As time passes, we draw ever closer to the date of the GICS® changes scheduled to take effect after the market close on March 17, 2023. There are five changes being implemented, some of which will move companies among sectors and others that will move companies within sectors.

Recent blogs have announced these changes: GICS changes are approaching considered the adjustments occurring in 6 of the 11 sectors and the resulting weights. The biggest changes will be a reduction in the Information Technology (IT) sector weight (-3.2%), with the balance heading to Financials (2.7%) and Industrials (0.5%). It also identified the changes in industry groups, industries and sub-industries.

A second blog (2023 GICS Change: S&P 500® Impact Analysis) dug deeper into the impact on the S&P 500. It highlighted the names of the 14 companies moving across sectors, a result of reclassifying certain companies to better reflect their underlying business activities.

This third blog aims to dig deeper still; does the moving of companies across sectors lead to a difference in the geographic diversification of revenues within sectors? We know that all the companies within the S&P 500 index are domiciled in the U.S., but their revenues are global in nature (See Exhibit 1 for a breakdown).

Utilizing the new sector classifications and the geographical revenue distribution of companies (derived from FactSet), we construct the geographical sales-weighted effect of the GICS changes across sectors.

![]()

The majority of sectors are unchanged. Exhibit 2 shows the distribution of revenues by geography for those sectors that are undergoing change.

The largest change in geographic revenues occurs within the U.S. for all sectors. This is as expected, as 69% of revenues in the S&P 500 come from the U.S. We note that the re-categorization of Data Processing and Revenue Outsourcing companies away from the IT sector led to an approximately 4% proportional revenue loss from the sector’s U.S. geography.

It’s also interesting to note that although Consumer Staples only has a 0.5% increase in weight, the impact to revenue from the U.S. for the sector is much greater, at 2.4%. Relocating the highly U.S.-focused businesses of Target, Dollar Tree and Dollar General from Consumer Discretionary to Consumer Staples has driven the latter sector to see a greater weight to the U.S. Finally, we noted small changes to the China and Taiwan revenue footprints for IT. This was a result of the reduction in overall U.S. revenues and reflective of where some of the largest markets for the sector are found.

Not all sectors are created equally. Exhibit 3 shows the percentage of U.S. revenues for all eleven sectors. We highlighted in red the five sectors that are affected by the upcoming GICS changes.

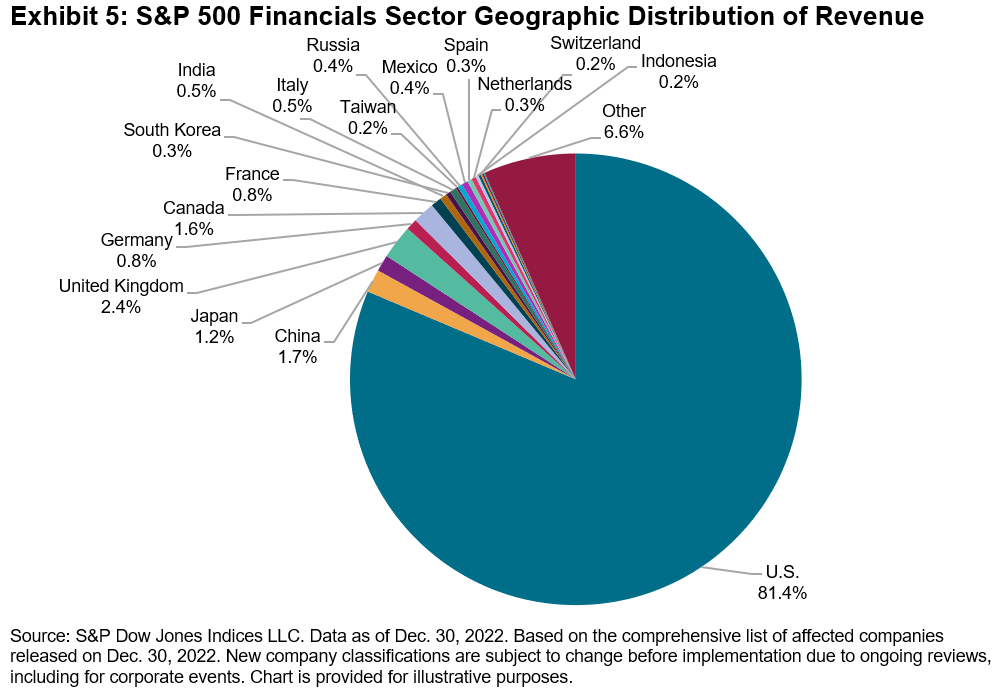

From a geographic revenue standpoint, IT is the most diversified sector, with only 44% of revenues driven by the U.S. This percentage will be reduced further due to the removal of Data Processing and Outsourced Services companies, which will move to either Financials or Industrials. This same change will increase the concentration of Financials in the U.S. from 80.3% to 81.4%.

To further illustrate the geographical spread among revenues and the impact of the GICS changes, the graphs below show the distribution of the Financials and IT sectors. IT is the most diverse sector, c. 44% of revenues are derived from the U.S. with China, Japan and Taiwan heavily represented in the geographical revenue distribution. The Financials sector is highly concentrated in the U.S. with the U.K., the next largest country, only providing around 2% of revenues.

Analyzing geographic revenues provides us with a complementary way to understand the upcoming GICS changes. While some companies are changing sectors within the S&P 500, the distribution of geographic revenues is not changing dramatically. The possible diversification benefits of U.S. equities via the S&P 500 remain.

For more information, please refer to our GICS changes pages here.

The posts on this blog are opinions, not advice. Please read our Disclaimers.