S&P Dow Jones Indices (S&P DJI) offers style and pure style indices, which categorize companies based on their growth and value characteristics. We recently published the paper Comparing S&P Style & Pure Style Indices, where we highlighted differences in design, fundamentals and potential applications for both index series.

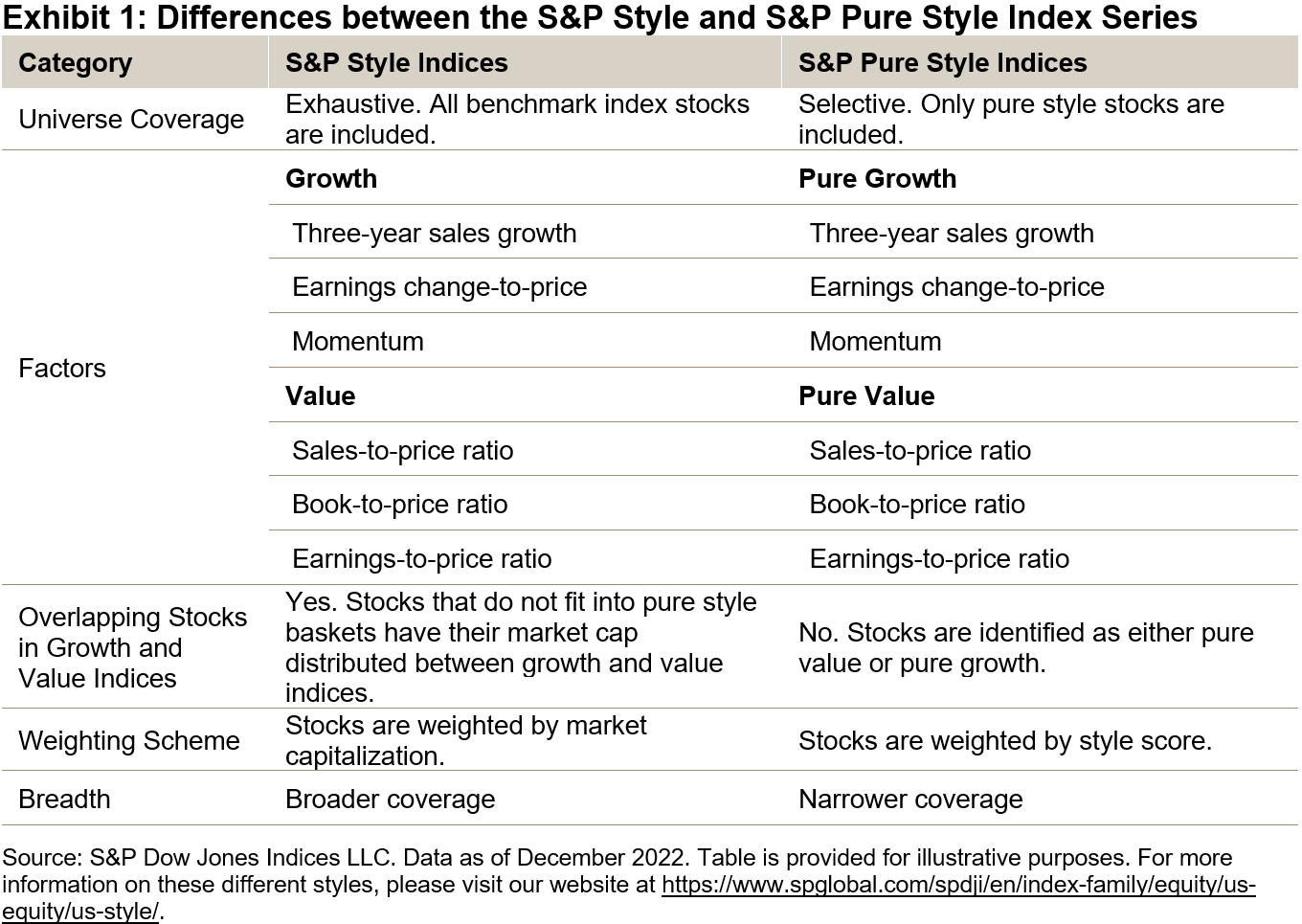

Exhibit 1 summarizes the index construction of the two series. S&P Style Indices provide broad style exposure, covering all stocks in the benchmark universe and dividing the benchmark weight into roughly equal portions at each annual reconstitution. S&P Pure Style Indices have a more selective focus and weight companies by their style scores, rather than in proportion to their float market capitalization. Both series use the same six factors to define growth and value.

