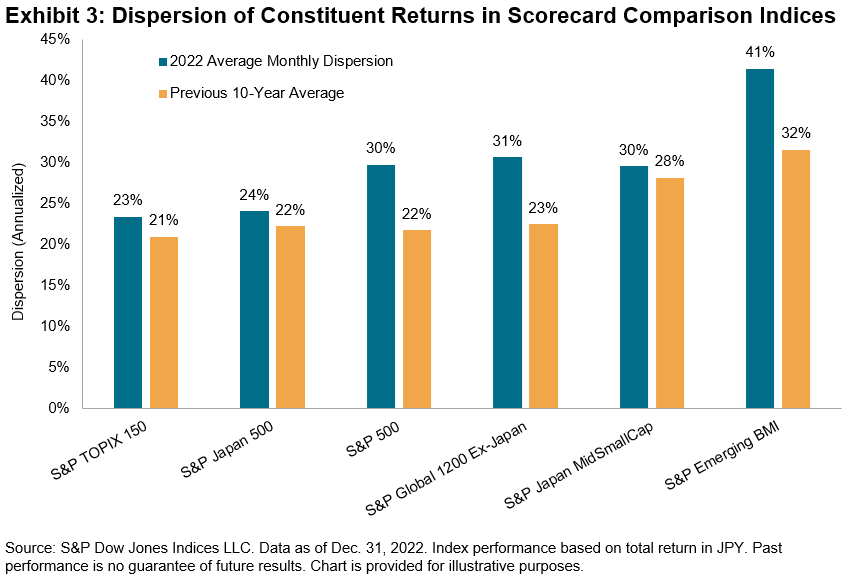

Second, opportunities for outperformance through stock selection were plenty in 2022. At the benchmark level, dispersion is the measure of the degree to which securities differ—above or below—the average performance.1 As illustrated in Exhibit 3, the average monthly annualized dispersion in the securities of the scorecard comparison indices was higher in 2022 than was typical over the past 10 years.

Due to the costs associated with running any portfolio, an actively managed fund may still underperform even if it picks outperforming securities. For an active manager, the key is to find not just securities that outperform, but those that outperform materially. At times when most securities perform similarly, differentiation is surely harder to find. Then, there are other times when the difference between winners and losers is larger.

Taken all together, the data in the SPIVA Japan Year-End 2022 Scorecard suggest that among the active funds offered in Japan, International Equity managers were relatively more successful in turning opportunities into positive outcomes. However, active funds in all the other fund categories struggled to take advantage of the abundance of opportunity presented in 2022’s market environment.

1 For example, see Edwards, Tim and Craig J. Lazzara, “Dispersion: Measuring Market Opportunity,” S&P Dow Jones Indices, 2014.

The posts on this blog are opinions, not advice. Please read our Disclaimers.