Index funds, which hardly existed 50 years ago, now play a prominent role in global financial markets. But passive investing does not dominate in every market segment. Recently, we have seen exponential growth in so-called “thematic” investing, with a proliferation of themes in areas like cybersecurity, robotics and electric vehicles. This more granular space is sometimes perceived to offer greater opportunities for active stock selection, as opposed to an index-based approach.

In traditional categories, passive investors have benefited substantially by saving on fees and avoiding active underperformance. Our recently released paper, The Case for Indexing Thematics with the S&P Kensho New Economies, shows that very similar principles may apply to the thematics space.

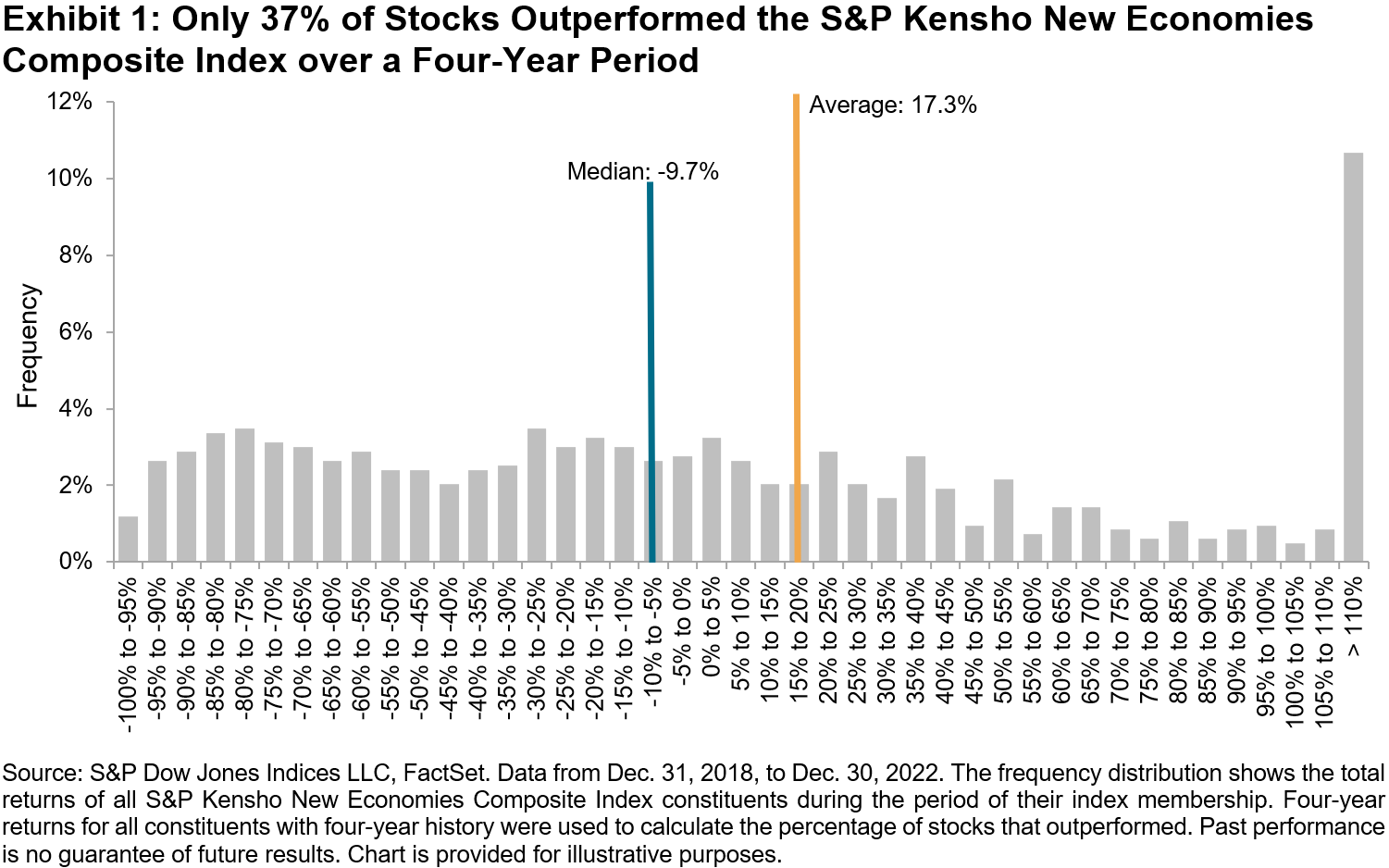

In the case of broad equity markets, one important cause of the difficulty in outperforming through the selection of single stock “picks” is that in most markets, the distribution of single stock returns is positively skewed, with the result that only a minority of constituent stocks outperform the index, particularly as the time horizon extends. The universe of stocks defined by the S&P Kensho New Economies Composite Index proves to be no exception. Exhibit 1 plots the distribution of cumulative returns of the index constituents over the past four years: the median return of -9.7% is far less than the average of 17.3% and, during the period, only 37% of stocks outperformed the index.

