The S&P BSE SENSEX 50 is designed to measure the performance of the top 50 largest and most liquid companies in India. The index constituents are weighted based on their float-adjusted market cap and must have a minimum annualized trading value of INR 10 billion. The S&P BSE SENSEX 50 is a highly diversified index, and its 50 constituents provide exposure to all 10 major sectors: Utilities, Telecommunication Services, Information Technology, Industrials, Healthcare, Fast-Moving Consumer Goods (FMCG), Finance, Energy, Consumer Discretionary, and Basic Materials.

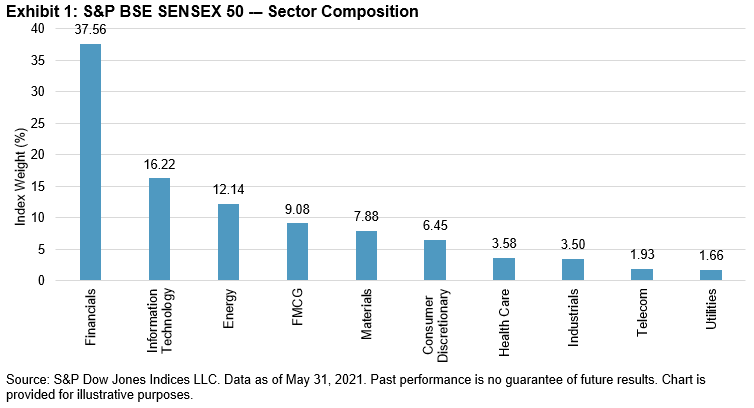

Exhibit 1 presents a pictorial representation showing the weight of the 10 sectors of S&P BSE SENSEX 50, as of May 31, 2021. We can see that the Financials and Information Technology sectors had the highest representation, at 37.56% and 16.22%, respectively, while the Telecommunications and Utilities sectors had the least representation, at 1.93% and 1.66%, respectively.

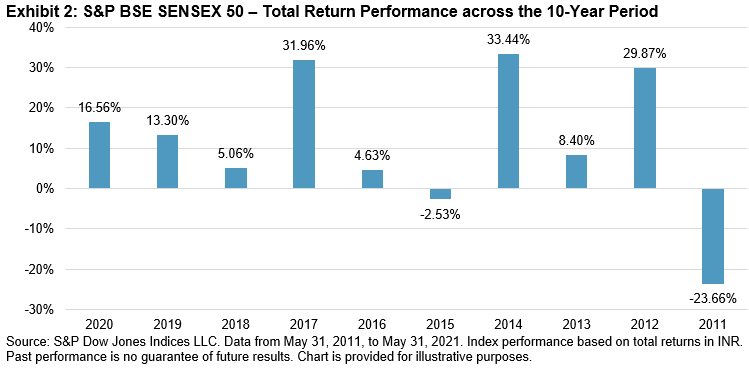

The returns of the S&P BSE SENSEX 50 have been promising over the past 10 years. The total returns index value has gone up from 6,095.76 on May 31, 2011, to 20,092.21 on May 31, 2021, reflecting an absolute return of 230%.

From Exhibit 2, we can see that in 8 out of 10 calendar years, the S&P BSE SENSEX 50 posted positive returns. The highest total returns of 33.44%, 31.96, and 29.87% occurred during 2014, 2017, and 2011, respectively. 2011 was the only year during which the index posted a significant negative return of -23.66%.

Exhibit 3 shows the annualized risk/return profile of the S&P BSE SENSEX 50 for 3-, 5-, and 10-year periods. Overall, the index’s returns were promising across all periods observed.

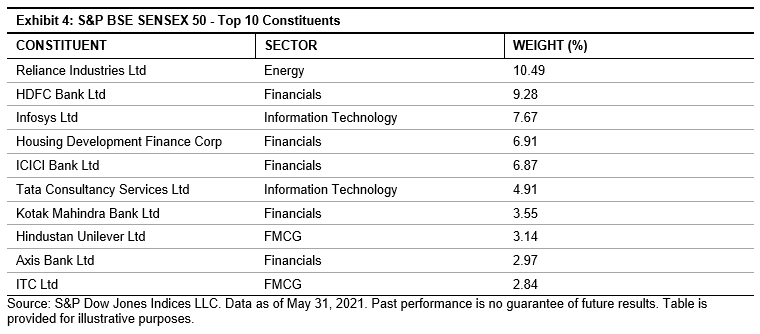

Exhibit 4 shows the top 10 constituents of the S&P BSE SENSEX 50 along with their corresponding sectors. We can see that Reliance Industries Ltd holds the highest weight, at 10.49%, followed by HDFC Bank Ltd at 9.28%. Furthermore, 4 of the 10 major sectors are well represented in the top 10 list.

To summarize, we can state that the S&P BSE SENSEX 50 is a well-diversified, liquid index that has a history of strong performance over the past decade.

The posts on this blog are opinions, not advice. Please read our Disclaimers.