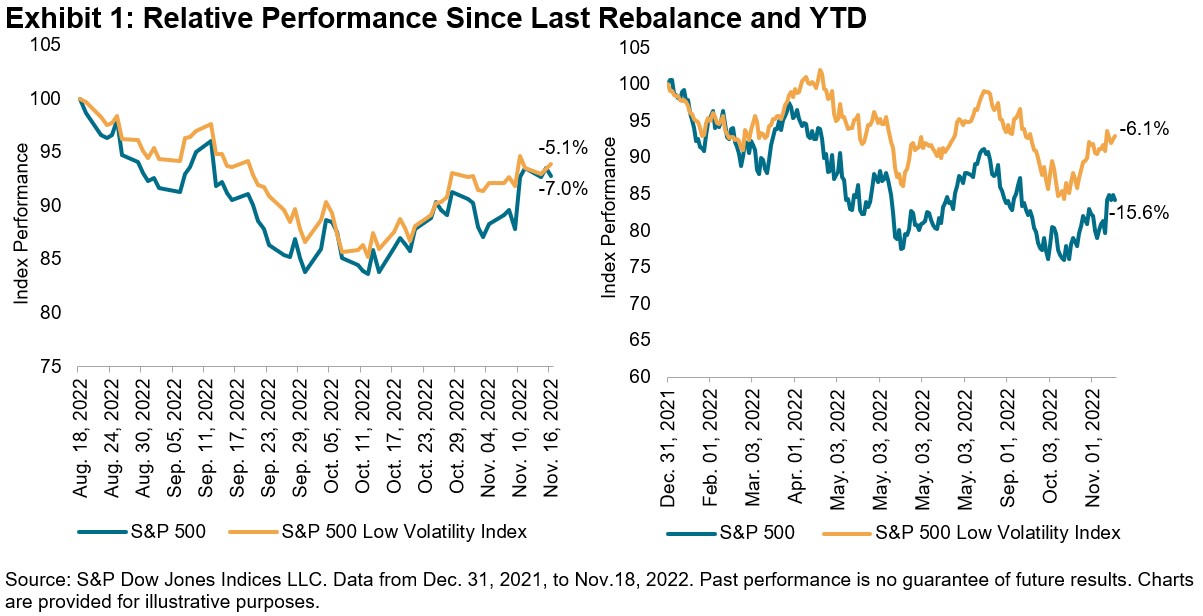

U.S. equities struggled again in the past three months. The last rebalance for the S&P 500® Low Volatility Index was in August 2022 and the S&P 500 has since declined 7.0%. The S&P 500 Low Volatility Index, which has historically moderated the performance of the benchmark, lost 5.1% in the same period.

For the entirety of 2022 so far, Low Volatility’s outperformance was much more impressive, declining just 6.1% compared to a loss of 15.6% for the S&P 500. Delivering what the strategy aims at, the low volatility index achieved its 9.5% outperformance with a standard deviation of 18% versus 25% for the benchmark S&P 500.

