The equity risk premia from factors (such as quality, momentum, and low volatility) have been widely accepted and adopted by investment practitioners across the globe and South Africa alike. The belief by many is that exposure to these risk factors, in addition to the market, could reward investors over the long term.

While the long-term outperformance of most factors can be backed by economic rationale, each is still susceptible to significant drawdowns over short-term horizons. Timing factor exposures is one option to avoid this; however, it may require a crystal ball to navigate the markets. Better yet, diversifying across multiple factors at once could offer a more attractive solution. Since factor returns are relatively uncorrelated, the benefits of diversification may generate more stable excess return outcomes.

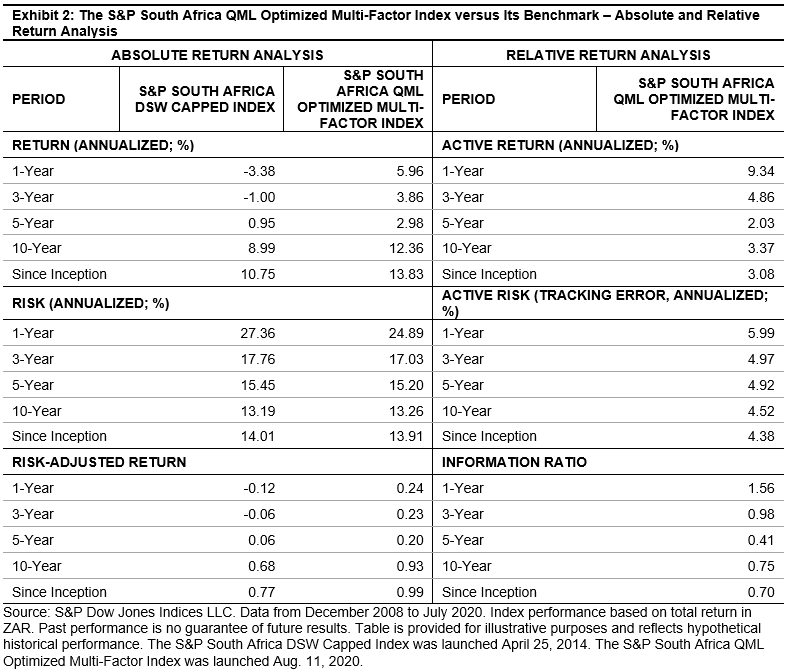

The new S&P South Africa Quality, Momentum & Low Volatility (QML) Optimized Multi-Factor Index adopts this philosophy and aims to systematically capture multiple risk premia simultaneously through an optimization approach. Exhibits 1 and 2 show the back-tested results of this strategy, which has been effective to date.

The primary objective of the multi-factor index seems simple enough; select stocks with the best quality, value, or momentum exposure. However, practically implementing this selection while adhering to other portfolio concerns can be fraught with challenges. For instance, how does one ensure that:

- The intended factor exposures are well balanced;

- The unintended sector exposures are limited;

- The tracking error to the benchmark index is controlled; and

- The turnover is low, efficient, and liquid to minimize trading costs and ensure capacity?

Optimizing the portfolio selection process is arguably the simplest way to solve this complex predicament. Through the power of a portfolio optimizer, its accompanying risk model, and S&P DJI’s Factor Scores, the solution reveals itself.

A mathematical optimization process is employed to help discover the most suitable stock selection and weighting that meet the objective to maximize multi-factor exposure, while abiding by any portfolio constraints. The constraints are simply a set of rules that help define the characteristics of the index.

In the case of the S&P South Africa QML Optimized Multi-Factor Index, these constraints include the following:

