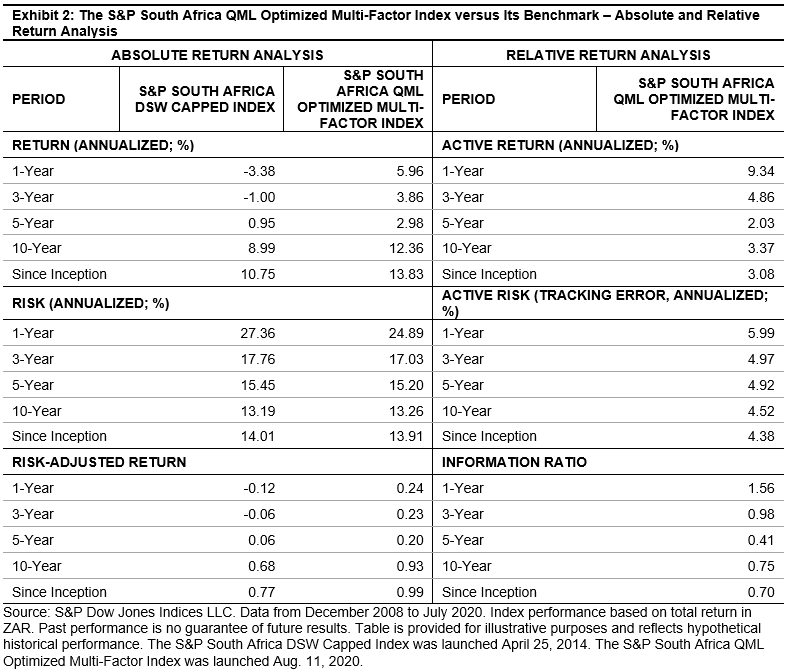

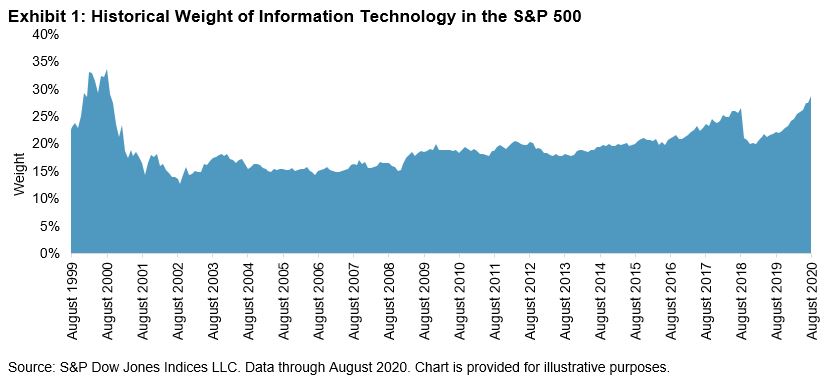

As of the end of August 2020, the S&P 500® Information Technology sector had risen a remarkable 36% YTD. Such outstanding relative performance of course reminds us of the late 1990s, when the markets experienced a technology bubble and subsequent bust.

One notable resemblance to the late 1990s is Information Technology’s weight in the S&P 500. Information Technology makes up 28.7% of the S&P 500 today, and its weight hasn’t been this high since August 2000, when IT was 33.6% of the index, as we see in Exhibit 1.

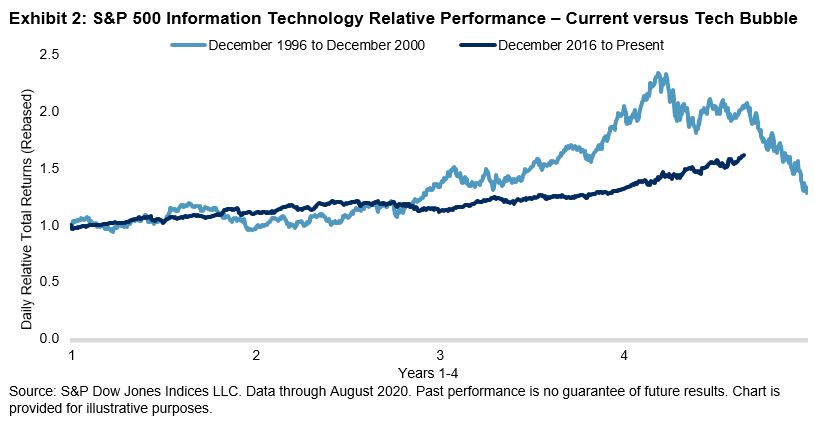

But the similarities end there. When we compare the most recent run-up in IT to its counterpart from 20 years ago, we observe that the current relative outperformance of the sector is much less extreme than during the late 1990s (see Exhibit 2). Moreover, the relative volatility of the IT sector was much higher then (December 1996-December 2000) than it is now, with an annualized standard deviation of daily relative returns of 23%—almost two and a half times the current period’s standard deviation of 9.5% (December 2016-August 2020).

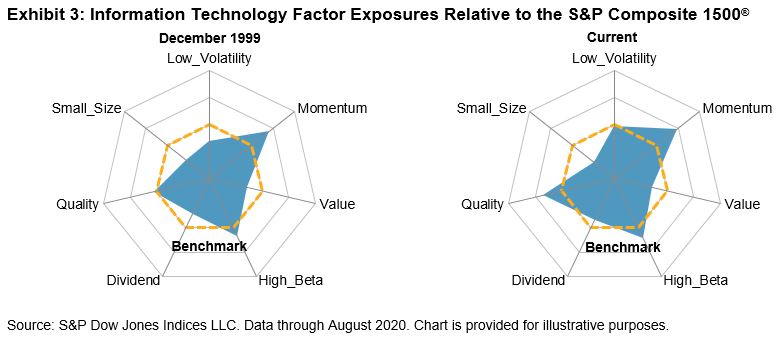

Finally, we observe significant differences when we compare the current factor exposures of the IT sector to its exposures in December 1999. Exhibit 3 shows that in 1999 and the present, IT had a strong tilt toward momentum and high beta and a tilt away from value. However, one of the main differences between now and then is that IT currently has much stronger tilts toward quality and low volatility than it did in 1999. This suggests that the companies within the current IT sector are both more profitable and less volatile now than they were 20 years ago.

Of course, with the considerable benefit of hindsight, we know that IT’s earlier outperformance peaked in March 2000. No one can know in advance what the future relative returns of the IT sector will be and whether its outperformance will continue, but history tells us that the Tech sector of today is not your father’s Tech sector.

The posts on this blog are opinions, not advice. Please read our Disclaimers.