This highlights the difficulty for thematic active managers seeking to outperform with concentrated portfolios, because when faced with a distribution of returns that is positively skewed (like in Exhibit 1), holding more stocks increases the likelihood of outperformance. The problem is of particular concern in the thematics space because, given the inherently granular nature of certain themes, the challenge of avoiding undue concentration is especially germane. For example, there are only 31 constituents within the S&P Kensho Robotics Index, one of the 25 subsectors that make up the 559 constituents within the S&P Kensho New Economies Composite Index (as of Dec. 30, 2022). In addition to being diversified across themes, the composite index’s concentration is further mitigated by a modified equal-weight approach applied in the construction of each subsector. The result of all of which is an index that is less concentrated than would be the case if a simple market-cap weighting scheme were followed.

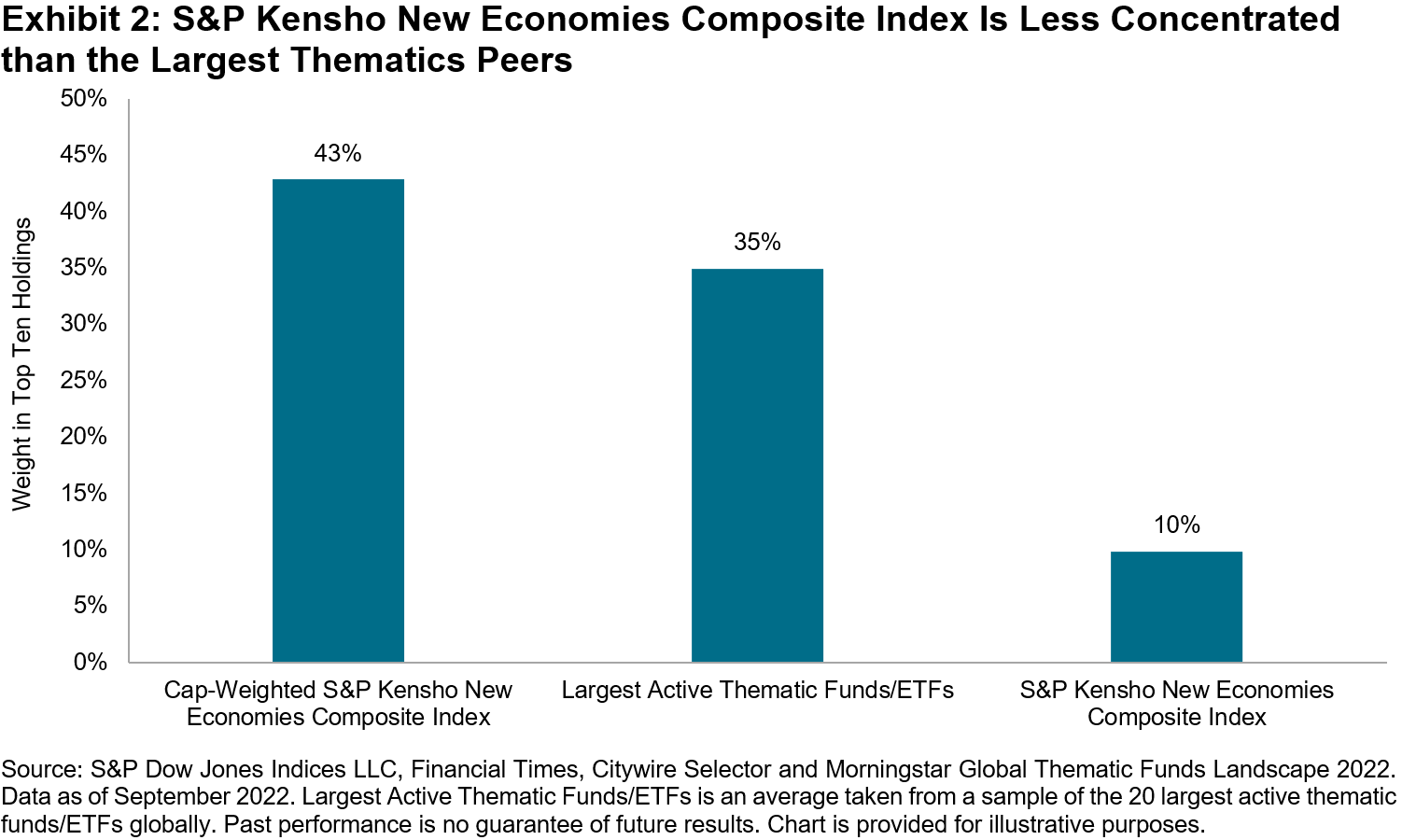

Exhibit 2 illustrates the relative difference in concentration levels observed in the S&P Kensho New Economies Composite Index, its market-cap-weighted equivalent, and the average of the 20 largest actively managed thematic funds. We use a simple measure of concentration, namely the aggregate weight of the 10 largest constituents, because it is freely available for the active funds; interested readers can find further analysis of index concentration in our paper.

The largest active funds appear, on average, much more concentrated that the S&P Kensho New Economies Composite Index, with on average 35% of their portfolios’ weight in the top 10 holdings, compared to only 10% for the index. Meanwhile, if the composite index was capitalization weighted, its concentration levels would have been even higher, with 43% of its weight in the top 10 holdings.

Considerations such as these help explain why thematic investing may be ripe for “indicization,” in which the well-known benefits of passive investing might be captured through benchmarks such as those in the S&P Kensho New Economies. In short, thematics appears to be yet one more segment of the investment landscape where, to put it simply: indexing works.

The posts on this blog are opinions, not advice. Please read our Disclaimers.