Investors are increasingly aspiring to align their investment objectives with their personal and societal values. At the same time, dividends are at the top of investors’ minds, as monetary policies tighten globally and volatility in the financial markets increases. In light of these trends, S&P Dow Jones Indices (S&P DJI) recently launched the S&P 500® ESG Dividend Aristocrats® Index, the latest addition to the S&P ESG Dividend Aristocrats Indices family.

A Focus on Dividends and ESG

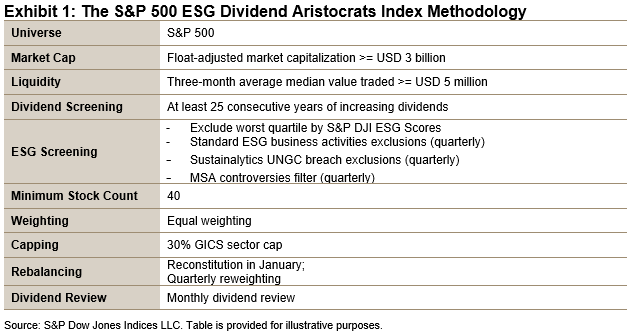

Exhibit 1 details the methodology of the S&P 500 ESG Dividend Aristocrats Index. The rules are consistent with the S&P 500 Dividend Aristocrats Index plus an ESG overlay. First, the index selects companies in the S&P 500 that have consistently increased dividends every year for at least 25 consecutive years. Next, multiple ESG screens are applied. The index excludes companies in the lowest quartile of S&P DJI ESG Scores.1 Additional ESG exclusion reviews are conducted quarterly based on business activities,2 United Nations Global Compact (UNGC) breaches3 and a Media and Stakeholder Analysis (MSA)4 controversy filter. Lastly, the remaining constituents are equally weighted and rebalanced quarterly.

Comparison of S&P DJI ESG Scores and Dividend Yields

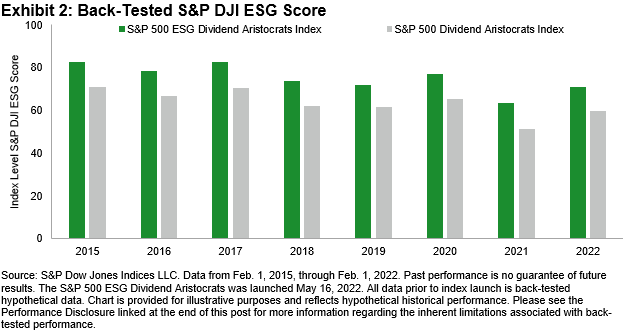

Turning to the index characteristics, Exhibit 2 shows that the S&P 500 ESG Dividend Aristocrats Index offered notable S&P DJI improvement over the S&P 500 Dividend Aristocrats Index. The S&P DJI ESG Score was improved, on average, by approximately 11.5 points per year, more than an 18% annual improvement.

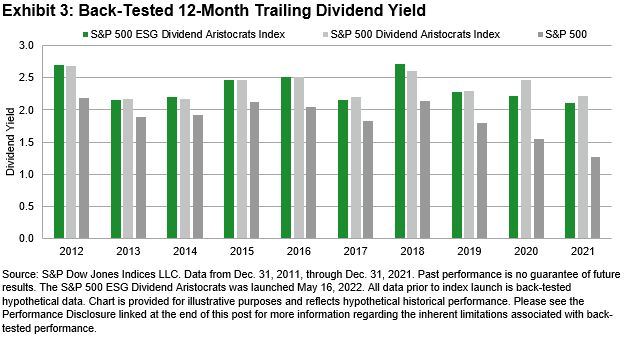

Looking at Exhibit 3, the S&P 500 ESG Dividend Aristocrats Index and the S&P 500 Dividend Aristocrats Index have had comparable yields, and both have held a significant yield advantage over the S&P 500. Over the full period examined, the average annual dividend yields for the S&P 500 ESG Dividend Aristocrats Index, S&P 500 Dividend Aristocrats Index and S&P 500 were 2.35%, 2.38% and 1.88%, respectively.