Differences in index construction help to explain the different constituent counts in the two types of indices. For example, Exhibit 2 shows that companies can be found in both growth and value indices, whereas there is no overlap between the pure growth and pure value indices. The pure style baskets also contain fewer constituents than their style counterparts, reflecting a more selective approach to style exposures.

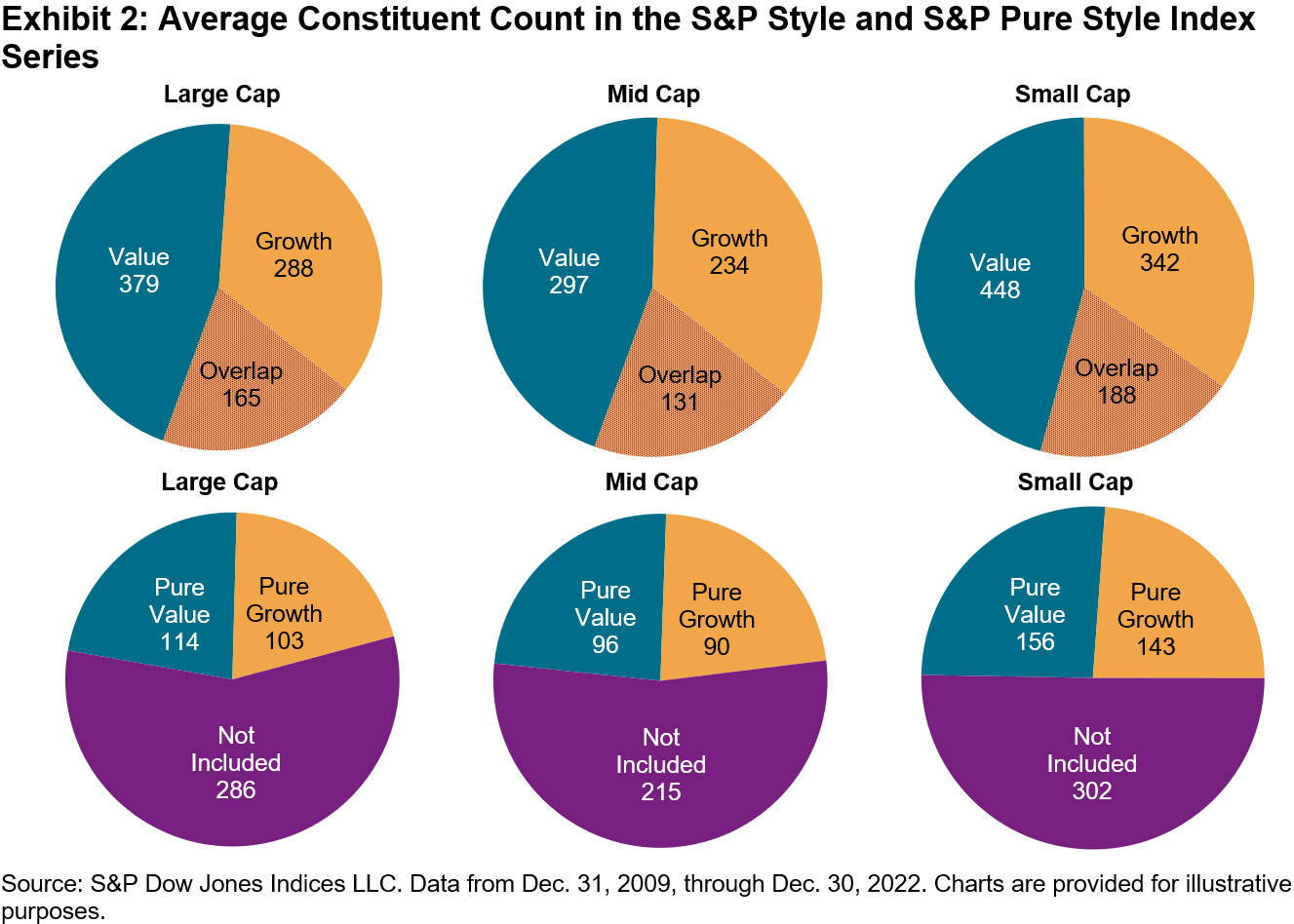

The selective focus of pure style indices means that S&P Pure Value and Pure Growth Indices reflect stronger value and growth characteristics than their style counterparts. Exhibit 3 shows this by comparing the average annual fundamental ratios of various indices: pure value indices typically had lower price-to-earnings, price-to-book and price-to-sales ratios, while pure growth indices had higher three-year sales growth and three-year EPS growth rates.

