The years between 2017 and 2021 were a frustrating half-decade for value investors. The S&P 500 Growth Index advanced at a compound annual rate of 24.1%, more than double the 11.9% return of its Value counterpart. Despite occasional (and sometimes prematurely celebrated) periods of success, Value underperformed Growth in four years of the five (and its win in 2019 was close).

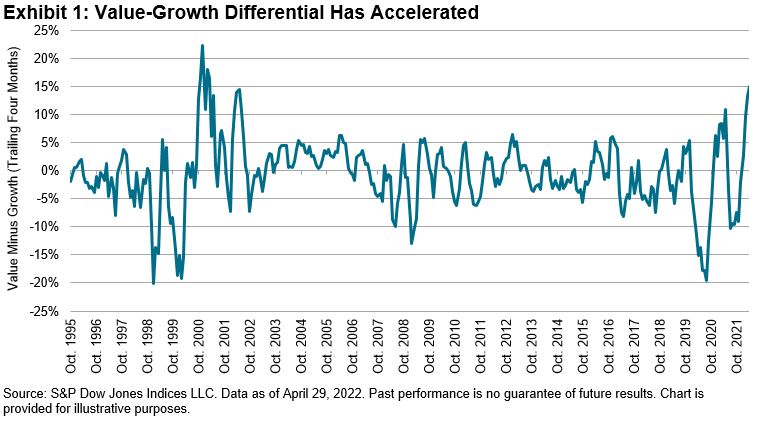

In the first four months of 2022, however, the style winds shifted, as Value (-5.0%) dramatically outperformed Growth (-20.0%). Exhibit 1 puts this difference in historical context, comparing January-April 2022 to all other trailing four-month intervals in our database. The 15% gap between Value and Growth is obviously high by historical standards, and represents a dramatic reversal from recent trends. (As recently as nine months ago, the gap favored Growth by more than 10%.)

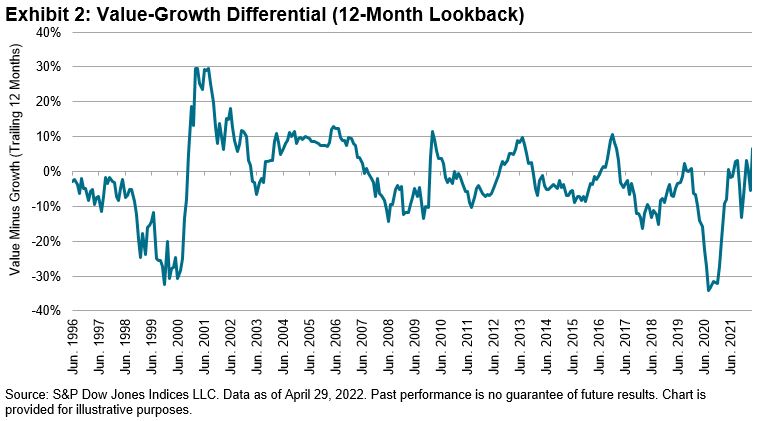

Exhibit 2 examines the same data with a 12-month lookback. The acceleration of Value’s performance is nearly as impressive from this perspective. At the end of April 2022, Value was 6.5% ahead of Growth; just five months ago, for the year ending November 2021, Growth was 13.3% ahead of Value.

For either lookback period, the conclusions are clear: Value has outperformed Growth to a historically uncommon degree, and this differential has accelerated quite dramatically in the last year.

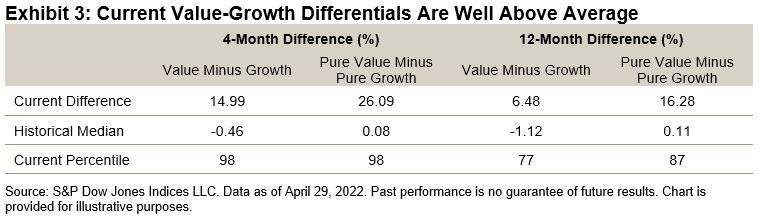

What does this portend for the future relative performance of Value and Growth? Spoiler alert: I don’t really know, but there are at least some reasons to suspect that Value’s advantage may weaken in the near term. Exhibit 3 compares the current Value-Growth spread to its historical level.

Value’s 15% differential for the first four months of 2022 was not only visibly above average, it’s at the 98th percentile of all such spreads in our historical data. The only higher readings came in the deflation of the technology bubble more than 20 years ago. Comparing Pure Value and Pure Growth produces much the same result. The trailing 12-month data suggest a similar, if somewhat less extreme, conclusion, with Value’s outperformance just into the top quartile of its history. (Similar analysis for mid- and small-cap style indices show much the same results.)

The fact that a data point is high in its historical distribution doesn’t mean that next month’s observation can’t be equally high, or higher. There’s no guarantee, for that matter, that the distribution is stable, and that the next observation won’t surpass the previous all-time record. That said, history suggests that the torrid outperformance of Value is unlikely to continue, at least in the short term, and that the next big move in the Value-Growth differential is more likely to be down than up.

The posts on this blog are opinions, not advice. Please read our Disclaimers.