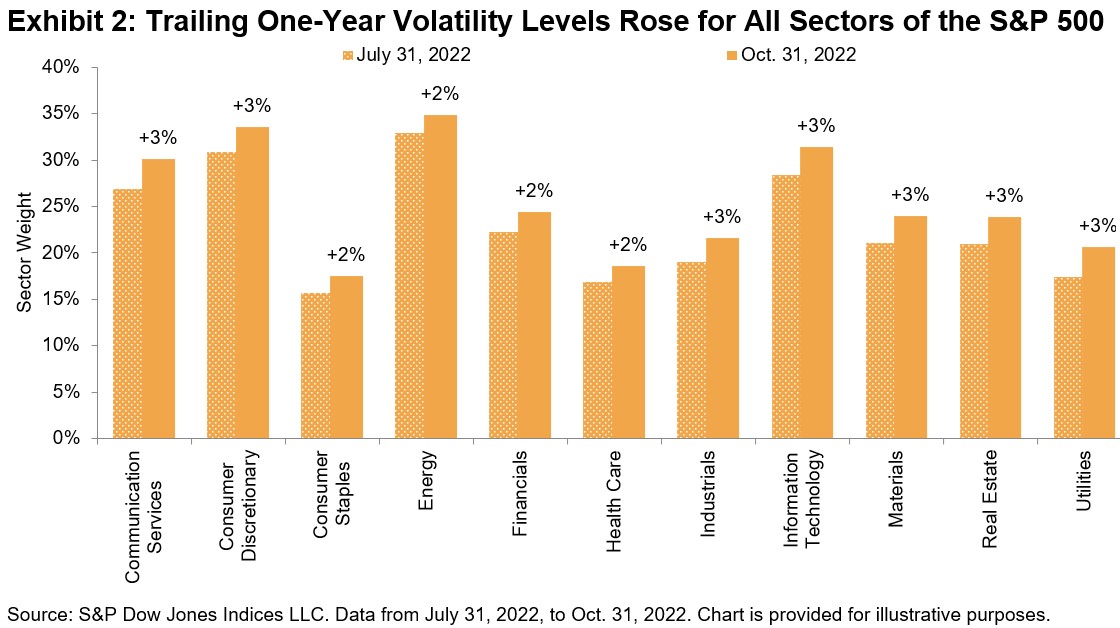

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

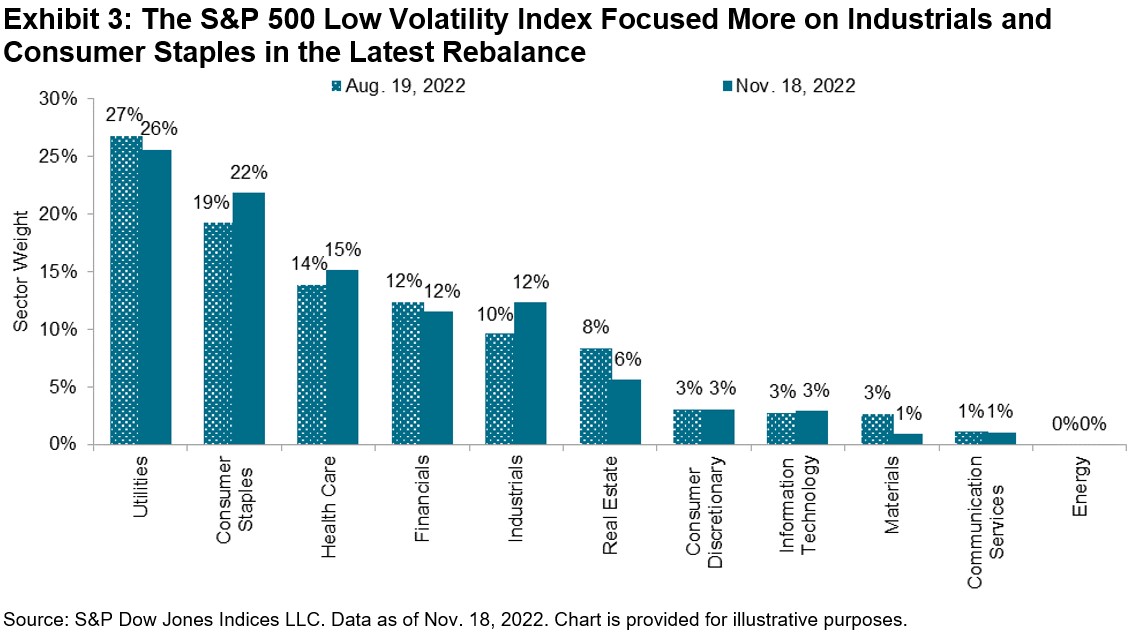

The latest rebalance, effective after the market close on Nov. 18, 2022, yielded just minor shifts in allocation. The two sectors that reduced their presence most significantly in the index were Real Estate and Materials, while the index focused more on Industrials and Consumer Staples. While Utilities also lost some ground, it remains the largest sector in the index. Energy stocks, which disappeared from the index in May 2020, have yet to make a reappearance.

