This blog is the second in the quarterly blog series we recently introduced to provide transparency into rebalance adds and drops for our S&P Quality, Value & Momentum Top 90% Multi-factor Indices (S&P QVM Top 90% Indices). The S&P QVM Top 90% Indices seek to track constituents in the top 90% of their universe, ranked by their average multi-factor score (subject to constraints) and float-market-cap weighted.

Exhibits 1, 2 and 3 summarize the June 2022 rebalance adds and drops for these indices as well as the decile ranks of their individual quality, value and momentum scores. As a reminder, the 1st decile includes companies ranked in the top 10% of the universe (by their respective factor scores), the 2nd decile includes companies ranked in the next highest 10%, and so on through to the 10th decile.

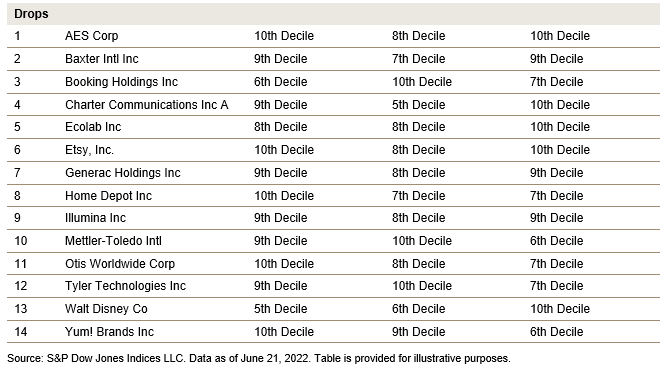

S&P 500® QVM Top 90% Index Rebalance Adds/Drops

There were 18 adds and 14 drops in the June 2022 rebalance. Since the March 2022 rebalance, Cerner Corp and People’s United Financial Inc were removed from the index, as they were acquired by Oracle and M&T Bank, respectively. Additionally, Under Armour Inc. and IPG Photonics were removed from the S&P 500.

Based on the overall multi-factor score ranks, 17% of the adds ranked in the top half of the universe, driven relatively evenly by all three factors. Similarly, all three factors contributed in relatively equal proportions to drops. Of the drops, 36% were in the 10th decile based on quality and momentum scores, while 21% were in the 10th decile based on value score.

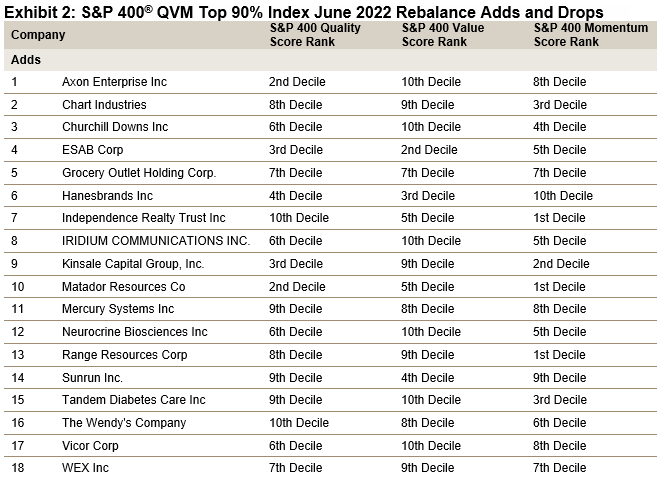

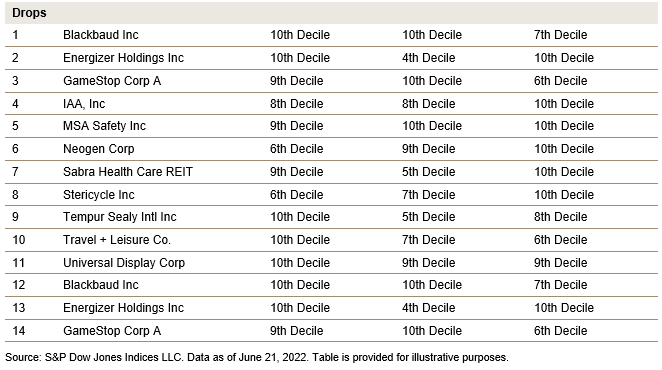

S&P MidCap 400® QVM Top 90% Index Rebalance Adds/Drops:

Seven companies were removed either due to acquisition events or movements across the cap range since the March 2022 rebalance. Therefore, there were seven more adds than drops in the June 2022 rebalance.

Momentum and quality scores primarily drove the drops from the index. Of the drops, 45% were in the 10th decile based on their quality score, 27% based on their value score and 55% based on their momentum score.

For the adds, 28% of companies had at least two factors ranked in the top half of the universe, and roughly one-half were in the top half based on their momentum score rank.