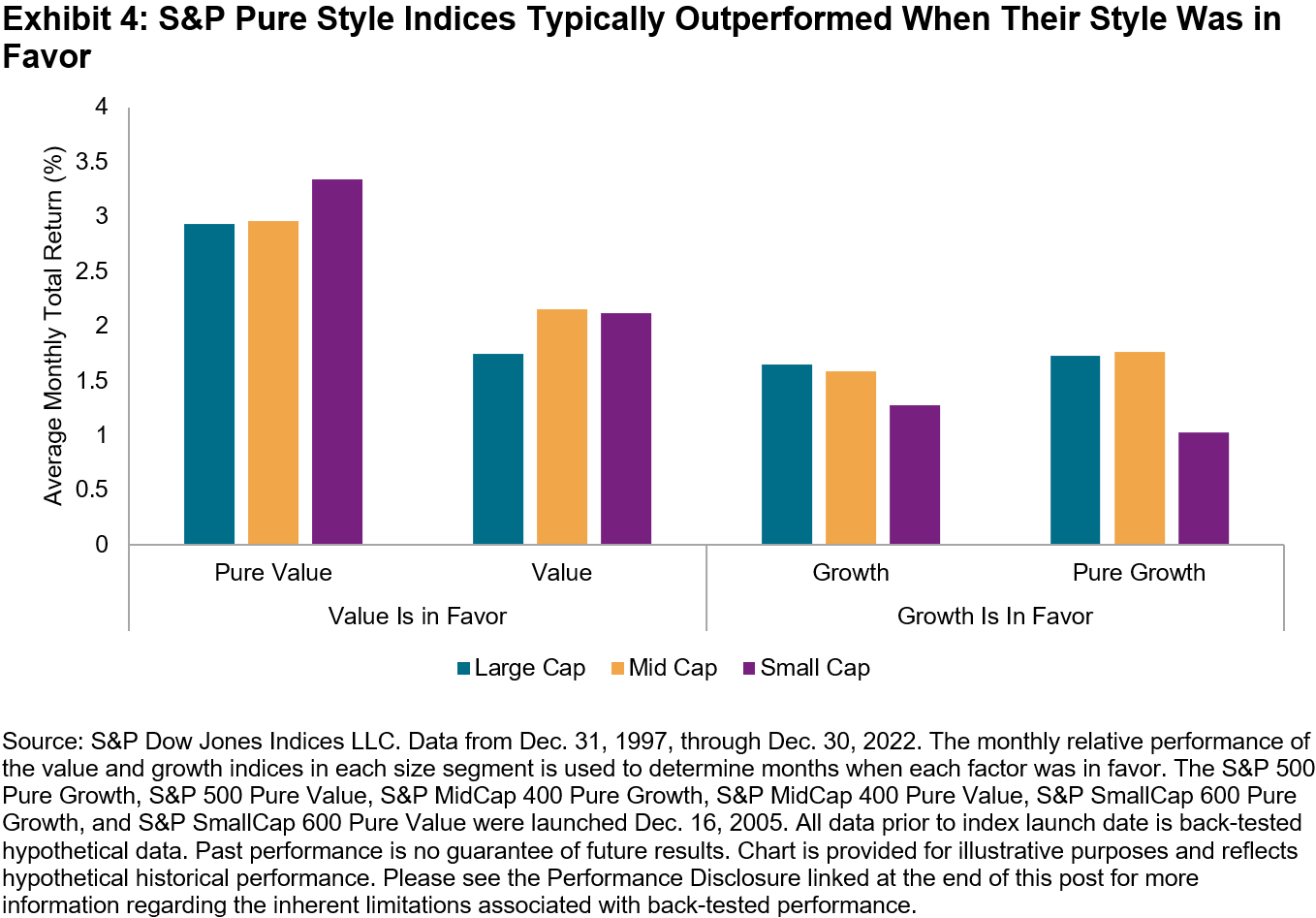

Unsurprisingly, perhaps, Exhibit 4 shows that S&P Pure Style Indices typically outperformed their S&P Style Index counterparts in months when their style was in favor. Based on data since 1997, Exhibit 4 shows that S&P Pure Style Indices posted higher average monthly total returns than S&P Style Indices when their style outperformed.