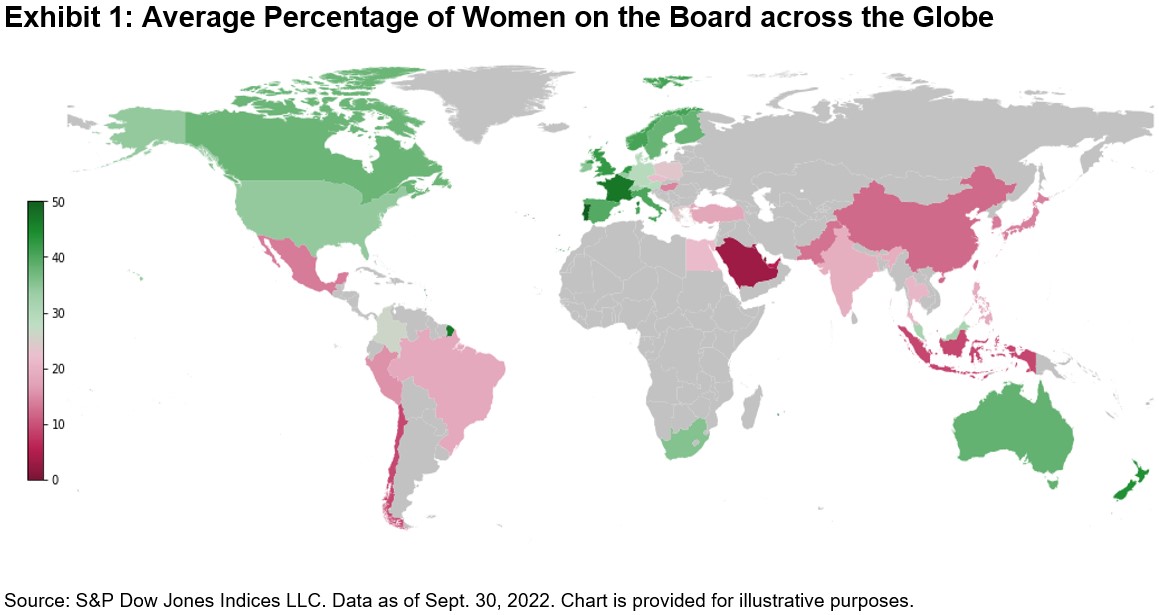

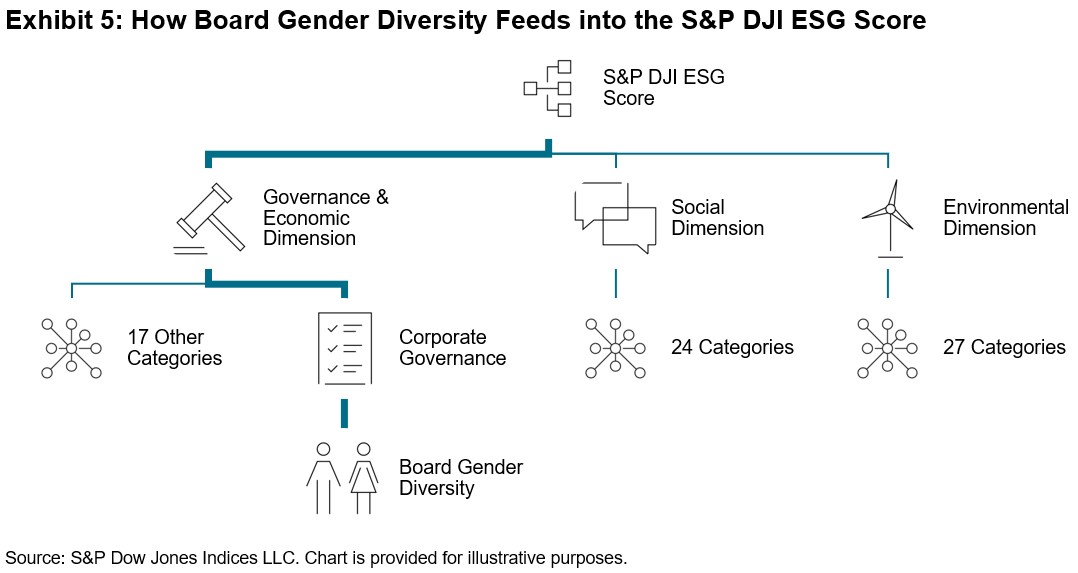

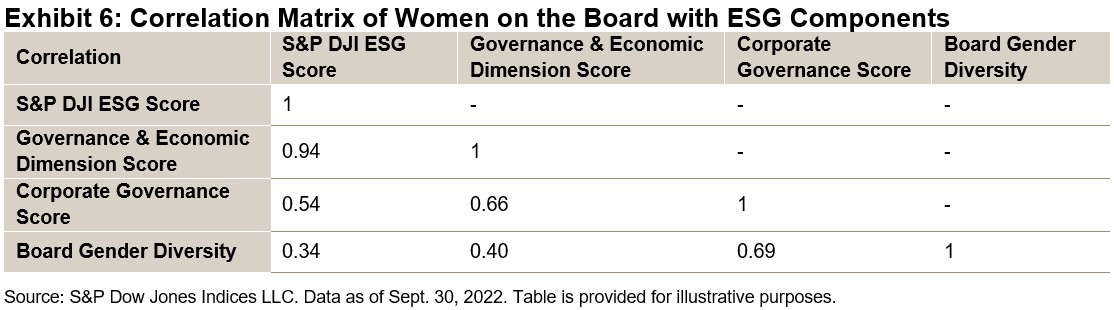

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.