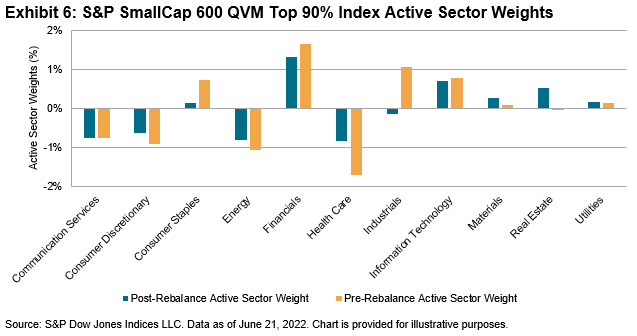

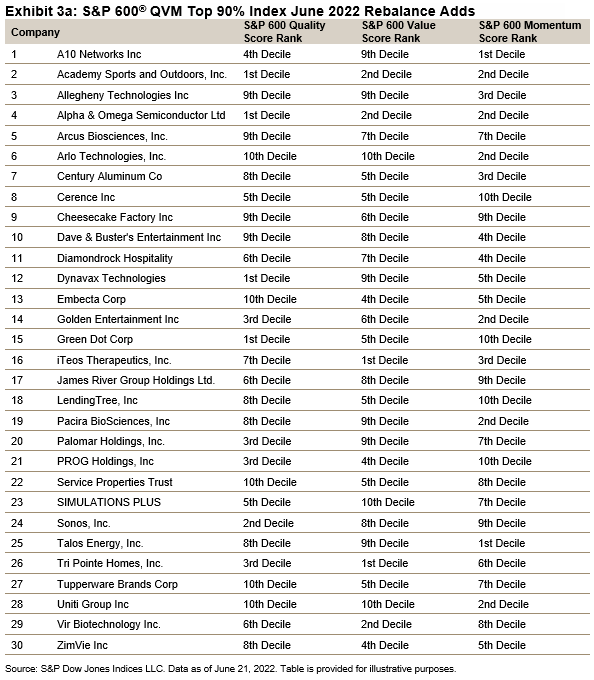

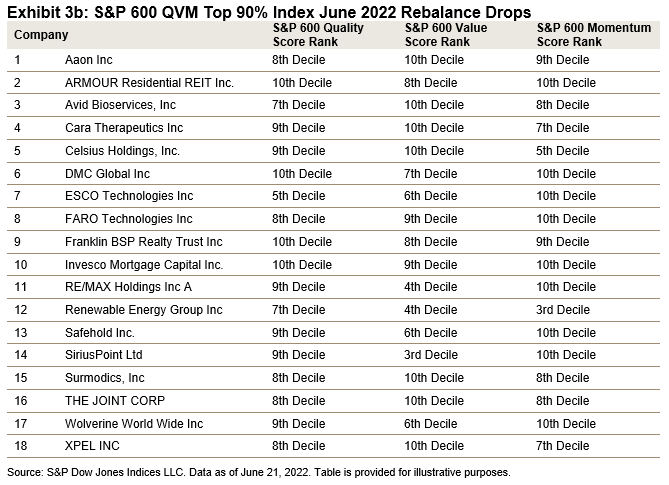

S&P SmallCap 600® QVM Top 90% Index Rebalance Adds/Drops:

There were 12 more adds than drops in the June 2022 rebalance. Renewable Energy Group Inc. was acquired by Chevron, while the other 11 companies were removed because they were dropped from the S&P SmallCap 600.

With respect to the adds, about half were ranked in the top half of the universe based on their momentum and value scores. In terms of the drops, most of the companies ranked quite poorly across all three factors. Of the drops, 22% were in the 10th decile based on quality score, 39% based on value score and 50% based on momentum score.

Sector Weights

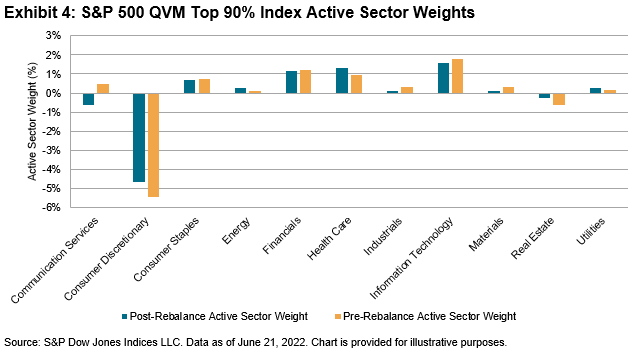

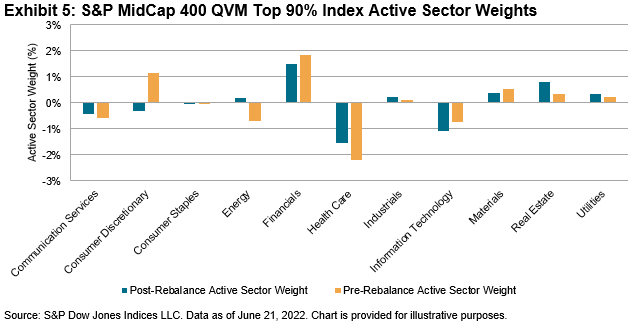

Due to the index construction methodology, large deviations from the benchmark sector weight are uncommon. Exhibits 4, 5 and 6 compare the pre- and post-rebalance active sector weights for each of the three S&P QVM Top 90% Indices.

Exhibit 4 shows that the relatively large underweight in the Consumer Discretionary sector decreased slightly, as have the overweights in IT and Financials. However, the overweight in Health Care slightly increased.

For the S&P 400 universe, the largest underweights were in Health Care and IT, which decreased and increased, respectively. The largest overweight was in Financials, which slightly decreased. Consumer Discretionary, which had an overweight pre-rebalancing, flipped to a slight underweight after the rebalance.

For the S&P SmallCap 600 QVM Top 90% Index, Energy and Health Care had the largest underweight, at approximately -0.80%, while Financials had the largest overweight, at 1.33%, after the June 2022 rebalance.