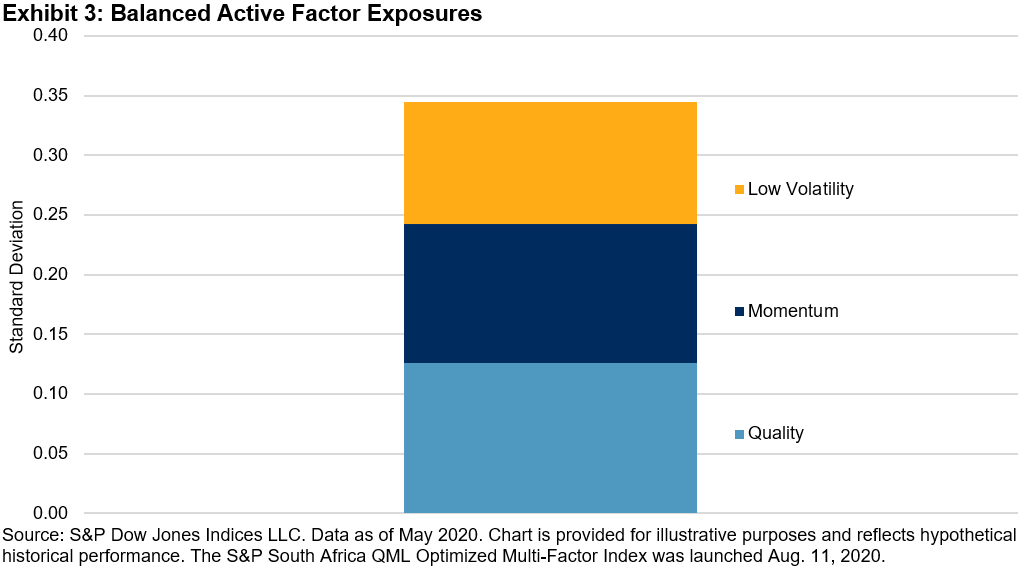

- Balanced active factor exposures to quality, momentum, and low volatility;

- Sector weights between 50%-150% of its benchmark weights;

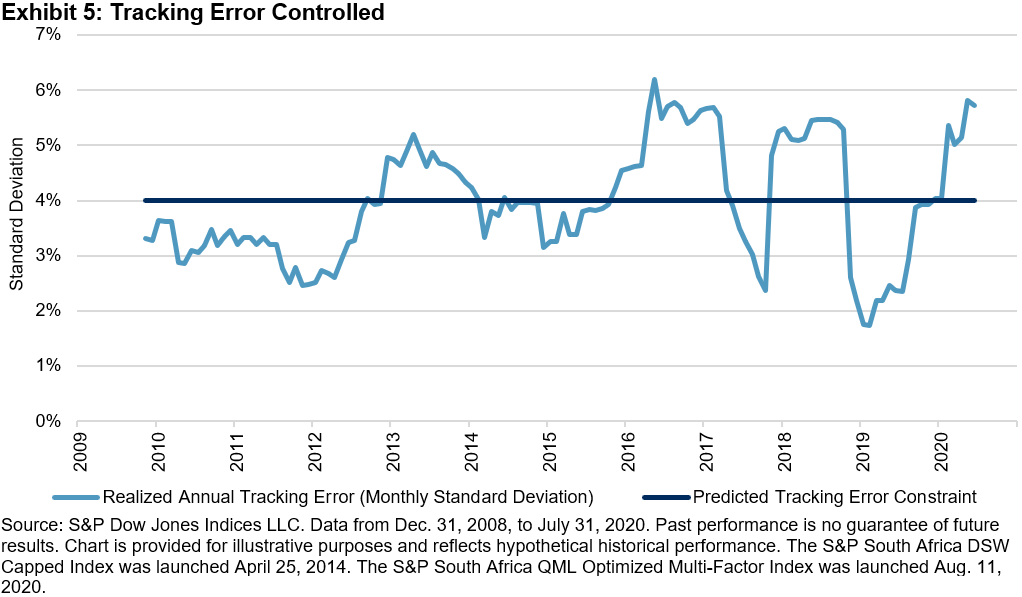

- Predicted tracking error to the benchmark index targeting 4%;

- Quarterly two-way turnover of no more than 25%; and

- The turnover of any position (i.e., each trade) should reflect the available liquidity.

In summary, the S&P South Africa QML Optimized Multi-Factor Index has historically achieved systematic diversification across factors through the powerful precision of its optimization process. Its controlled tracking error to the benchmark may also make it attractive to market participants looking for a core holding. Equally, those typically enticed by active funds’ promise of potentially higher returns could be compelled by the index’s historical performance, not to mention the relative advantages of lower cost and greater transparency associated with passive products. Either way, the S&P South Africa QML Optimized Multi-Factor Index may represent the next generation of smart beta for South Africa.

The posts on this blog are opinions, not advice. Please read our Disclaimers.