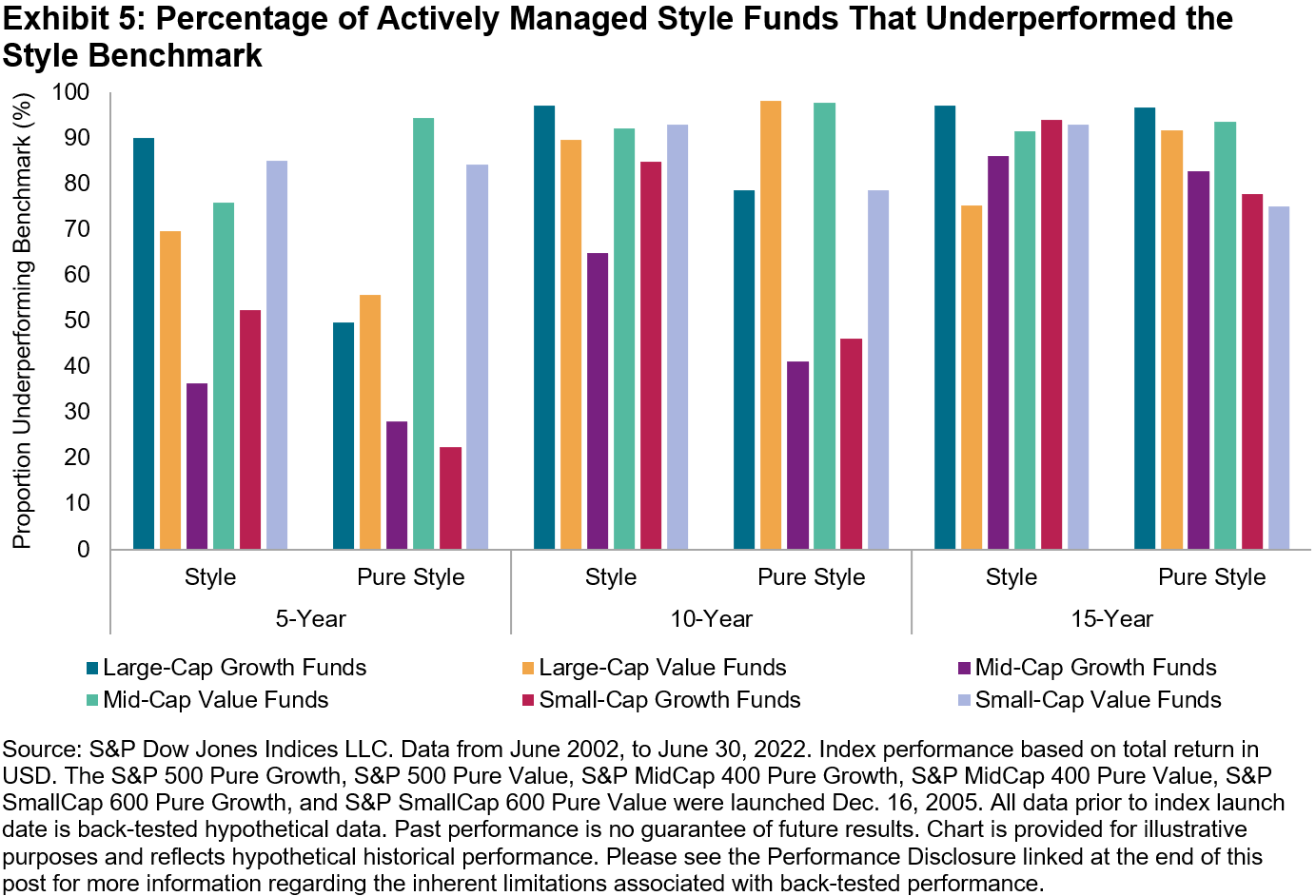

Lastly, we compare how actively managed funds have fared against the S&P Style and Pure Style Indices. Exhibit 5 compiles historical data of the percentage of actively managed style funds that underperformed both index series. Even though some active managers had success in shorter time periods, the S&P Style and S&P Pure Style Indices were difficult to beat over long-term horizons.

In conclusion, differences in design and objectives between the S&P Style and S&P Pure Style Indices allow investors to express style exposures in different ways: a broad and exhaustive approach for S&P Style Indices, or a narrower and selective approach for S&P Pure Style Indices. While the S&P Pure Style Indices can be used as suitable benchmarks for actively managed style portfolios, historical results show the potential benefit of taking an index-based approach.

The posts on this blog are opinions, not advice. Please read our Disclaimers.