Performance

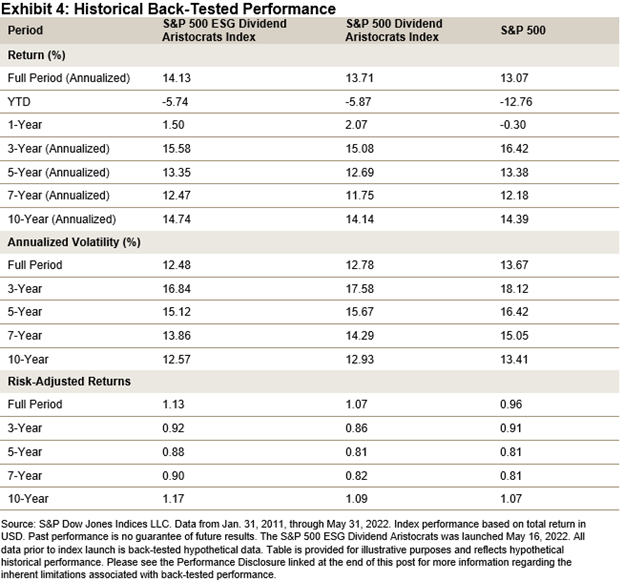

Exhibit 4 shows that the S&P 500 ESG Dividend Aristocrats Index has generated higher risk-adjusted returns over the 3, 5, 7, 10 and full year periods versus the S&P 500 Dividend Aristocrats Index and S&P 500.

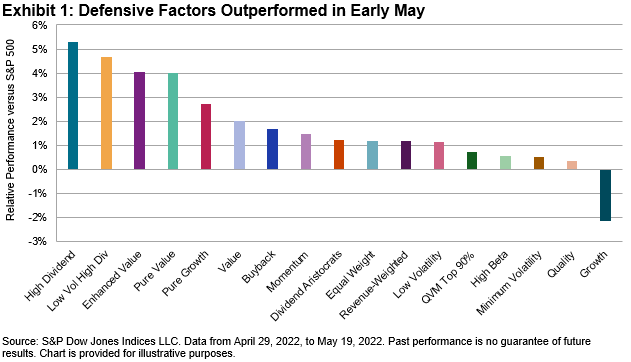

Interestingly, as financial conditions have tightened materially since the start of 2022, companies with consistent dividend payments have outperformed the broad market. Year-to-date, the S&P 500 ESG Dividend Aristocrats Index and the S&P 500 Dividend Aristocrats Index have outperformed the S&P 500 by 7.02% and 6.89%, respectively.

This may be due to two reasons; first, because cash returned to investors is more valuable now that real interest rates are rising,5 and second, because a company’s ability to consistently increase dividends could signal a durable business model that is well positioned to outperform throughout the business cycle.

When it comes to the goal of pairing consistent dividend paying companies with investment objectives that align personal and societal values, the S&P 500 ESG Dividend Aristocrats Index could be an option to consider.

- The S&P DJI ESG Scores are the result of further scoring methodology refinements to the S&P Global ESG Scores that result from S&P Global’s annual Corporate Sustainability Assessment, a bottom-up research process that aggregates underlying company ESG data to score levels.

- Companies with the following specific business activities are excluded: controversial weapons, thermal coal, tobacco products, oil sands, small arms and military contracting.

- As of each rebalancing reference date, companies classified as non-compliant with the United Nations Global Compact principles according to Sustainalytics are ineligible for index inclusion.

- The MSA monitors a company’s sustainability performance on an ongoing basis by assessing current controversies that could potentially threaten a company’s reputation or financial health.

- https://fred.stlouisfed.org/series/DFII10.

The posts on this blog are opinions, not advice. Please read our Disclaimers.