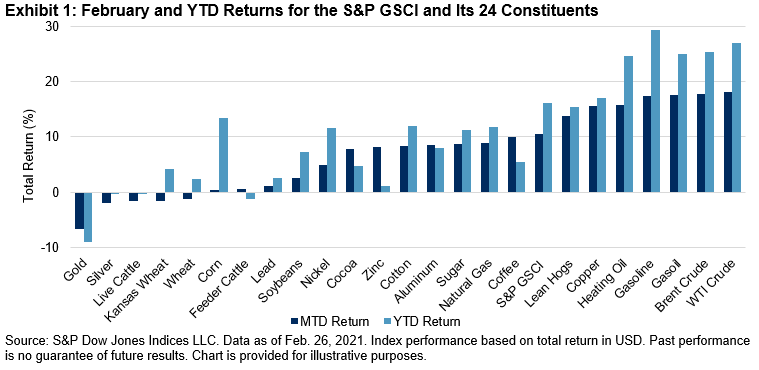

An inflationary tide lifted almost all commodity boats in February 2021. Most constituents of the S&P GSCI rose while gold, the commodity that market participants often look to for inflation protection, lagged. The S&P GSCI rose 10.6% overall in February, with copper and energy doing most of the heavy lifting.

After a strong January, the S&P GSCI Crude Oil accelerated further in February, rising 18.1%. A combination of continued OPEC+ production compliance and a historic cold weather event in Texas, knocking out more than four million barrels per day of production, were the catalysts driving this oil price gush. The remaining energy commodities followed suit, with gains of at least 9% for the month.

The S&P GSCI Copper woke up in February to join the energy party, rising 15.6%, close to double the next-best-performing industrial metal, the S&P GSCI Aluminum. Copper inventories were depleted and remained at levels not seen since 2005. The swiftness of the decline in copper inventories was unprecedented. The ramp up in manufacturing activity continues across the world, as demonstrated by the latest strong PMI readings. The clean air push is also contributing to the rally in industrial metals. China’s upcoming NPC meeting will be a highlight, with this event likely to affect future demand, as well as the production of aluminum, the most energy-intensive metal to produce.

The S&P GSCI Gold fell 6.6% in February as safe haven assets were sold off in favor of more bullish asset classes and U.S. bond yields spiked. This was the largest monthly drop in gold prices since November 2016. The S&P GSCI Platinum rose 9.8%, breaking out to a five-year high on the back of a potential third year of global supply deficits and new market awareness of the metal’s use in hydrogen energy technologies.

The S&P GSCI Agriculture ended the month up 2.1%; soybeans and corn rallied to multi-year highs, driven by relentless buying from China as it rebuilds its hog herd following the devastation caused by African swine fever. The S&P GSCI Sugar rallied 8.8% in February, with industry forecasters further trimming sugar surplus estimates for the current and new crop years.

The livestock sector was dominated by an impressive rally in lean hogs; the S&P GSCI Lean Hogs rose 13.7%. Lean hog futures have been trending higher since mid-December 2020 due to a combination of higher wholesale prices, extreme weather events, and exports to other markets helping offset the expected decline in shipments to China.